LNG portfolios turn to one year time-charters to mitigate growing volatility

Missing Freeport LNG supplies are starting to cool the spot shipping rates but LNG charterers are still seeking options to mitigate hikes in volatility and liquidity challenges for the coming winter.

Extreme volatility and high prices seen in the last year are changing the playing field for LNG trading in numerous ways. Global LNG flows are being reshuffled, with Europe challenging the dominance of Asian importers by hiking its year-to-date imports by 60% versus the same period last year. With this change, security of supply has been restored as the central principle for most buyers. Traditional 20-year agreements are back on the table, providing ripe conditions for new project developments.

At the same time, the LNG shipping market is shifting, as charterers are facing a hike in volatility as well, leading to a partial disconnect between spot markets and fundamentals as liquidity dries up. Like the buyers, charterers are seeking options to reduce exposure to the spot market. More players are opting for multi-year time-charters in their fleet to cover for winter stresses on the shipping demand. Evidently, LNG time-charter rates are up across all vessel types and the spot market has already risen well before peak winter demand.

Missing Freeport supplies are starting to cool the spot shipping market

The LNG shipping markets faced strong headwinds at the start of the year, as the European energy crisis rearranged global gas flows and sharply curtailed shipping demand. In spite of the knock-on effect on shipping fundamentals, the conflict in Ukraine kicked off a strong recovery in the spot market. This trend has continued into the summer market, with spot freight rates reaching 35% above last year. The implication of the recent fire and consequential complete shutdown of the Freeport LNG plant in Texas are starting to cool the spot freight rates. With initial market signals of a correction back towards the summer rates in 2021.

