CPP floating storage: Taking stock

CPP floating storage: Taking stock

The global explosion of floating storage after the onset of covid-19 and the crash in global oil demand was not only concentrated to crude oil, but also led to dramatic changes across the refined products spectrum. This insight reviews the subject of clean petroleum products (CPP) floating storage, and namely its three main components gasoline, diesel and jet fuel. How are offshore floating storage volumes for these products faring globally, and what regional dynamics can we see?

The Global Picture

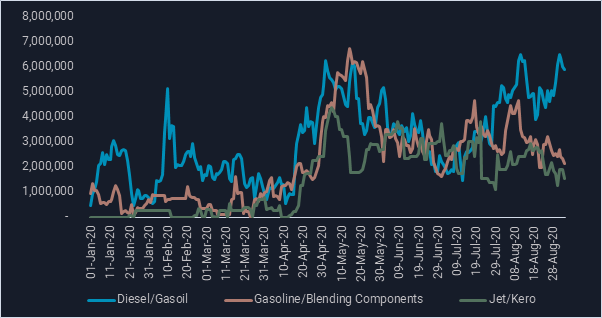

Now approaching the end of the third quarter, we can say that the market has passed the peaks in CPP floating storage seen in April-May (see chart). While another a future rise cannot be completely discounted, the recent high of almost 100mn bbl (combined CPP floating storage) is highly unlikely to be seen again, and highly unlikely to rise in such a sudden manner.

Global key CPP floating storage volumes (bbl)

See this in the Vortexa platform

Lingering CPP floating stocks

Nevertheless, there remains a significant volume of CPP still floating offshore around key demand centres.

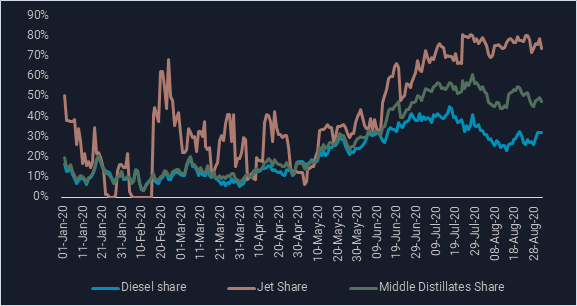

- As of end-August, diesel held the top spot for the most widely stored CPP product across the global tanker fleet. Around 25mn bbl of diesel was seen in floating storage globally at the end of August, down by around 40% from the peak volume in mid-May.

- Global gasoline floating storage stood at around 11mn bbl at the end of August, down almost 80% from the peak in May.

- Unlike road fuels, jet fuel floating storage has bucked the trend by climbing over the same period to 13mn bbl, up by 20% from mid-May levels.

- Despite a very slight recovery in air passenger traffic, global jet fuel demand remains sluggish while gasoline has fared relatively better since Q2 – especially upon entry into the summer driving season in the US. As a result, jet fuel has held its position as the second most widely stored clean product across August.

Asia: The early indicator

Back in March, Asia was the first region seen to be accumulating CPP in floating storage, in line with it being the first region to introduce widespread movement restrictions. Since then we saw sharp volatility for floating storage volumes across products in Asia. Volumes wound down between May and July but persistently weak diesel, in key export markets such as India and China, demand has kept offshore inventories elevated.

Southeast Asia & China key CPP floating storage volumes (bbl)

See this in the Vortexa platform

- Diesel floating storage volumes off Southeast Asia and China (combined) are at levels last seen at the peak of demand destruction in early May.

- Around 6mn bbl was observed in floating storage at the end of August, matching volumes seen during early May. Volumes exclude gasoil tankers deployed in longer term logistical floating storage.

- Gasoline floating storage volumes in the region stood at 2.7mn bbl, down by 60% from the mid May peak.

- Jet fuel floating storage volumes have broadly declined since April but still remain well above pre-Covid levels, at just under 2mn bbl (end August).

- The region is unlikely to see a build in offshore jet fuel stocks as traders continue to look to export surplus jet to west of Suez markets.

Europe: The global distillates hub

Over the course of the pandemic, Europe attracted much of the surplus diesel and jet fuel coming from the Asia, Middle East and the US. Subsequently Europe is now home to the largest share of middle distillates floating storage.

But as the European summer draws to a close, the seasonal peak in jet fuel demand for the year has already passed. Meanwhile, large diesel consuming nations – such as UK, France and Germany – are grappling with an economic downturn, curbing import demand.

Under this backdrop, diesel and jet fuel floating storage is unlikely to draw down as quickly as it has in other regions, or at global level. In fact, the share of jet fuel floating storage in northwest Europe and the Mediterranean, as a proportion of the global total, has grown.

North west Europe and Mediterranean floating storage as a share of global total

- Jet fuel held in floating storage in northwest European/Mediterranean waters accounted for almost 80% of the global total at the end of August.

- The region’s share of total diesel/gasoil in floating storage stood at around a 30%.

- Floating storage volumes for diesel/gasoil and jet in the region stood at 6.9mn bbl and 9.7mn bbl, respectively, at the end of August.

- Floating storage volumes for jet in the region peaked at 15 mn bbl in mid-August and for diesel/gasoil at 10 mn bbl in late June.

Gulf of Mexico: Wind down complete?

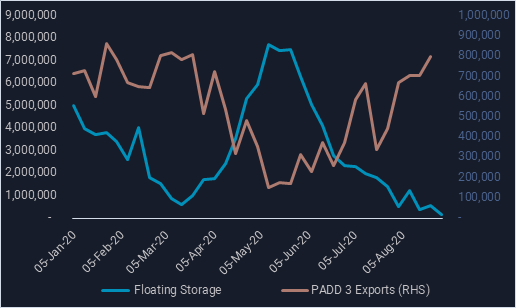

Unlike Asia and Europe, CPP floating storage activity in the Gulf of Mexico has all but normalised to pre-covid levels. During the period of peak demand loss (March to June), the majority of CPP floating off the US Gulf Coast, Mexico and/or the Caribbean was gasoline – most of which struggling to clear into Mexico.

Gasoline floating storage in the Gulf of Mexico (bbl) vs. PADD 3 gasoline exports (b/d)

The arrival of the US driving season, in conjunction with a massive reduction in PADD 3 domestic gasoline output has helped clear offshore inventories (see chart) and is likely to prevent any build in offshore gasoline volumes in the near future.

Looking ahead, one factor to watch in the US is the impact of rising onshore diesel stocks. With EIA reporting distillate inventories at multiyear highs, and limited demand for surplus product into Europe and Latin America, US diesel floating storage volumes could rise.

Interestingly this month will see the arrival of two newbuild VLCCs laden with middle distillates from Asia and the Middle East into US waters, an unusual destination given that previous such cargoes have tended to head to Europe and/or west Africa:

- Newbuild VLCC Hunter Idun is heading towards the Bahamas fully laden with diesel/gasoil originating from South Korea, Qatar and Malaysia.

- Similarly VLCC Babylon is heading to Philadelphia, likely for upcoming ship to ship discharges, carrying a combination of jet and diesel cargoes originating from Oman and Ruwais, UAE.

Want to know more about these flows?

{{cta(‘bed45aa2-0068-4057-933e-3fac48417da3′,’justifycenter’)}}