Dangote refinery ramp up amid oversupplied product market

In this insight we review the current status of the recently launched 650kbd Dangote refinery in Nigeria and its impact on Atlantic Basin crude and product markets.

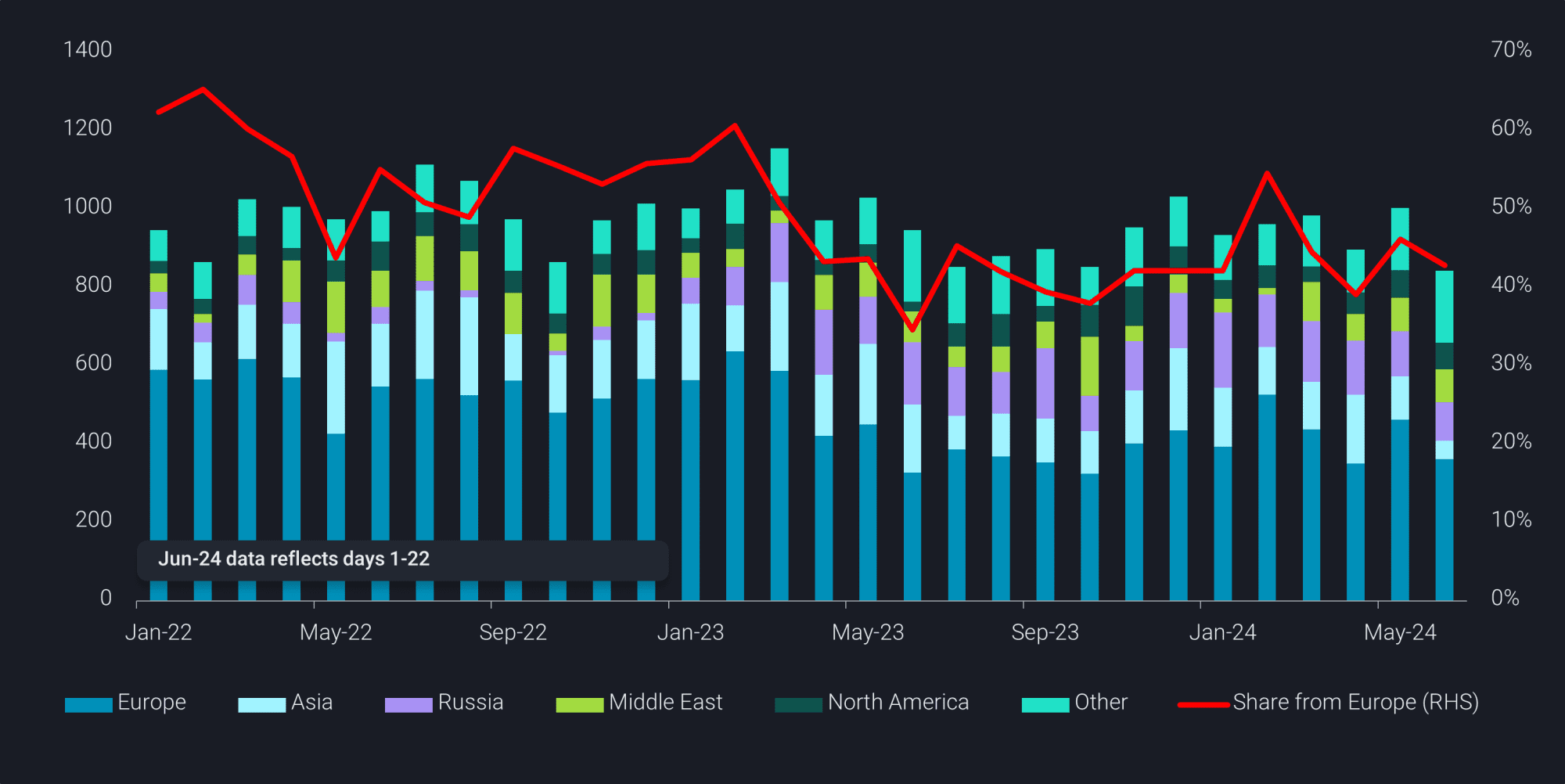

Refinery margins in the Atlantic Basin continue to weaken due to a combination of factors including an amply supplied product market, sluggish PADD 1 gasoline demand and rising exports from PADD 3 (up 10% y-o-y in June).

