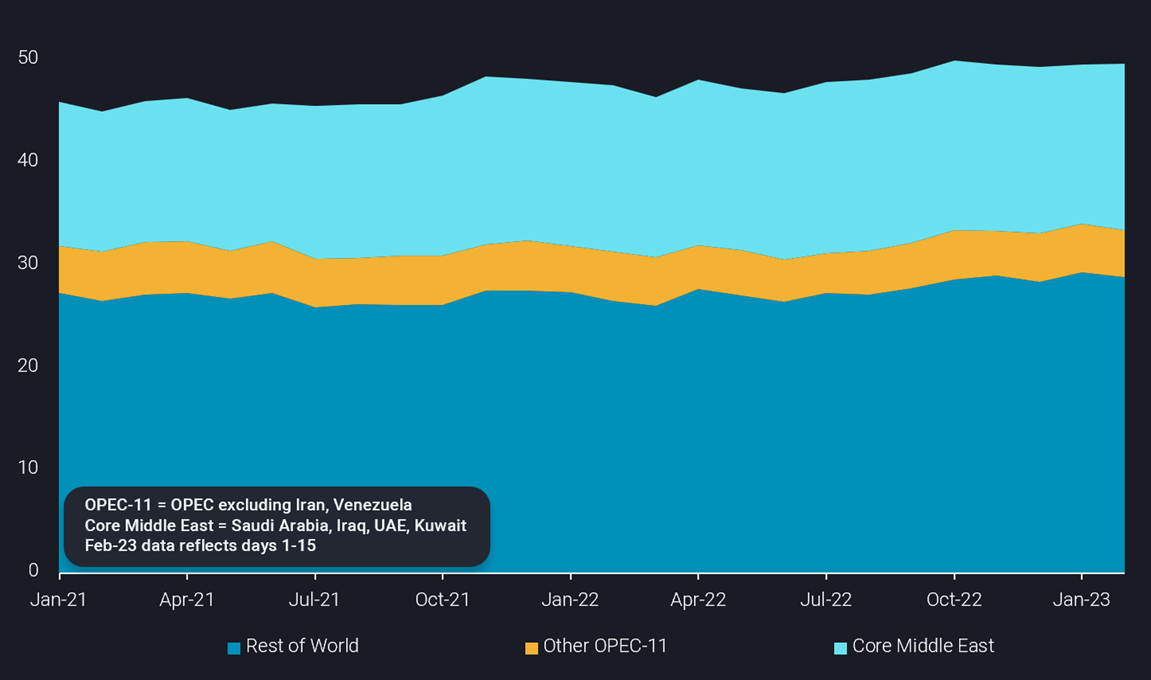

OPEC-11 crude loadings climb in February preventing dip in global seaborne supply

In this insight, we investigate the different trends emerging in crude/condensate loadings from key producers and the impact on global supplies.

OPEC-11 crude/condensates loadings show a preliminary gain this month of 500kbd from January levels, as key Middle East nations are raising waterborne supplies. Higher loading activity from the key regional producers has helped nudge global loadings marginally higher over the same period despite weak loadings from other regions.

This marginal rise in near-term waterborne supplies, under a current environment of recessionary demand concerns and weakening global refining margins (especially on diesel) lends further support to a bearish price outlook going forward, at least in the near term.

OPEC loading activity highlights divergence between members

Total OPEC-11 loadings (i.e. excluding Iran and Venezuela) stand at just shy of 21mbd for February, an increase of about 0.5mbd from full-month January levels. But on closer inspection, we see in our February data a strong divergence in the performance of the big Middle East producers versus the rest of the OPEC group.

