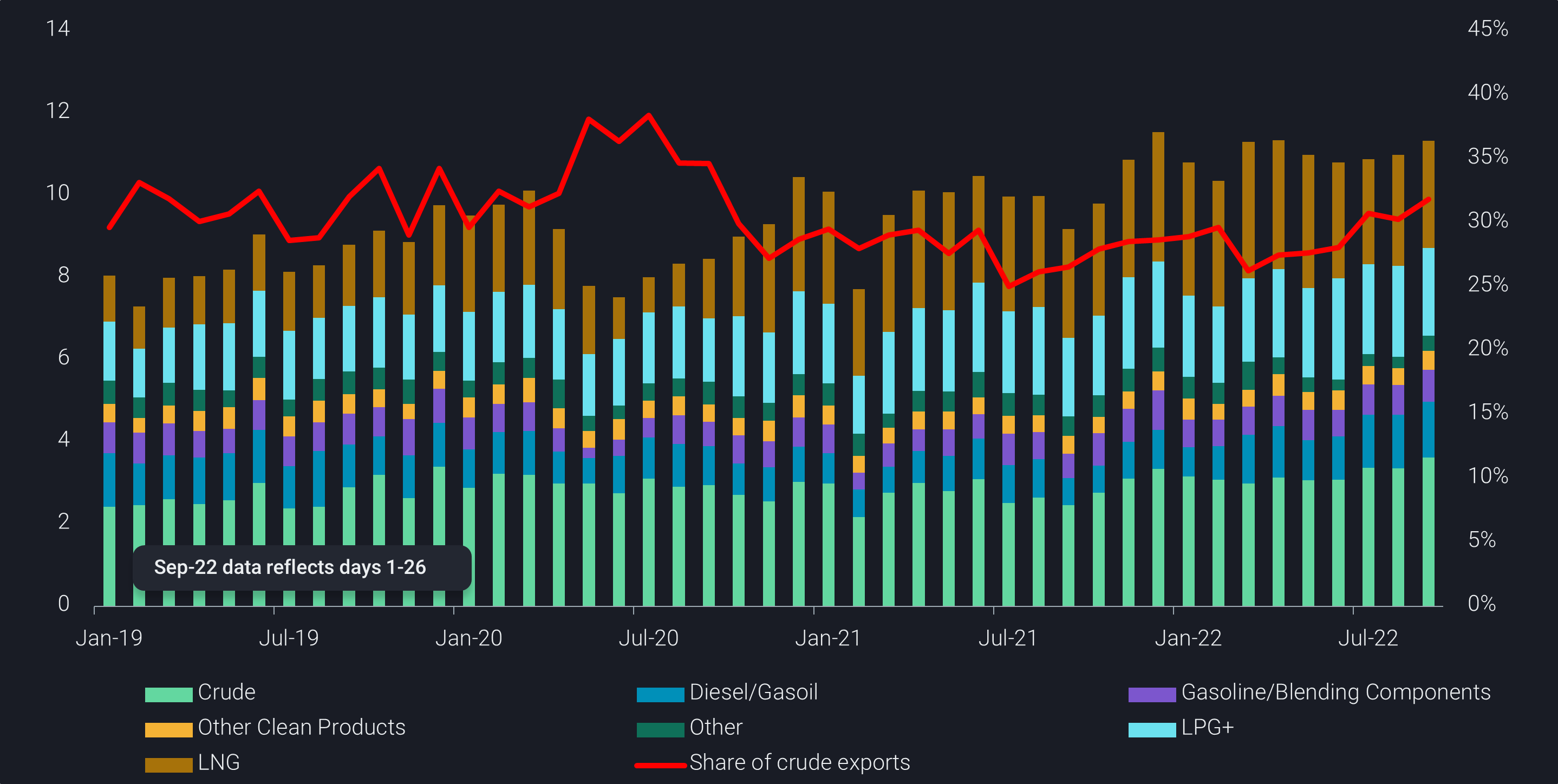

Atlantic Basin CPP supply driven by US export growth

We look at strengthening diesel demand pull from LatAm in a world competing for incremental barrels out of the US with an update on Atlantic basin gasoline and naphtha markets.