Already poor Atlantic Basin clean product demand amid the precipice of more supplies coming into the market from Dangote refinery is bad news for refiners on both sides of the Atlantic. West Africa’s clean product demand has historically been dominated by European refiners, so the ramp-up of the Nigerian plant will impact European gasoline exports most, but also diesel, and LPG exports – the latter especially from US refiners.

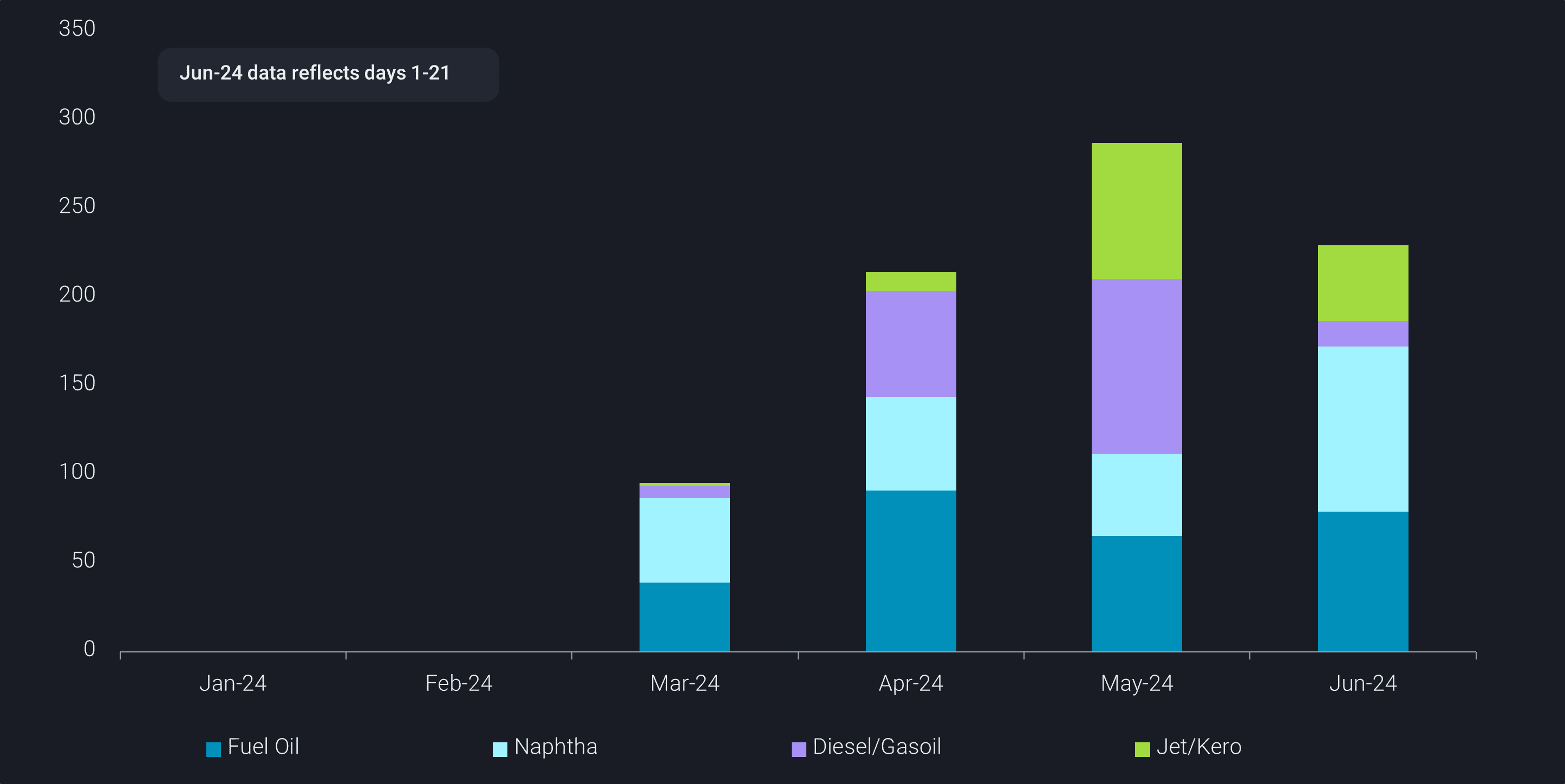

As we move closer to July, the drum roll beats faster especially in anticipation of the long-awaited secondary units which are expected to produce (according to Argus Media) 325kbd of gasoline, 150kbd of diesel, and 55kbd of jet/kero. Most of the gasoline is expected to be retained for domestic markets but the majority of diesel and jet fuel is likely to be exported.

Nigeria tightened the sulphur cap on oil products imports to 50ppm at the start of June (Argus Media) from the 200ppm limit set on 1 March. This move arrives just as Atlantic Basin’s most anticipated new refinery start-up comes to life. A tighter sulphur cap for imports is widely thought to promote the sale of diesel, jet fuel and gasoline from Dangote refinery in the domestic Nigerian market. Dangote refinery is now capable of producing 10ppm ultra-low sulphur diesel production, and 10ppm gasoline production is expected to follow in mid-July.

Latest observations?

Since the start-up of the Dangote refinery, Vortexa data shows five fuel oil cargoes (LSSR) directed to the US (PADD 1 and 3) from March until late April, followed by exports to the Caribbean and Europe in mid-May to the present. However more recently, fuel oil cargoes have been heading East of Suez to hubs such as Fujairah and Singapore.