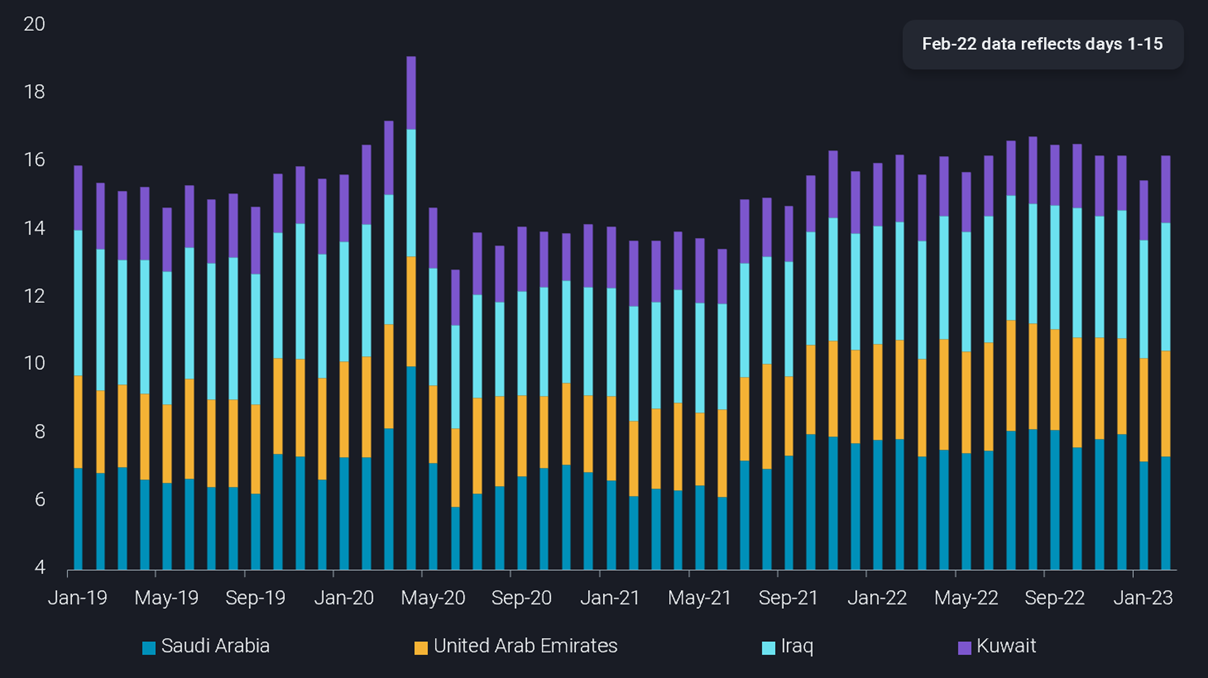

For the core Middle East nations, the overall theme observed in February flows is rising loading activity, after recovering from a weak January, and a very strong shift by some producers to target specific markets:

- Saudi loadings rose 150kbd m-o-m to 7.3mbd after having dropped in January to the lowest total since August 2021. Flows to Ain Sukhna (and therefore likely eventually to Europe via the SUMED pipeline) are on track to climb for the fourth consecutive month

- Iraqi loadings have grown strongly so far in February, up by almost 300kbd m-o-m, with flows to Europe rising even more sharply at 500kbd

- UAE loadings rose only marginally (<100kbd) m-o-m, but also show increased flows to Europe

- Kuwaiti flows (to all destinations) are up 200kbd m-o-m, but those to China have picked up even more strongly and rising to a multiyear record of 1mbd so far in February – well above the 600kbd average flow in 2022

Away from the Middle East, other OPEC producers, namely those in West Africa, are showing signs of falling behind again, after a relatively strong Q4 22.

- Nigerian supplies have fallen in February, for the second consecutive month, with loadings down m-o-m 170kbd from the December peak of 1.6mbd.

- Angolan loadings, at 1.1mbd so far in February are marginally lower m-o-m. There is a notable absence of flows to India – the nation is second only to China in historical imports of Angolan crude but is likely seeing more value importing long-haul Russian crude

Non-OPEC supply dips in February

Outside of OPEC supplies, the most important consideration for global crude supply is Russian activity. The start of this year marked a very sharp recovery in Russian exports in the aftermath of a very low December export programme – coinciding with the 5 December EU import sanctions deadline.

February exports, at 3.3mbd, are around 270kbd below January levels. But this should not be seen as a reflection of Russia’s recent comments to cut production by 500kbd as of March. When viewed under historical context, we see m-o-m declines in February are a seasonal phenomenon, as Russian refineries typically maximise product output around this period, with no maintenance work at this time of the year. Another factor to note is that under current market prices for Russian oil, whether under the price cap mechanism or not, Russia will naturally try to maximise product (especially diesel) exports over crude exports, where possible.