Seaborne clean products (CPP) supply in the Atlantic Basin is becoming increasingly supported by the US, with diesel being a sharply growing contributor to the nation’s wider energy exports. Rising demand from key consumers in Latin America and Europe – the latter seeking replacement barrels for Russian diesel – has paved the way for higher PADD 3 seaborne refined product exports, despite domestic diesel stocks at critically low levels.

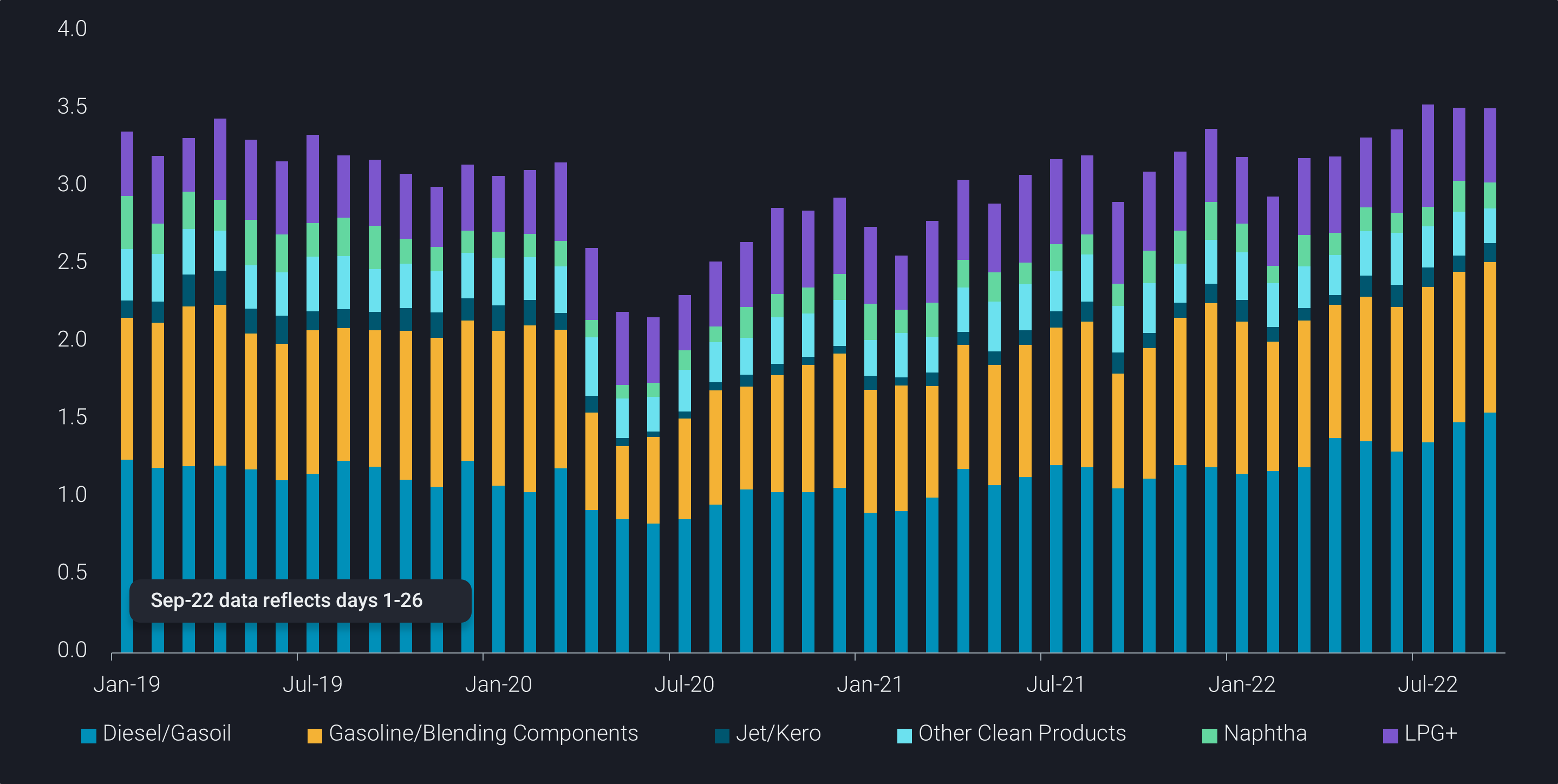

Agricultural and power generation driving Atlantic Basin diesel demand

LatAm import demand for diesel has been increasing since June and we expect industrial demand, a strong harvest season and power generation needs to pull further on PADD 3 diesel supplies despite LatAm refineries running at multi year highs.

Mexico diesel imports have been climbing in three consecutive months ending September due to strong fuel subsidies despite historically high retail prices (Argus) and indications of a slowing economy.

Brazilian diesel imports have surged by 45% in September m-o-m to feed the agricultural sector which is expecting the 22/23 harvest season to attract barrels amid a 14% y-o-y growth due to better crop yields and an increase in areas planted (CONAB, National Supply Company). Improving drought conditions along with hydropower generation means that most of the diesel will be used for farming.

Chilean diesel imports are expected to carry on at the current high levels (Jan-Sept 2022 are 11% higher compared to Jan-Sept 2019) as the country mitigates the ongoing impact of a historically long drought.

Europe has also increased diesel imports from PADD 3 in the four consecutive months to September, giving US refineries a strong incentive to maximize diesel yields in H2 2022 and beyond. US refining flexibility has been proven already this year as US distillate yields reached above 30% multiple times.

Meanwhile, PADD 2 diesel demand was up by 5.2% in September y-o-y (EIA) as agricultural activity begins to pick up for the fall harvest season and refinery utilization in the region falls 5% percentage points below 2021 levels amid low stocks.

