Exploring the forces behind the weakness of naphtha prices

A cocktail of rangebound demand, affected by steady LPG+ substitution, and reasonably ample supplies makes naphtha lose out in relative product pricing.

The summer of 2023 has not only brought skyrocketing gasoline and jet/kero cracks, as could have been expected to some extent. Also diesel and even fuel oil prices heated up. Heavy, dirty HSFO surprised by temporarily surpassing ICE Brent (ArgusMedia), as a function of shrinking supplies struggling to meet seasonally supported demand. But one product is left out in the cold – naphtha. The petrochemical feedstock is falling far behind gasoline, offering a massive reforming spread for suitable grades and spare capacity, weighing somewhat on generally very supportive margins. Why is that?

Two evident answers may come to mind first. Petchem demand is probably very poor, while supply is amplified by the huge skew in crude quality in favour of light sweet barrels, with the still reverberating US shale boom (light, sweet crude) and OPEC+ cuts (medium to heavy sour crude) driving developments. Surely these two factors play a role, but they are certainly not telling the full story, with key explanatory factors to be found in global trade flows.

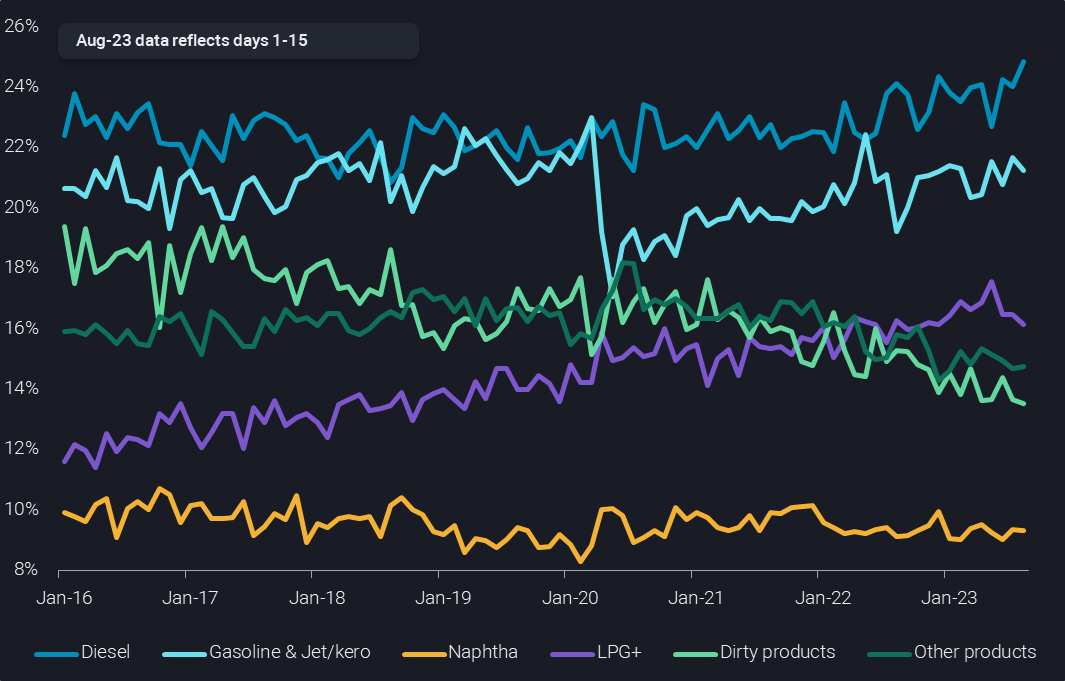

Shares of selected products in world oil product exports (%)

Looking at Vortexa data for world oil product exports shows that the share of naphtha is very stable over time at around 9.5%. Dirty products are steadily declining from close to 17% mid 2020 to 13.7% more recently due to the above mentioned crude slate changes, but also due to regular additions of complex high-conversion refining capacity, especially in China. Over the same period, refiners managed to hike diesel and combined gasoline/jet/kero supplies by about 2pp each. Accordingly, crude slate changes may have facilitated higher production of transportation fuels at the cost of residues, but there is not really an indication that naphtha supplies (yields) have increased meaningfully.

