PADD 3 clean product flows redirect amid sluggish demand

We take a look at the impact to USGC refiners amid a surge of clean product imports from the East of Suez and looming potential start up of Atlantic Basin refining capacity during a time of declining demand in the region.

East of Suez transportation fuel exports (gasoline, diesel, jet) hit a historical peak in March reaching 8.62mbd,10% higher y-o-y with over 2mbd pointed toward the Atlantic Basin markets. Although these volumes began to crowd out USGC refineries as early as 2021 (compared to 2019 volumes), we have seen an acceleration to the tune of around 400kbd since July 2023 amid strong and steady volumes into South America from Russia (red line).

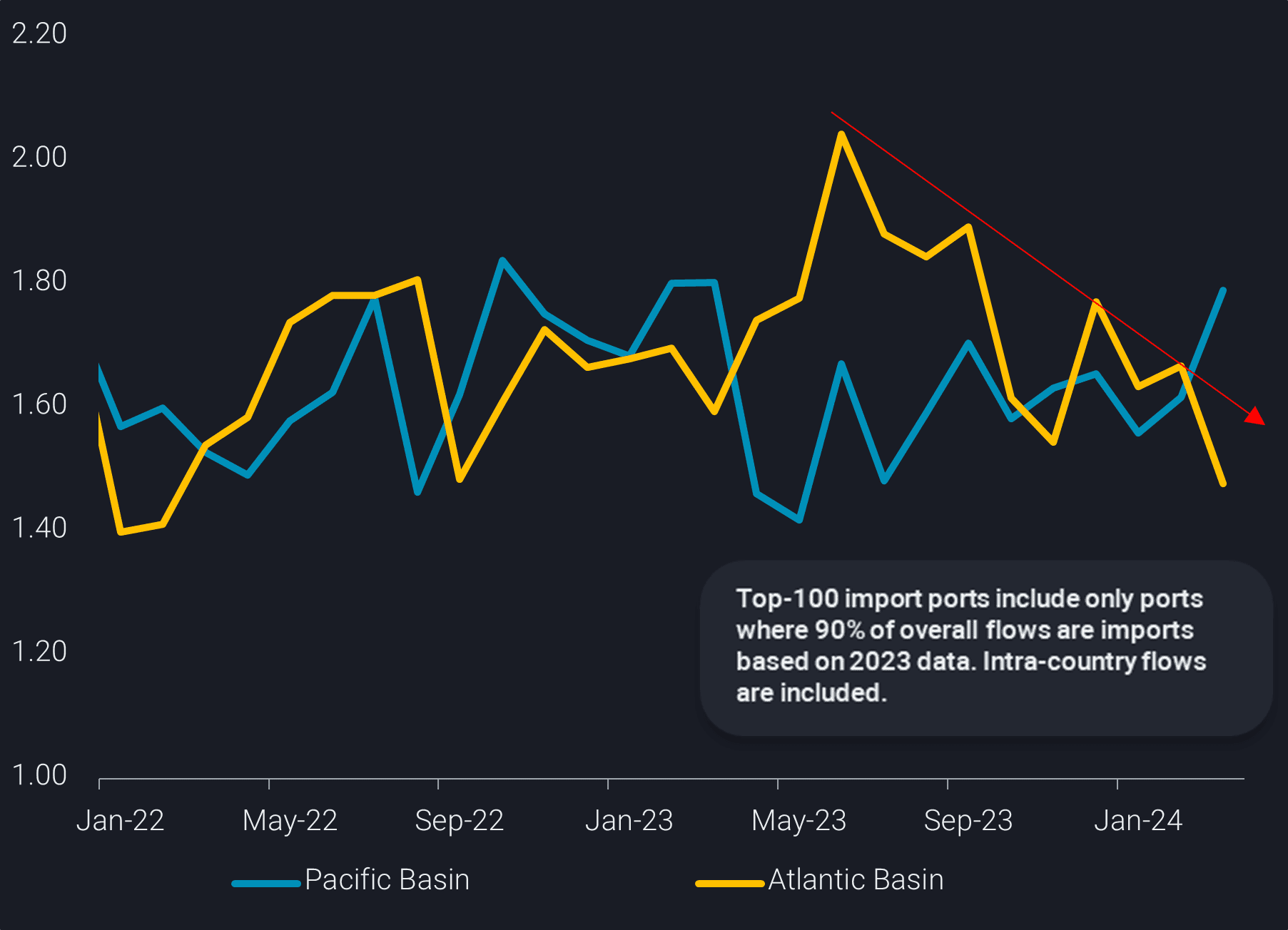

Meanwhile, the demand into the Atlantic Basin continues to drag downward for the main transportation fuels. Using demand indicators measuring ports where at least 90% of imports and exports are imports, we flush out the major trading hubs, and see that overall the Atlantic Basin is a shrinking demand market while the Pacific Basin remains relatively stable.

Gasoline arrivals into select ports in the Atlantic Basin have plummeted 30% overall since their peak in June 2023. While the fall in gasoline arrivals can be partially explained by the removal of the Nigerian gasoline subsidy in Q2 2023, we can also see sharp declines in USAC where gasoline seaborne import demand fell for almost nine consecutive months since peaking in June 2023.