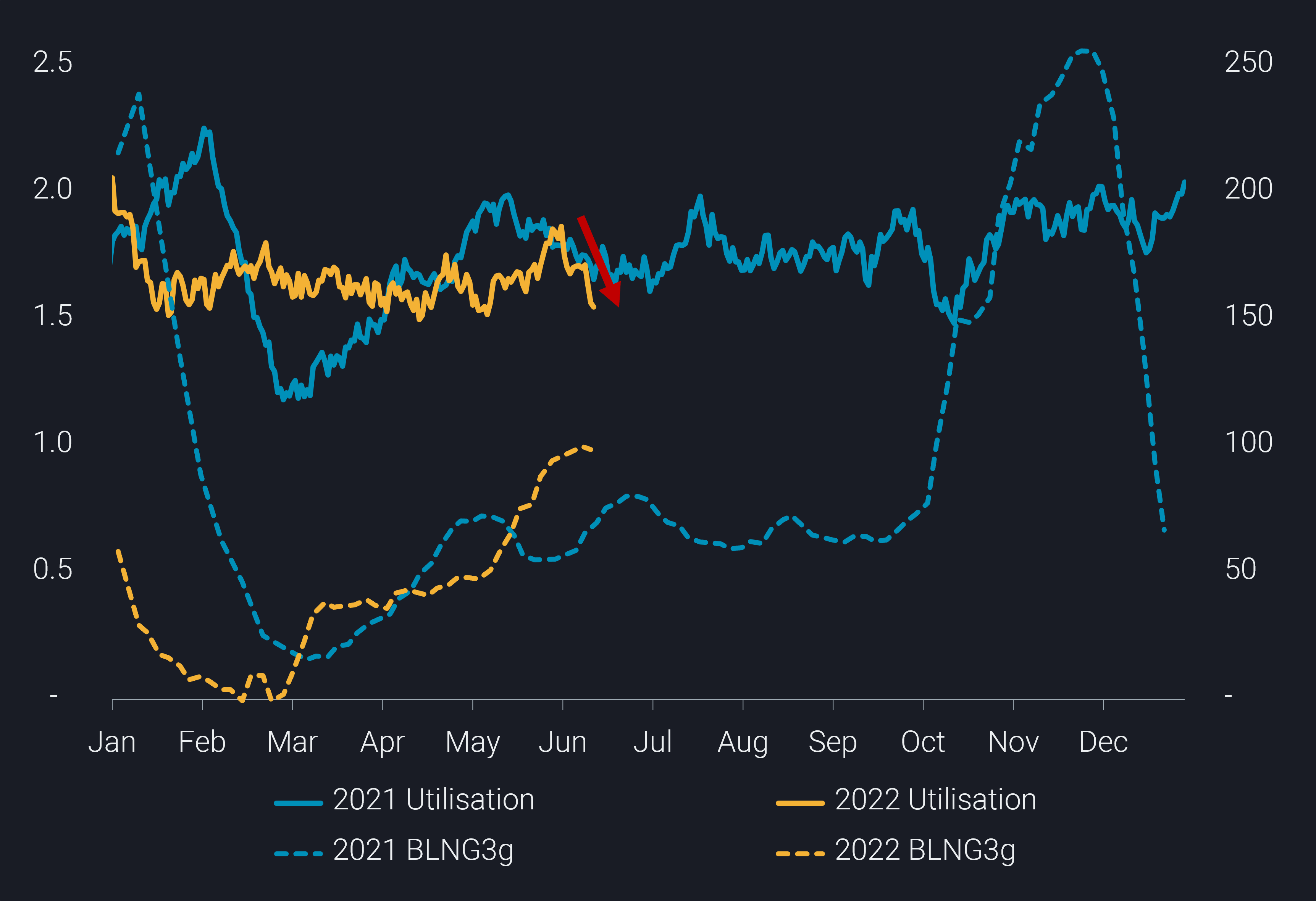

LNG tonne-miles originating from the US (billion, LHS) & LNG freight rate (thousand USD, RHS)

