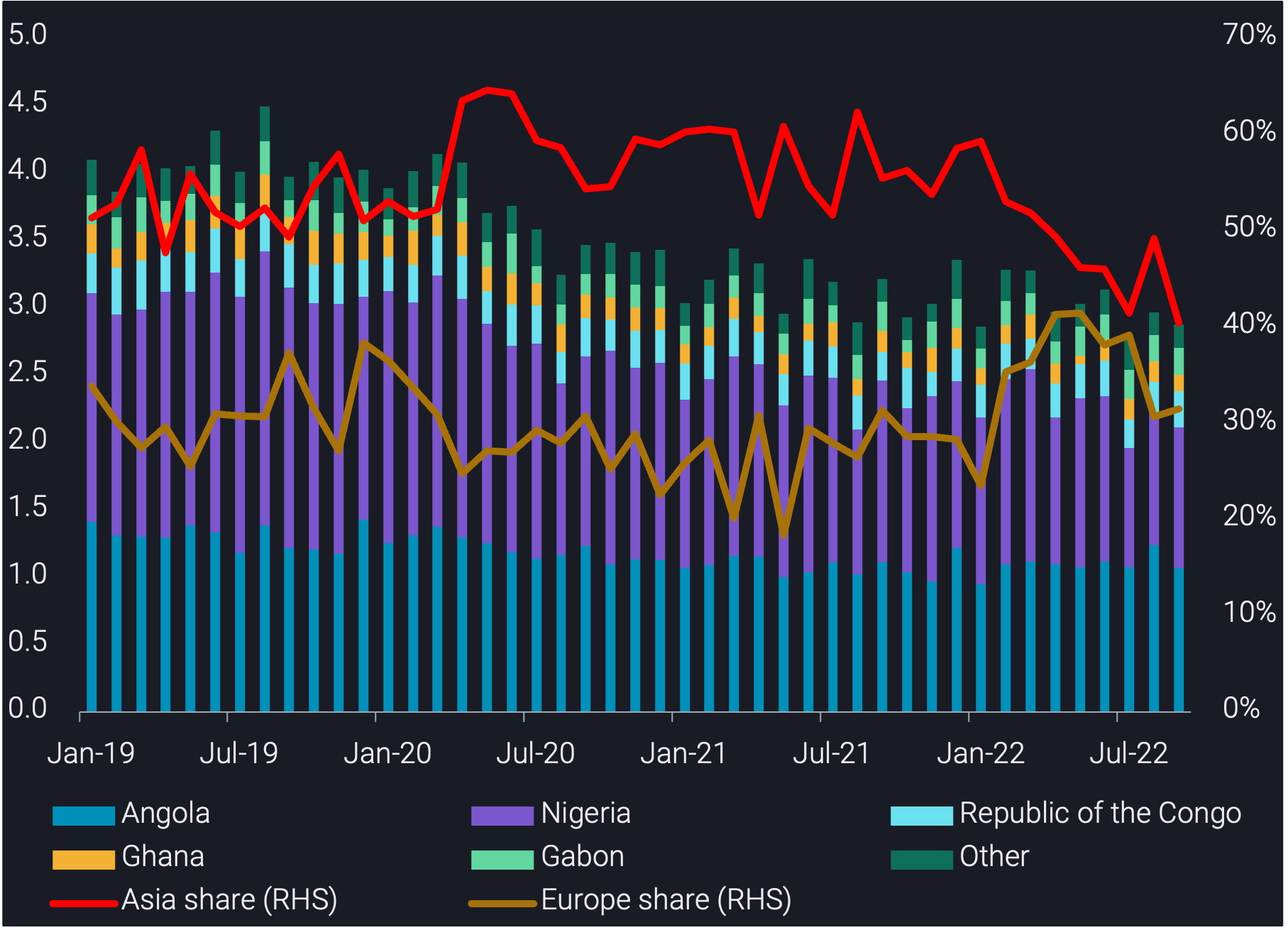

Angola overtook Nigeria as West Africa’s largest crude exporter in Q3 2022

In this insight we explore the redirection of West African crude flows to Europe from Asia and how the combination of shrinking exports and production capacity issues in Nigeria has promoted Angola to being West Africa’s largest crude exporter.

