PADD 3 clean product exports continue above seasonal norms

PADD 3 clean product exports remain above the seasonal average despite a reportedly high maintenance for USGC refiners this February. In this insight we explore factors related to these export dynamics.

PADD 3 clean product exports are showing remarkable resilience to the reported heavy maintenance season in the region, posting a 20% increase for February 2023 (days 1-20) y-o-y and an 11% increase over the seasonal average y-o-y.This increases comes despite PADD 3 utilization rates for week ending February 9th falling below 80% after an extended period of high run rates in previous years – 2023 avg of 90.5%, 2022 avg of 93.5% compared to 2019 average of 92% (EIA).

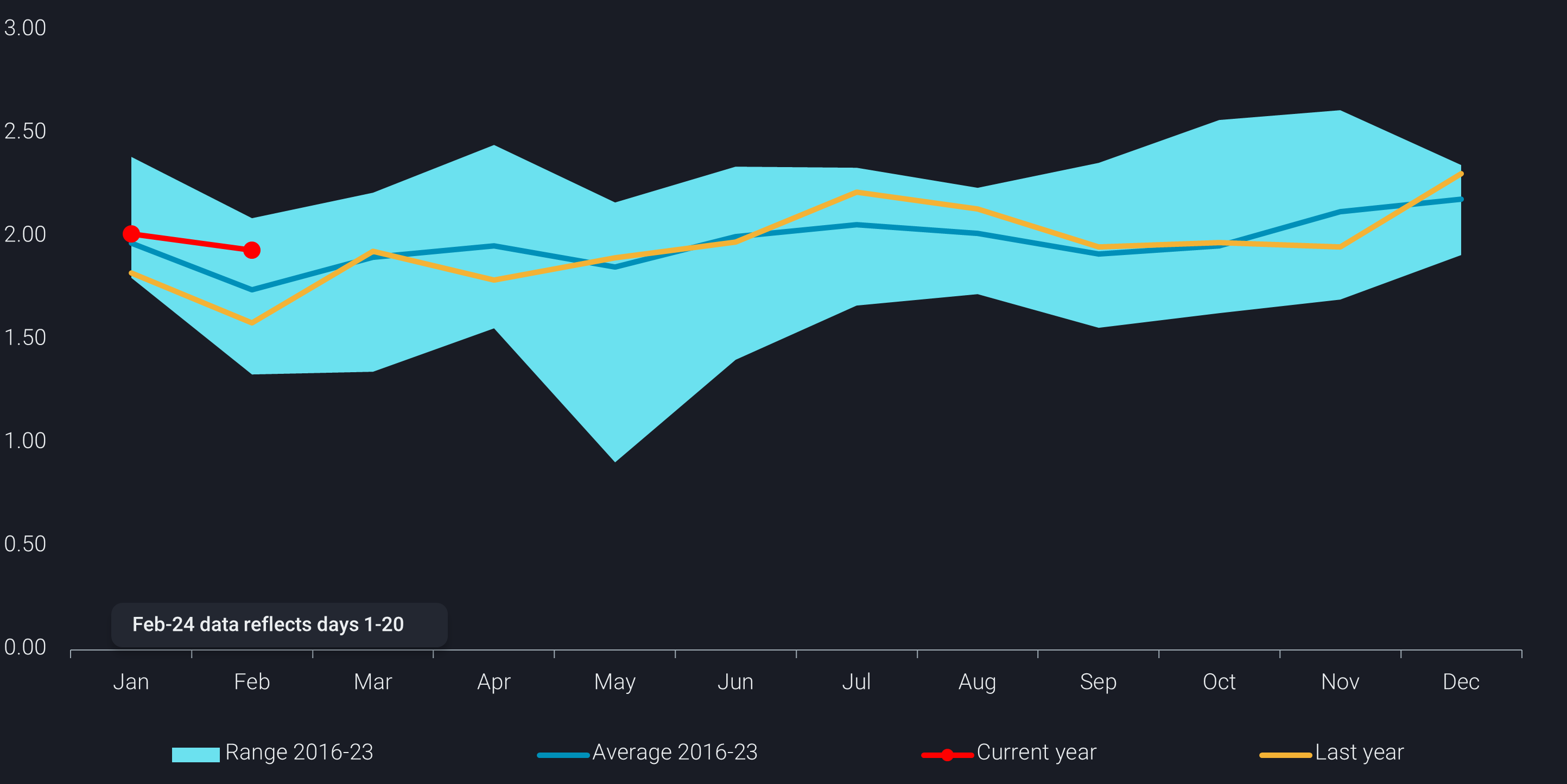

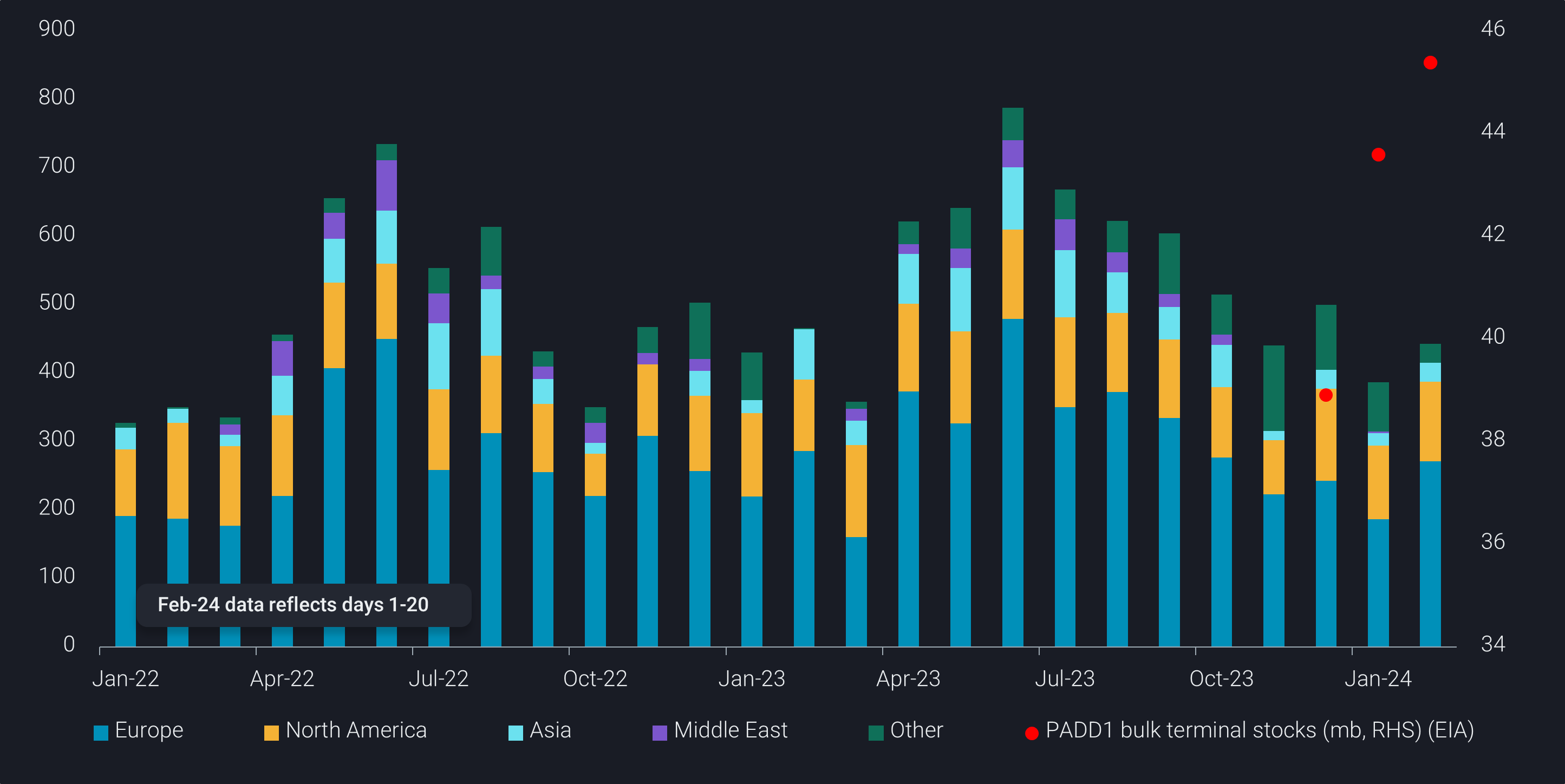

Despite the drop in weekly total PADD 1 gasoline stocks (EIA, week ending February 9th) stocks at bulk terminals have been building for four consecutive weeks (EIA). Bulk terminal stocks are used by gasoline suppliers to balance throughput with demand rates, a good indicator of demand and could explain the gasoline margin falling 26 percentage points between Feb 13- Feb 16. We have also observed a 45% increase in PADD 1 seaborne imports of gasoline/blending components from Europe in February m-o-m which has likely led to a build up of stocks.