Meanwhile, naphtha cargoes have also been moving both east and westwards. From the beginning of March to late June, Dangote refinery has exported seven cargoes to Europe, mainly to Antwerp, and five to to Northeast Asia, mostly Daesan, South Korea. Diesel/gasoil exports have predominantly stayed in Africa (55% of cargo volume), with a minimal number of cargoes (5) leaving Africa for Spain and Puerto Rico. Jet cargoes (Jet-A1) remained in West Africa from April to late May, before moving elsewhere within the Atlantic Basin – to Suape, Brazil in late May, and then most recently to Northwest Europe in June, with a steady import volume of 15kbd since April.

Since Dangote refinery’s start-up, its crude imports have exclusively been sweet crude, mainly light, sourced domestically from Nigeria, with 75% of cargoes from ports loading Bonny, Forcados, Agbami, and Odudu, and the remaining 25% has been WTI loaded from PADD 3.

On the subject of logistics, an interesting observation from Dangote refinery exports is that one of the SPMs (single point moorings) at Dangote Offshore Terminal is yet to be employed. This could be seen as a possible indication of the refinery being able to ramp up exports even higher than current levels.

Currently, Nigeria is on track to import 230kbd of gasoline from Europe for the first half of this year and this volume is likely to move lower during the course of this year as Dangote refinery continues raising runs at primary and secondary units. The further the refinery moves along its launch, the more it is a cause for concern for Atlantic Basin refineries.

If existing Atlantic Basin refiners are to supply less gasoline to Nigeria, the demand outlook for other key importers is by no means bright. Mexico, another major global gasoline importer, is showing signs of volatility in its gasoline demand this year due to higher regional refinery runs and the looming start up of the Dos Bocas refinery on the East Coast. At the same time, the peak of US summer gasoline demand has now past and European gasoline demand is not likely to surge higher any time soon to plug the gap left by fewer imports by Nigeria. In short, competition among refiners in the Atlantic Basin is intensifying and the Dangote refinery is only adding to that.