Demand for Russian residual fuel oil grows amid global HSFO tightness

Russia’s residual fuel oil is increasingly coveted amid a tightening global HSFO market with Middle East importing the largest share.

Rising demand for Russian residual fuel oil has been met by limited upside to the country’s exports in recent months, whilst supplies elsewhere could see declines in light of lower sour crude exports from OPEC. The tightening HSFO market has seen VLSFO-HSFO differentials narrowing steadily across major fuel oil trading hubs in recent weeks.

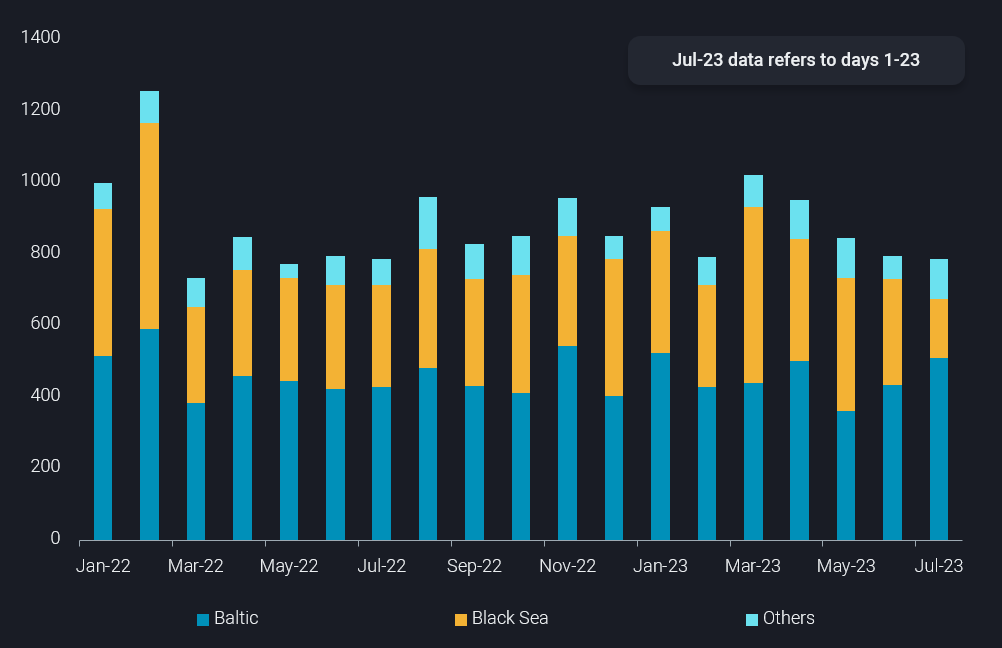

Russia Black Sea fuel oil exports fall amid heightened tensions

Despite slowing refinery maintenance activities, Russia’s residual fuel oil exports in July remained flat month-on-month (m-o-m) at 800kbd, down almost 22% from the peak in March. Amid rising tensions in the Black Sea, several tankers have diverted to load from Russian Baltic instead of Russian Black Sea, leading to a material shift in loading volumes between the two region in July. Russian Baltic residual fuel oil exports have risen almost 16% m-o-m this month (days 1- 23) matching the previous high seen in January, whilst supplies from Russia Black Sea fell to a multi-year low of 165kbd. Consequently, cargoes loaded from Russian Baltic to East of Suez would take at least 11 days longer compared to those from Russian Black Sea, based on Vortexa’s voyage calculator, exacerbating the HSFO market tightness.

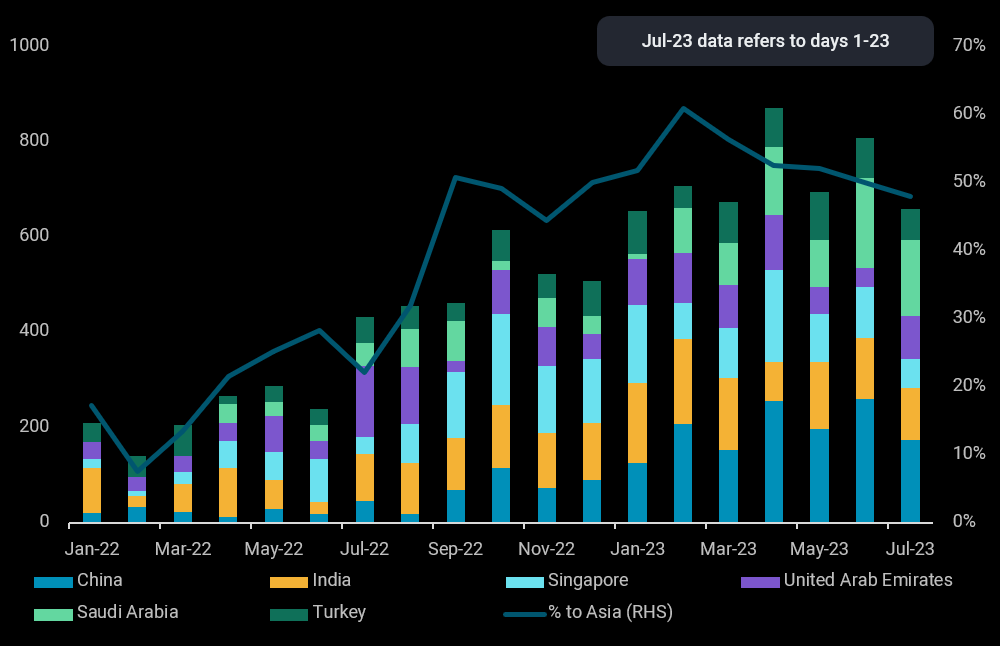

Firm Middle East appetite pulls away Russian supplies from Asia

As summer heat rages on, Saudi Arabia’s imports of Russian residual fuel oil for power generation remain firm and are expected to peak seasonally in August. Higher Russian supplies were also seen discharging into UAE’s Fujairah storage terminals, which could potentially be re-exported, together with a rare handysize cargo arriving in Oman this month. In all, Middle East imports of Russian residual fuel oil are on track to reach a multi-year high of 260kbd this month, accounting for 75% of the region’s total fuel oil imports.

Higher Middle East imports have come at the expense of declines to Asia, which saw arrivals of Russian residual fuel oil retreating by almost 24% m-o-m this month, led by China. Notably, Russian residual fuel oil imports into Zhejiang province, home to the fifth largest bunkering port globally, came to a halt this month after averaging 50kbd in the last two months. Russian supplies to Shandong province, supplementing independent refining operations as secondary feedstock amid crude import quota limitations and vessel inspection delays in the past months, also fell by over 35% m-o-m in July. By virtue of distance, Asia will likely remain the marginal buyer of Russian fuel oil, which means an increase will likely only come after Middle East’s summer heating demand peaks.

Global HSFO tightness to persist amid supply downside risks

Whilst global HSFO demand for power generation, bunkering and refinery feedstocks is expected to remain firm in the weeks ahead, supplies could see declines. OPEC’s crude production cuts are expected to reduce sour crude supplies particularly to Asian refiners, in turn impacting their HSFO production. Additionally, Iraq will be delivering 70kbd of HSFO to Iran for six months starting in August in its oil-for-gas swap agreement (Argus), which will reduce the former’s HSFO exports. In the absence of a rebound in Russia’s fuel oil exports, we expect global HSFO cracks to remain well-supported at least through end Q3.