And although the decline in diesel demand into the Atlantic Basin has been more gradual, it continues to slide downward for relatively the same period, with Brazil as the main culprit.

Where does this leave PADD 3 clean product exports?

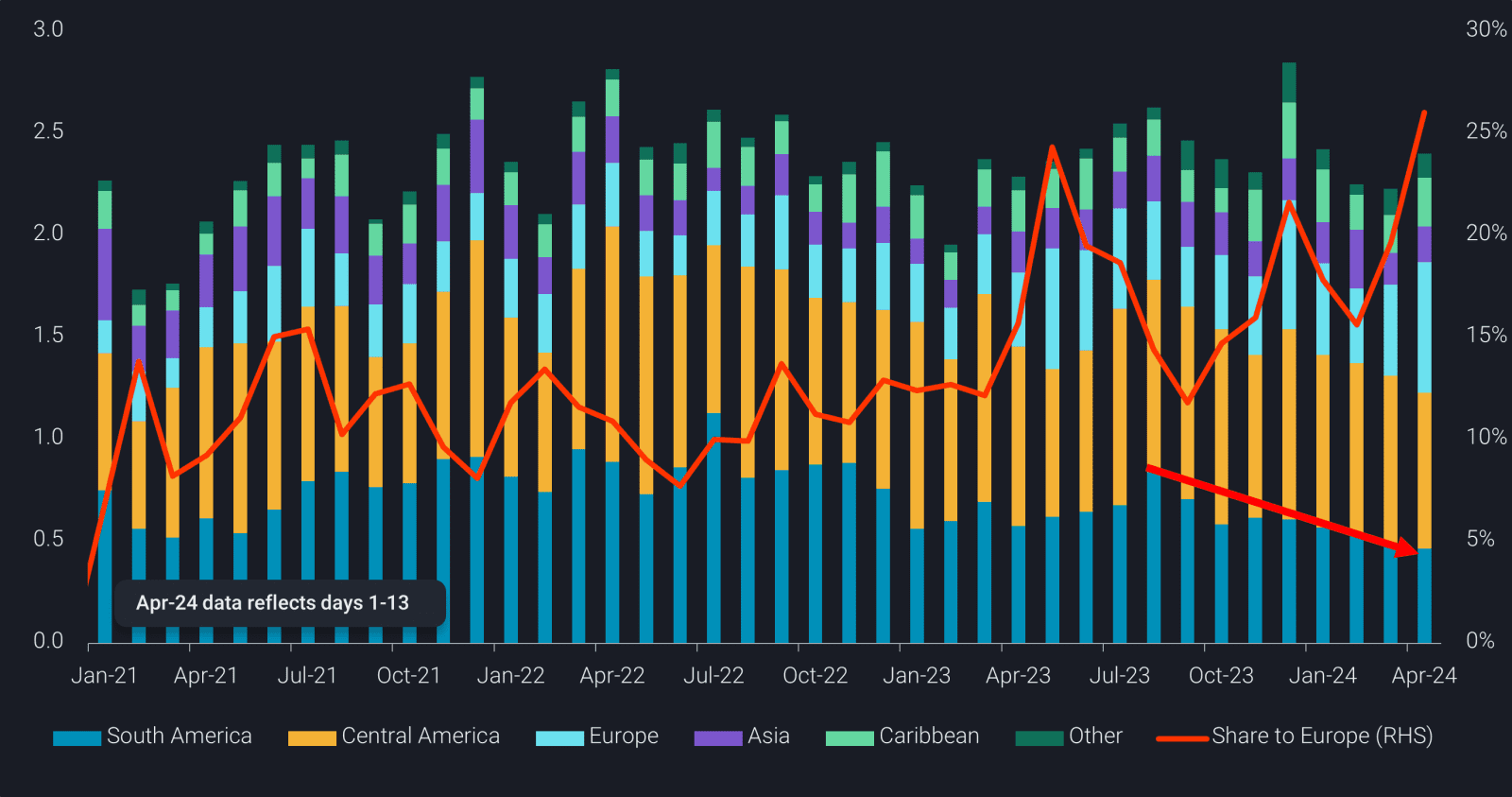

Even with the consistent demand downturn for PADD 3 seaborne clean product exports since 2019, total clean product exports (excl. LPG) have only decreased by 4% from 2.6mbd in 2019 to 2.5mbd in 2023. Meanwhile, exports headed from PADD 3 toward America’s West Coast have dropped 50% in March 2024 since peaking in May 2022. Panama Canal constraints have interrupted USGC flows to America’s West Coast in addition to lower diesel requirements into PADD 5 due to the replacement by renewables.

There has however been a recent surge in diesel flows into Europe which have bumped up PADD 3 exports by 150kbd Jan-Mar 2024 compared to Jan-Mar 2023, a flow that may well continue considering the marginal Middle East barrel has become more expensive due to the rerouting of cargoes around the Cape of Good Hope.

Despite this outlet to Europe for diesel giving some relief to USGC refiners, looming over the horizon are the start up of two massive refineries in the Atlantic Basin; Dangote, Nigeria (650kbd) and Dos Bocas, East Coast Mexico (350kbd) with the potential to produce 500kbd of gasoline. If these refineries come online and start producing on-spec products (more likely Dangote than Dos Bocas) this will likely mean more trouble for PADD 3 refining margins.