As the global swing supplier, the US has a big impact on LNG shipping

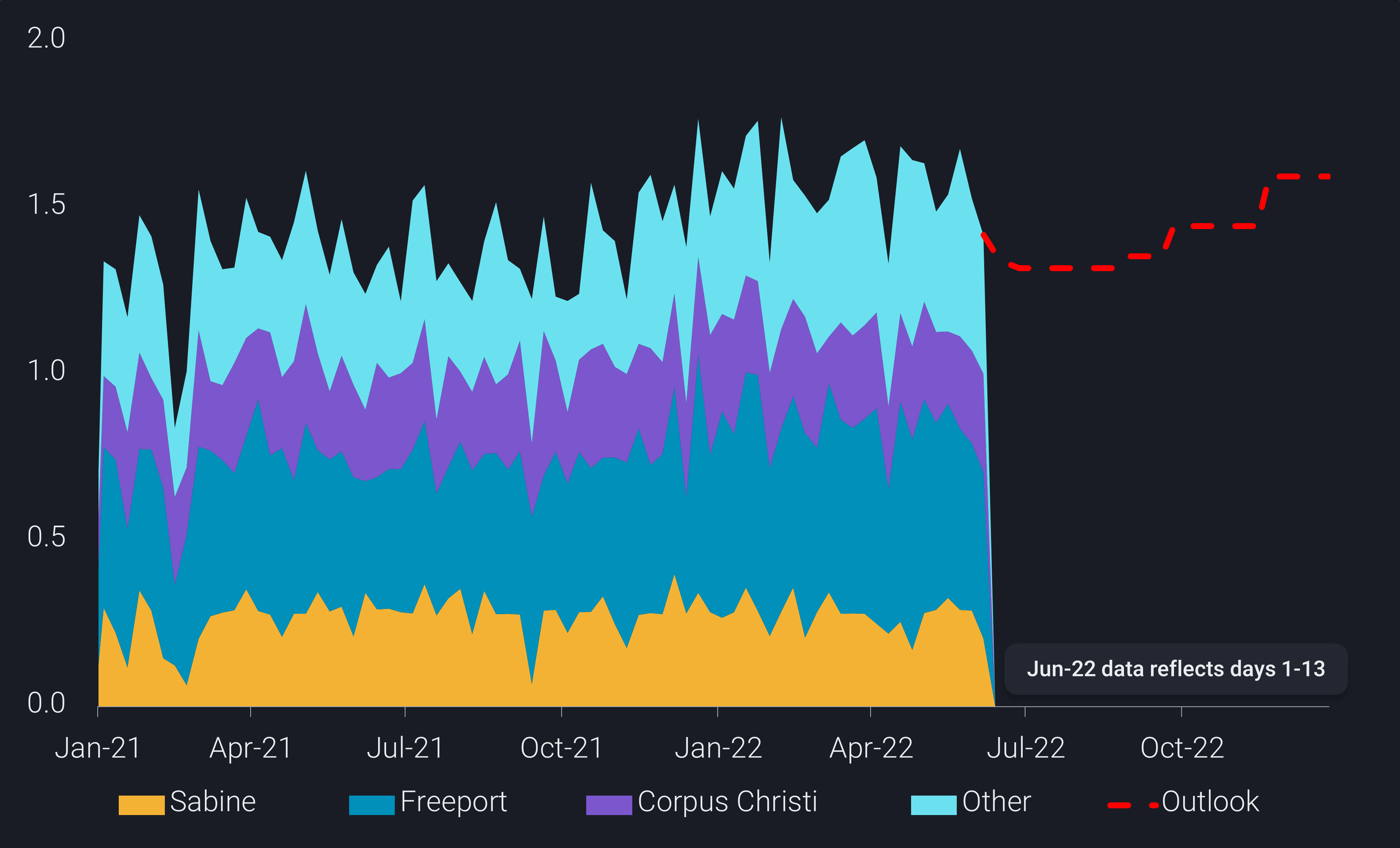

As the ashes settle from the fire in the Freeport LNG plant, the third largest US LNG terminal, a realistic estimate of the impact on exports is coming to light. The operator has indicated that a partial start-up of the three train facility is expected by September but the facility would not be back to full capacity by the end of the year. The loss of 20 cargoes per month, which accounts for 18% of US total exports, is material to the market, especially as Europe diversifies its gas imports away from Russia. The latter is on its own intent incrementally curtailing pipeline supplies to its biggest market, gathering huge profits on the oil export side in spite of various sanctions and booming logistical costs.