West African crude exports totalled 2.9mb in September 2022, edging lower from August but an uptick from record lows of 2.75mb in July. This slowdown in West African crude exports, which were 175kbd below the 12-month average, was driven largely by Nigeria’s declining export capacity and crude production.

The share of West African crude exports to Asia declined by 9 percentage points between January to September 2022, compared to the same period in 2021, sitting at 40% in September. The volumes instead diverted to Europe, as European refiners replaced lost Russian Urals and consequently turned to other Atlantic Basin crudes, including sweeter West African grades – which would have the knock benefit of relatively lower refining costs.

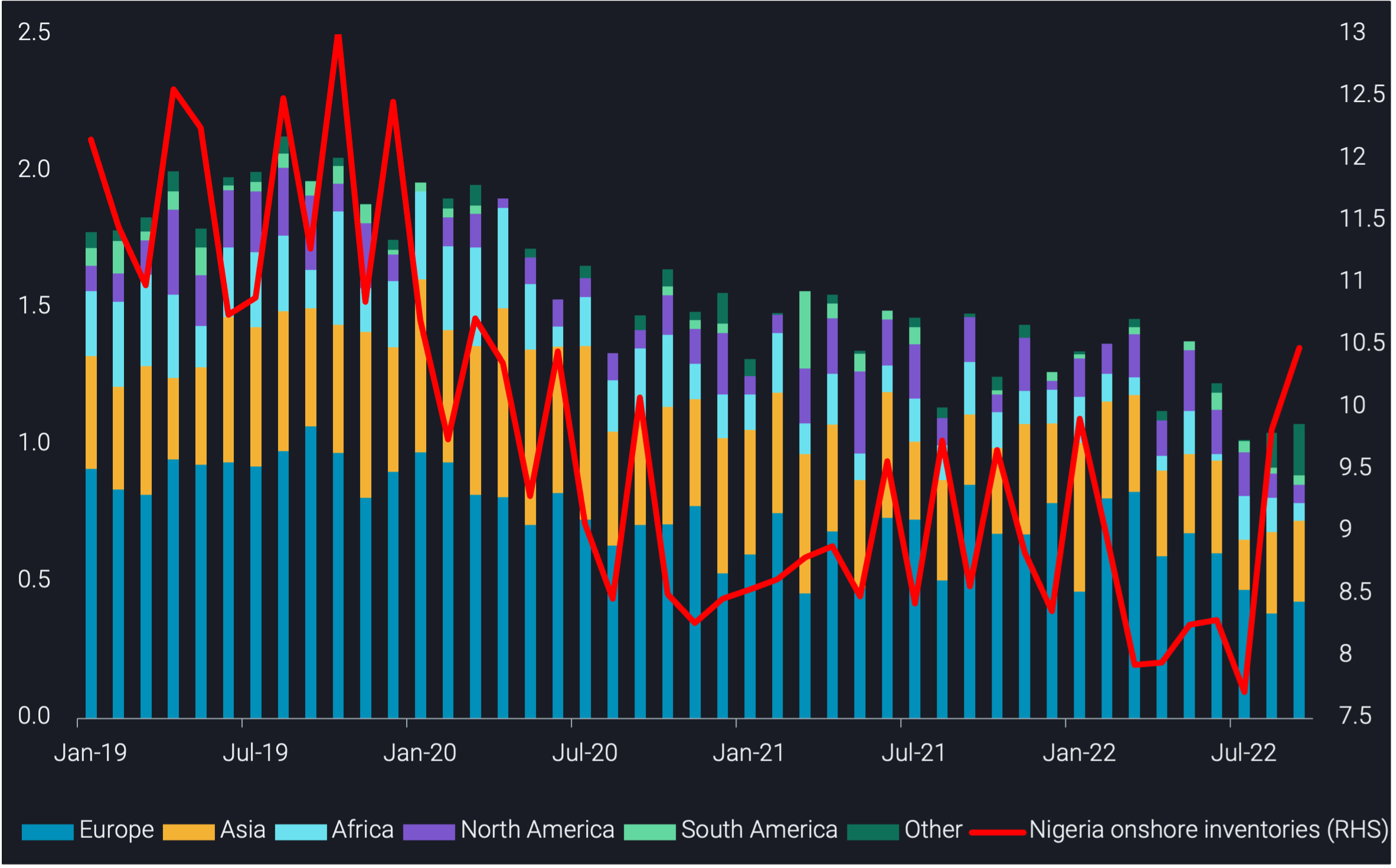

Nigerian crude exports decline, onshore crude stocks build

Nigerian crude exports totalled 1.1mbd in September 2022, close to a very weak Q3 2022 average of around 1mbd. This decline was driven by three factors:

1. Shutdowns at Nigeria’s Forcados and Brass terminals due to repairs – the former responsible for exporting Nigeria’s largest crude stream of the same name (Argus Media).

2. The Trans-Niger pipeline, which transports 180kbd of crude to the Bonny Export Terminal, has ceased operations due to crude theft (Bloomberg).

3. Lower Nigerian crude production due to structural underinvestment, coupled with crude theft. Production declined to 1.1mbd in August (OPEC), a 25% decline from 6 months earlier.

As Nigeria’s exports have declined, we also see a rise in Nigeria’s onshore crude inventories – up by nearly 3mb since August 2022 to a two year high of 10.5mb (as of 1 October 2022).

As an alternative to Forcados, Nigeria has focused on exports of other key sweet, middle distillate rich grades, namely Egina, Escravos and Qua Iboe. These grades accounted for 380kbd of Nigeria’s crude exports in September, remaining flat month-on-month.

Angola overtook Nigeria as West Africa’s largest crude exporter in Q3 2022