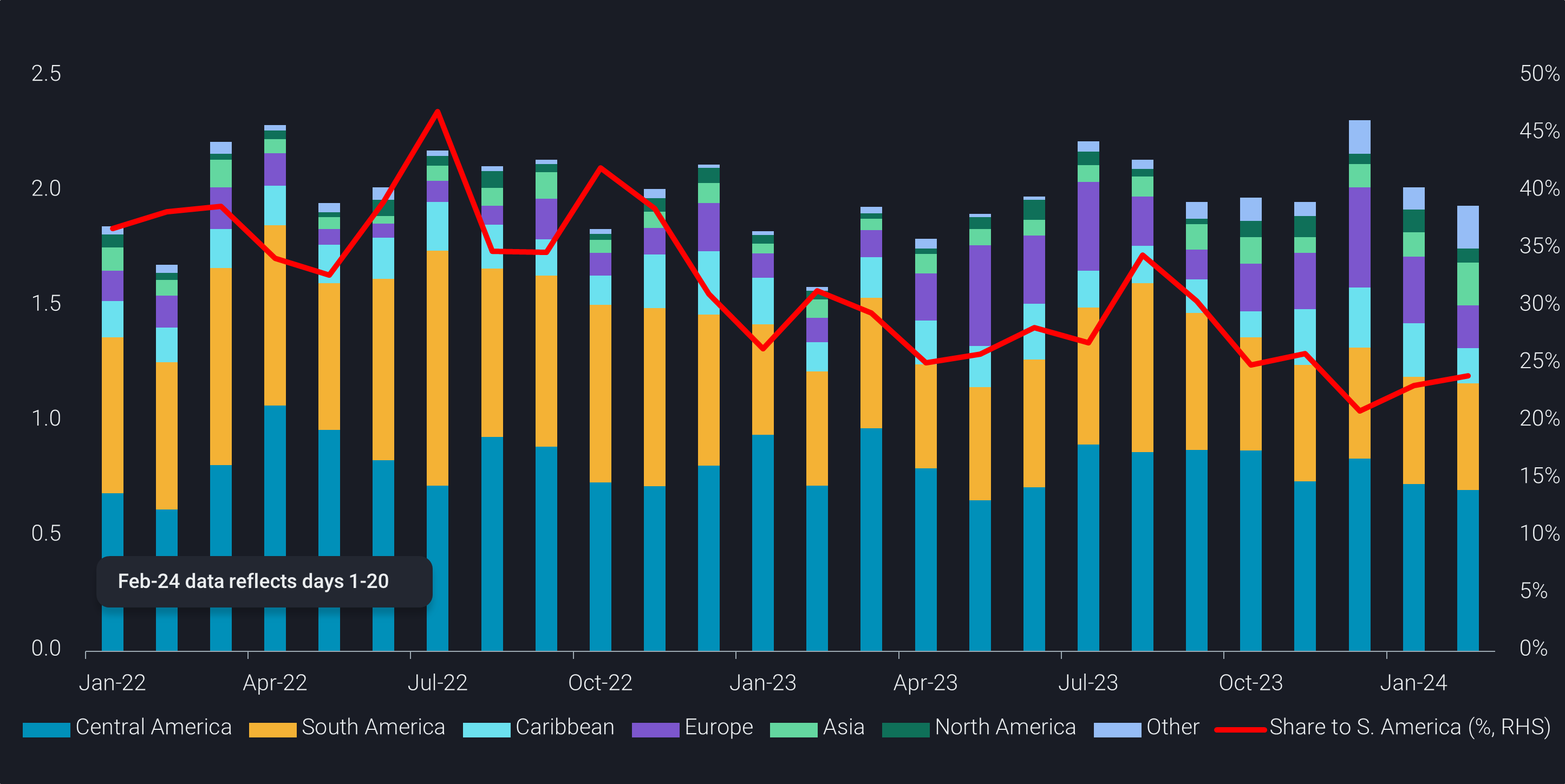

The recent build in PADD 1 gasoline stocks and relatively mild winter are not the only factor at play for PADD 3 clean product exports. We can also see a 30% decline in PADD 3 cpp exports destined to South American markets during 2023 compared to the previous year. This looks to be due to reduced demand in Peru and Chile while Russian diesel continues to pour into Brazil backing out PADD 3 exports.

The consistently high clean product exports from PADD 3 has been good news for European countries who imported a five year high of diesel from PADD 3 in 2023. Even West Africa imported gasoline from PADD 3 in July 2023 through January 2024.

And most recently we can see a rise in naphtha exports from PADD 3 hitting 23 month highs, with volumes pointed to Asia seeing nearly doubling m-o-m in February 1-20, likely due to logistical constraints to move Russian naphtha through the Red Sea.

Looking forward, challenges for PADD 3 refiners include the start up of Dangote refinery (650kbd) which could start gasoline production as soon as Q4 2024. However, more of a wildcard due to the large import program will be the start up of the Dos Bocas refinery (340kbd) located on Mexico’s East Coast which is expected to produce 170kbd gasoline for domestic consumption and 120kbd diesel. In 2023, Mexico’s East Coast imported 335kbd of gasoline and 150kbd of diesel which could be a concern, however given Mexico’s history of poorly run and maintained refineries, it would be unlikely for the Dos Bocas refinery to offer surprises to the upside and meet full production targets. As a result expect PADD 3 product exports to remain healthy in first-half of 2024.