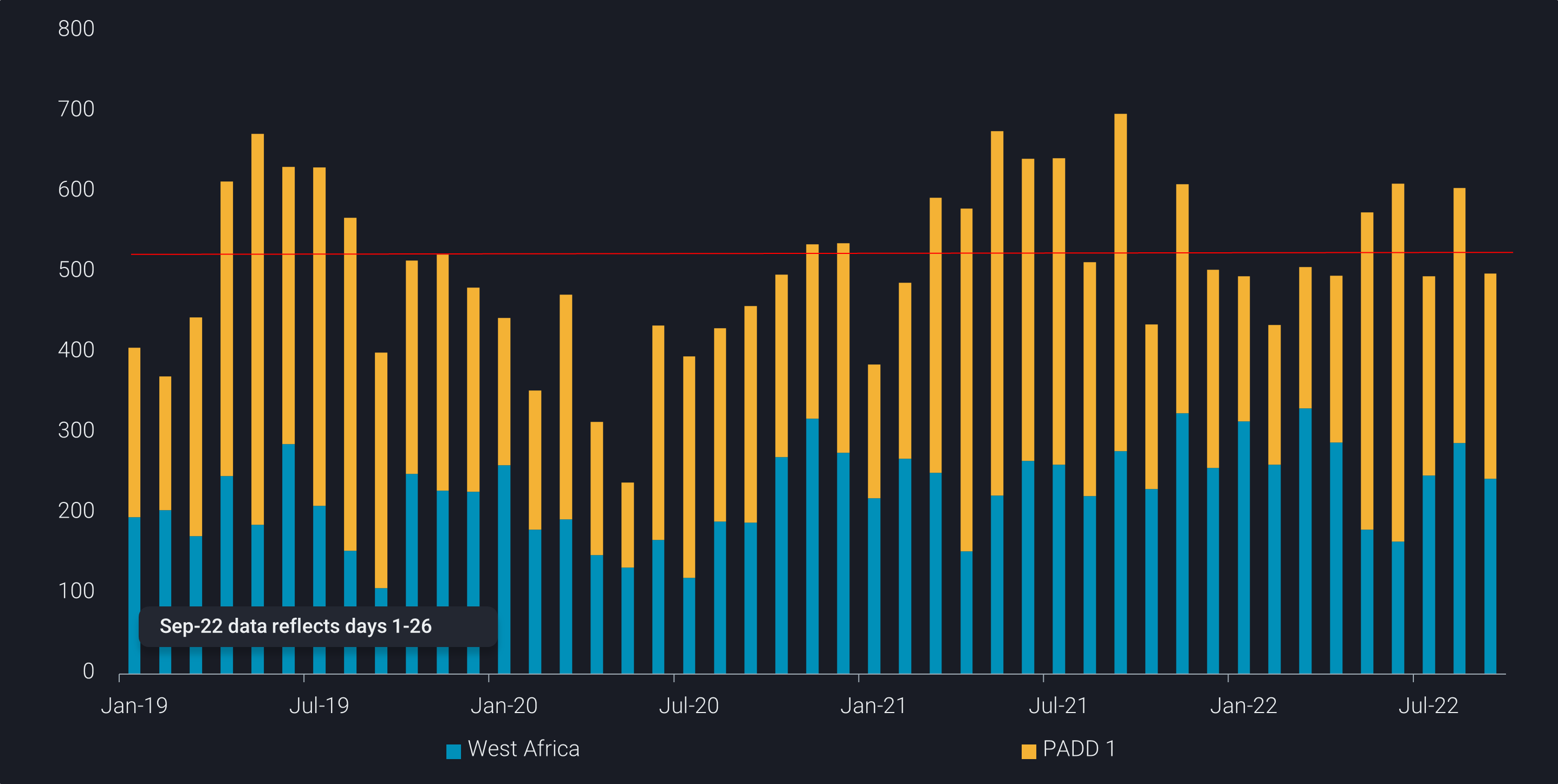

High retail prices in PADD 1 slows demand for European gasoline

While Atlantic Basin diesel imports have been going from strength to strength, gasoline consumption has been hit by high retail prices, recessionary fears and reduced subsidies.

However, since it could be a while before we observe refineries shifting yields away from diesel, we could see gasoline cracks return to seasonal highs in Q2-2023 due to persistent lack of gasoline production coupled with low stock levels in major consuming regions.

PADD 1 seaborne gasoline imports are down 22% Jan-Sept 2022 compared to Jan-Sept 2021. High retail/pump prices have scared off consumers resulting in disappointing demand figures despite historically high ARA gasoline stocks.

Meanwhile the West Africa gasoline market imported 8% more gasoline from Europe Jan-Sept 2022 compared to the same period in 2021.