In a crucial development, the share of LPG+ (including ethane) in total product exports rose by nearly 5pp from 2016, largely thanks to massive US supply additions. All these additional barrels needed to secure outlets by eating away market share from other products, including in particular the feedstock market in the petrochemical industry – at the cost of naphtha. This is surely a major factor in poor pricing of naphtha relative to refined products. One could even go as far as to say that naphtha pricing should not be considered in the context of refining economics and crude prices (type of cost based), but rather in relation to LPG prices (demand and substitution based).

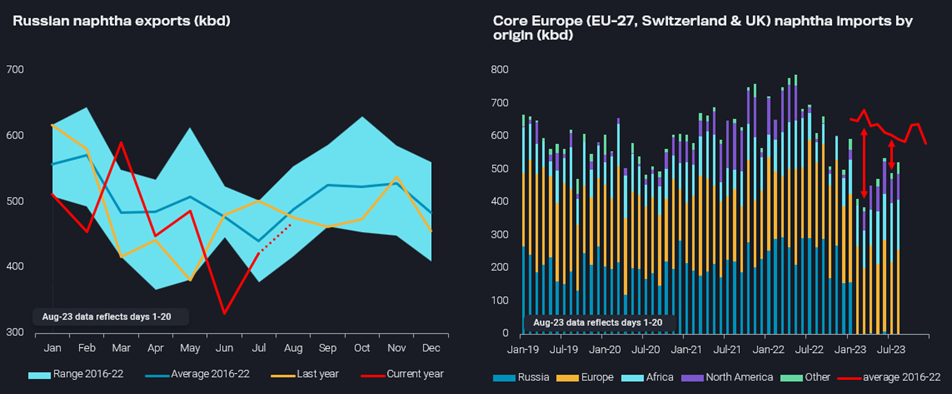

At the same time, various short-term trade flow indications are neither speaking in favour of the light distillate. Russian naphtha exports appear to have recovered somewhat over July and August and have generally not been far off the seasonal norm since March (see left-hand chart above). Meanwhile, European players managed to get replacement supplies for the lost access to Russian naphtha over June-August, quite in difference to the situation earlier in the year (see right-hand chart above). Algerian and US supply came in to meet peak summer gasoline blending demand, which is now expected to taper off slowly but surely.

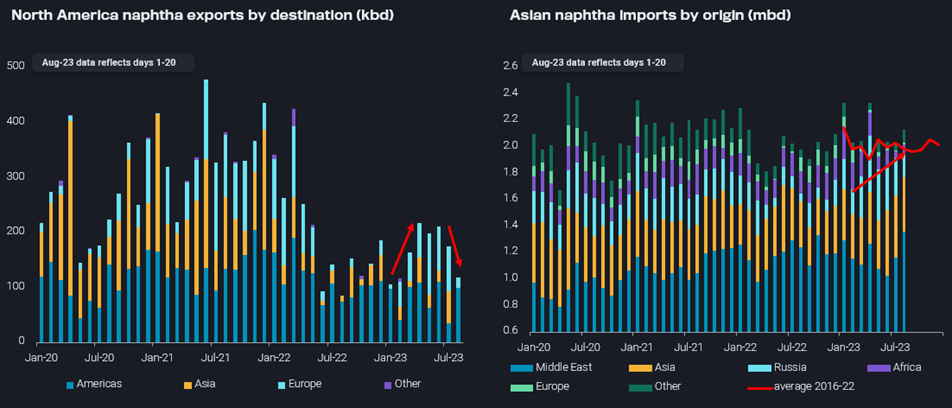

Over in Asia, naphtha imports have actually marginally outpaced the seasonal norm over 2016-2022 so far this year (see right-hand chart above), somewhat questioning poor demand perceptions. However, regional buyers could increasingly fulfil nearly all their needs by making use of just three sources, regional Asian supplies, growing imports from the Middle East, and the stranded barrels from Russia largely stunned in the Atlantic Basin.

As a consequence of otherwise amply supplied Asian markets, US, African and European exporters have largely lost access to the No1 import market. This is allowing for an easy match of European needs and incentivising US players once again to largely refrain from exporting the light end. North American exports may well fall back to the low level of around 100kbd in the remainder of the year, similar to H2 2022, but only a third of 2021 levels (see left-hand chart above).

Looking forward, not much speaks for significant improvements in naphtha pricing relative to refined products, especially in a more bullish crude price environment. In line with the comments above, it may be stronger LPG prices over the winter season that come in as a helping hand, rather than refining economics.