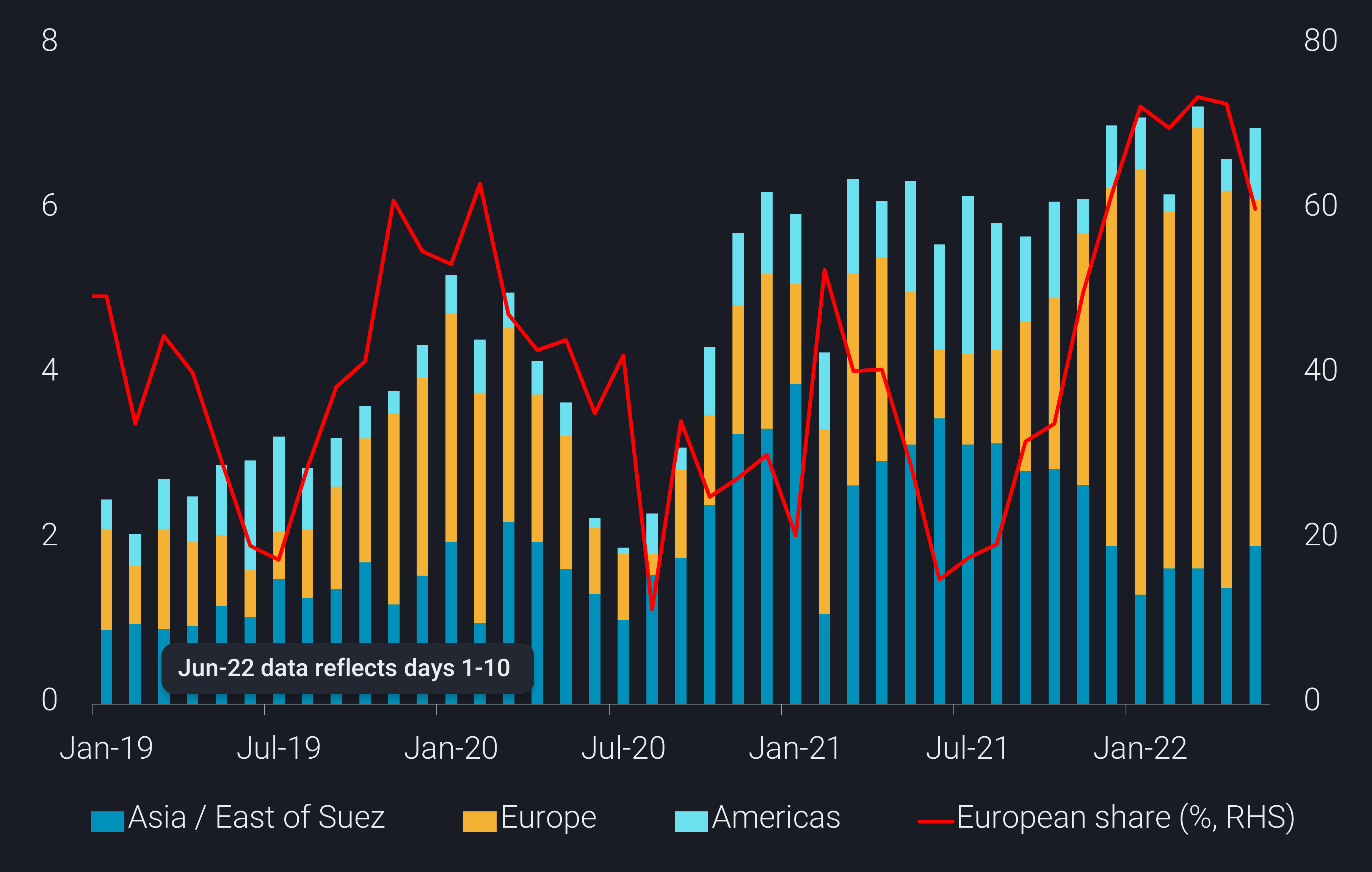

US monthly LNG exports by destination (mt, LHS) and percentage of European share (%, RHS)

In the first five months of this year, close to 70% of US LNG cargoes were discharged in Europe, compared to 37% in Jan-May 2021 as well as on average over 2019-2021. In comparison, slightly above 50% of the US LNG supplies targeted Asia over H2 2020 and 2021. The outcome of this shift is much shorter voyages for the average US LNG shipment so far this year. However, there are early signs that more US cargoes will head to South America and Northeast Asia during the summer months. The longer voyage will further increase the tonne-mile demand on the global LNG fleet, which has the potential to partially offset the length created by the Freeport LNG outage.

The uncertainty around the restart of Freeport is leaving lifters with challenging decisions for their fleets. Initially many players held onto vessels, hopeful of gaining cargoes once the partial start-up began in weeks. Now the wait is several months at best, forcing many extra Atlantic vessels into the balance at the same time. As of 13 June, the Baltic Exchange freight assessment has started to drop off for both US to Europe and US to Japan LNG routes (BLNG2g and BLNG3g). A trend that is expected to continue back towards the summer rates in 2021.

The Freeport outage will weigh on the summer spot market but is unlikely to continue into the winter months, as it returns to full capacity. Leaving the factors driving the growing number of charterers taking firm fleet positions still very much present. Hence LNG spot markets are likely to experience liquidity challenges again this winter. This creates a clear case for holding extra vessel length during volatile times, as a precondition to facilitate reliable supply that buyers are desperately seeking.