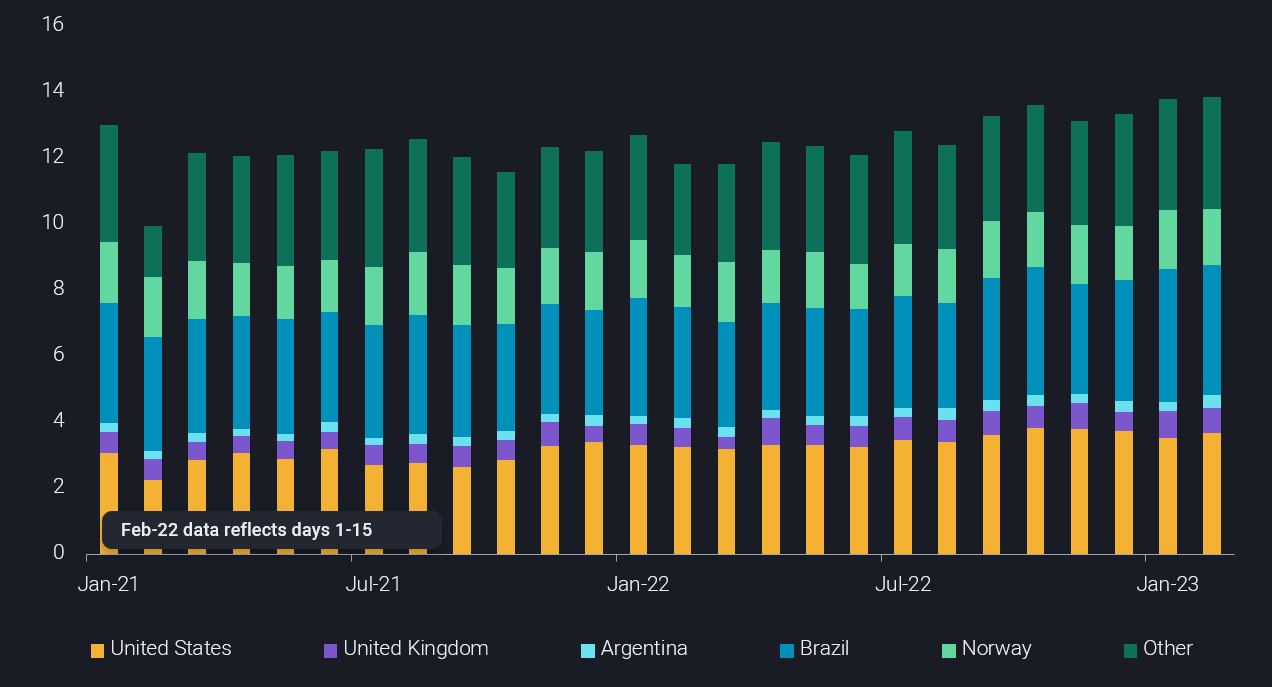

The other key component of non-OPEC supply is the Atlantic Basin. Loadings from the latter had been a crucial incremental source of supply in H2 22, especially for the European market. But the latest readings suggest while supply is still ample, it is plateauing.

Total Atlantic Basin loadings – defined as Europe, Med/NAfr, WAfr(non OPEC) and East Coast Americas are almost flat (+50kbd m-o-m) so far in February:

- The only major producers to have posted a m-o-m increase in loadings are the US, UK and Argentina, all in the order of 120-140kbd

- Brazil, Norway, and Egypt (incl via SUMED), which had all upped flows to Europe in recent months, posted total loading declines in the order of 50-100kbd

Taking into consideration the above, for now it seems global supplies are ample and are keeping a lid on prices – which have failed to break the $90bl level for more than three months now. However, looking ahead, the main concern over the medium to longer term is the one of spare capacity. Should there be a strong US gasoline driving season and/or a resurgence in Chinese products consumption, or even a wider/surprising increase in global oil demand, it is hard to see where extra supply could come from. Because of this, despite the recent bearish sentiment on crude prices, there is a fundamental, longer-term support factor that cannot be overlooked.