Angola’s crude exports averaged 1.1mbd in Q3 2022, 80kbd higher than Nigeria over the same period. Whereas Angola’s crude exports to China declined 300kbd in September m-o-m, its crude exports to Europe increased 100kbd in September m-o-m, sitting at six-year highs. Nigeria’s declining export capacity, reduced crude production coupled with increased European demand for (sweet) West African grades has resulted in Angola taking the top spot as West Africa’s largest crude exporter in Q3 2022.

The redirection of Angolan crude to Europe is partly a by-product of weaker demand from China and the shift by European refiners looking for alternatives to Russian Urals. Additionally, heightened European demand for sweet grades due to higher natural gas prices are incentivising European refiners to cut costs, supporting higher exports to Europe of Angolan grades such as Cabinda, Clov and Pazflor. The main destinations for Angolan crude in Europe are Netherlands, Italy and France.

However, Angolan grades are facing price pressure as they compete increasingly with light sweet crude from Libya and falling (but still high) US crude. This is reflected in their declining premiums to North Sea Dated (Argus Media) – Cabinda and Pazflor were assessed at $1.55/bl and $1.61/bl as of 30 September 2022, respectively, down from $3.75/bl and $3.43/bl on 30 August 2022, respectively.

Outlook

Looking ahead, total West African crude exports will remain capped as Nigerian exports continue to contend with export and production issues. As a region, West Africa will have to remain competitive for high volumes to continue flowing to Europe. European refiners have been largely successful in their efforts to find alternatives to Russian Urals and could pivot marginal supply to other Atlantic Basin producers or even the Middle East. Should large Chinese product quotas for the Q4 2022/Q1 2023 materialise, that could also intensify competition for West Africa crude.