Fast-forwarding on a few weeks from London’s IE week, the overall tone for oil prices has moved dramatically away from bullish expectations for the second half of the year, to downward revisions in response to the “risk-off” mode seen across global markets.

Brent and WTI crude futures have fallen (as of 21 March) to levels last seen more than a year ago and before the Russia-Ukraine war. Meanwhile the main oil product futures contracts (Ice Gasoil and Nymex RBOB) have also fallen sharply since the start of the month. While some of this is linked to a wider sell-off in financial markets, our global flows data shows strong signs of alignment with the bearish sentiment.

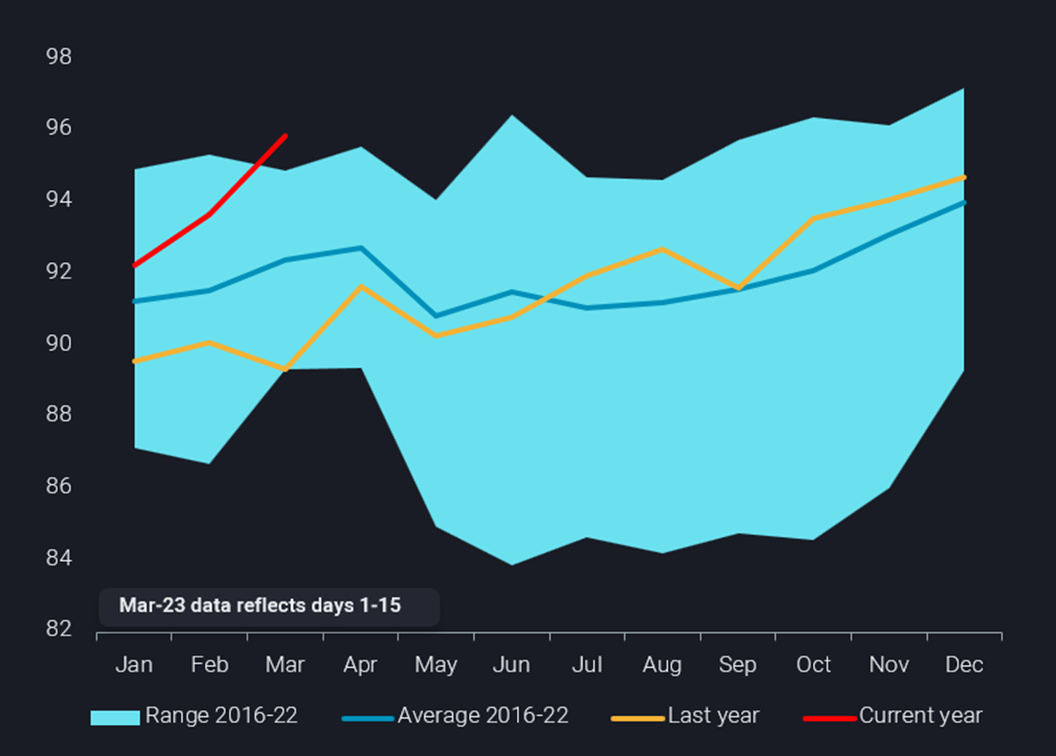

So far this month, total seaborne oil loadings have been exceptionally high, as indicated by loading volumes breaking outside of the seven-year range (see chart above).

For the first time since April 2020, global crude/condensate loadings have almost hit 50mbd (March 1-15), up by around 400kbd from February. Across all products (clean, dirty, LPG/NGLs and chemicals), the total for the so far in March is 46mbd, also a multi-year high.

Concerns about a lack of supply or availability of oil, be it crude oil or diesel – both were previously considered most at risk of disruption due to the Russia-Ukraine war – have not materialised and both commodities have shown signs of ample supply.

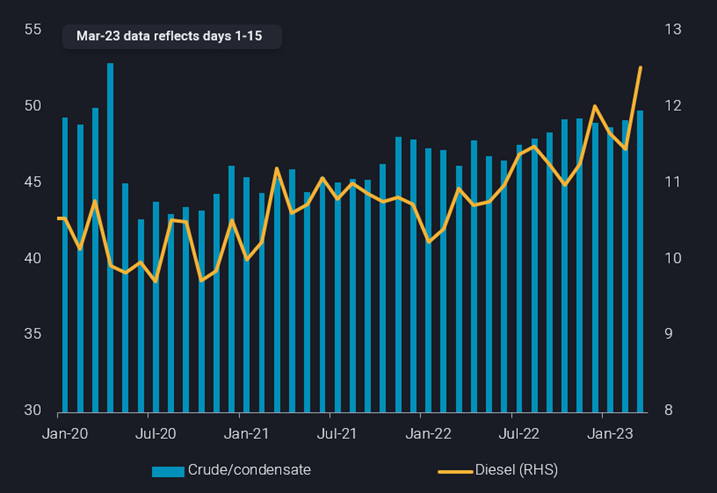

Russian crude loadings so far in March have held stable m-o-m at 3.6mbd, despite announcements from Moscow of a 500kbd production cut. At the same time, Russian diesel loadings are up 400kbd m-o-m to an extraordinarily high 1.5mbd so far in March. Though some of this rise is due to deferred loadings from February, it still represents a multi-year high and is contributing to the global picture.

Supported by rising Russian loadings, global diesel loadings show strong growth averaging almost 12.6mbd so far in March and significantly above the former multi-year peak of around 12mbd seen in December.

For diesel, it is important to note the relatively muted response in diesel prices to ongoing strikes across France. France is historically a huge diesel importer and was so especially from Russia pre-war. But despite at least three French refineries running at reduced levels or not at all (Argus Media) and the limited ability at seaborne terminals to quickly increase imports, Ice gasoil futures are still below levels seen at the start of the month.

In conclusion, while the price action across the oil price complex has been sharp and intense, global seaborne oil flows do not suggest and looming supply crunch. At least for the near term supplies look ample and demand could be threatened, especially in the case of diesel, by wider recessionary concerns. In fact, the high exports could be a direct consequence of low domestic demand in the first place, e.g. in the US.