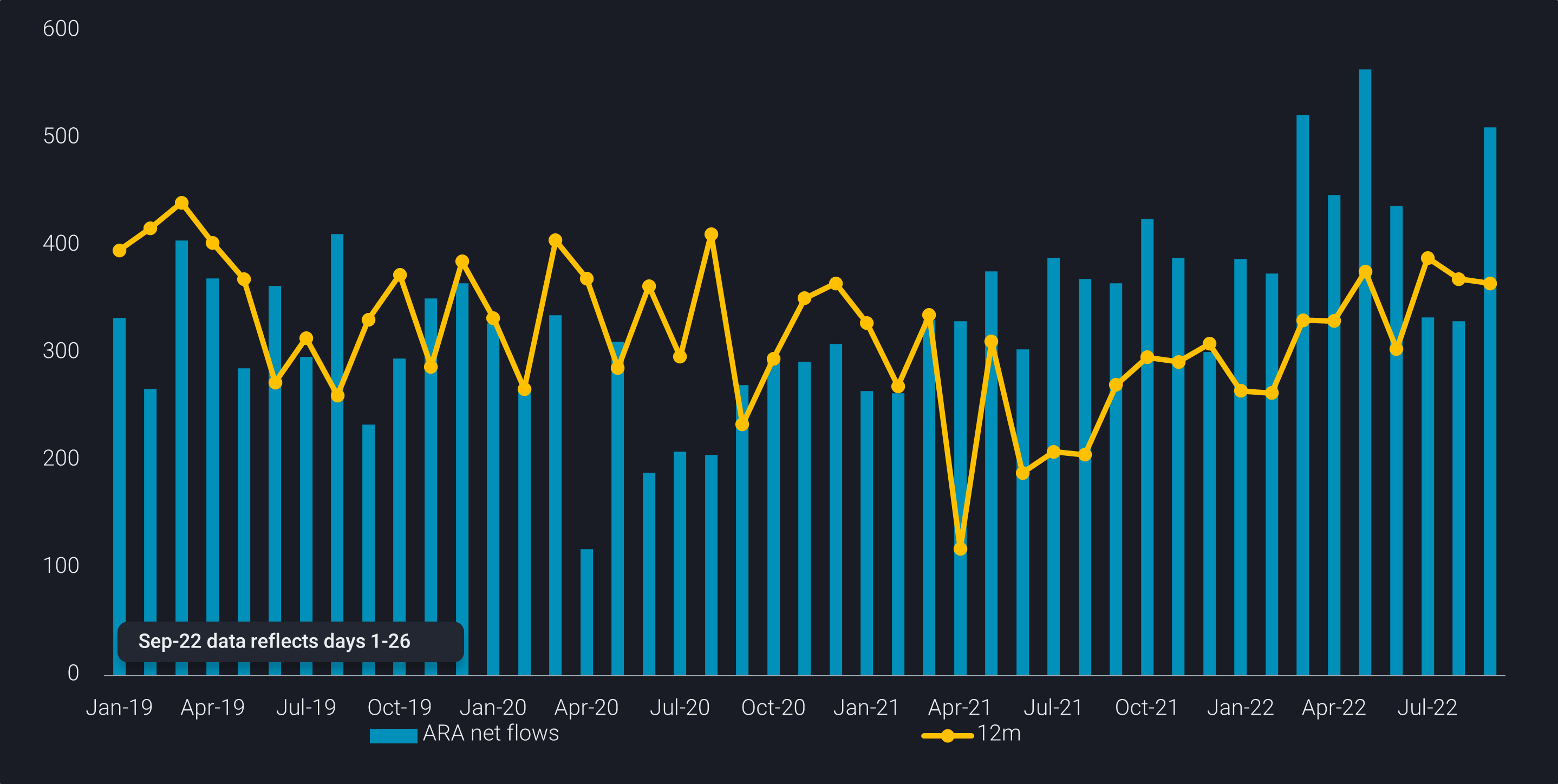

Naphtha surplus continues despite yield shifts

US naphtha cracks may see some support from winter gasoline blending demand and lower global supplies due to the turnaround season. However naphtha is expected to remain structurally under pressure until the Asia petchem sector rebounds. Although South Korea import demand started to pick up in July, cracker maintenance has curtailed seaborne imports which have retreated again in August and September.

ARA naphtha net flows (imports minus exports), a proxy for the net accumulation of naphtha, remain relatively elevated and have increased in September after falling in July and August. The reason for the build is likely due to European naphtha exports having tumbled in September after climbing for four consecutive months as fewer exports head toward Asia. US naphtha exports are slowly rising in September m-o-m, mostly pointed toward Brazil.

Looking ahead, diesel cracks should show a strong performance over the coming months as the world competes for power generation, Russian-replacement barrels (by Europe) and agricultural demand. On the supply side, we expect to see refineries go on planned maintenance coupled with a higher risk of unplanned incidents/outages since refineries have been running very hard compared to historical norms. The biggest wild card is from the East of Suez market, where potentially huge Chinese product export quotas could materialize.