Global crude/condensate flows are showing signs of slowing down in July

Global crude/condensate exports are showing signs of slowdown in July while China continues to build stocks keeping imports robust.

20 July, 2023

Recent developments in key global crude oil markets are starting to affect seaborne crude exports as well as arrivals for July, according to Vortexa data. Following up on our recently published crude insights focusing on crude quality and freight, we now focus on crude flows in key markets such as OPEC, US and China.

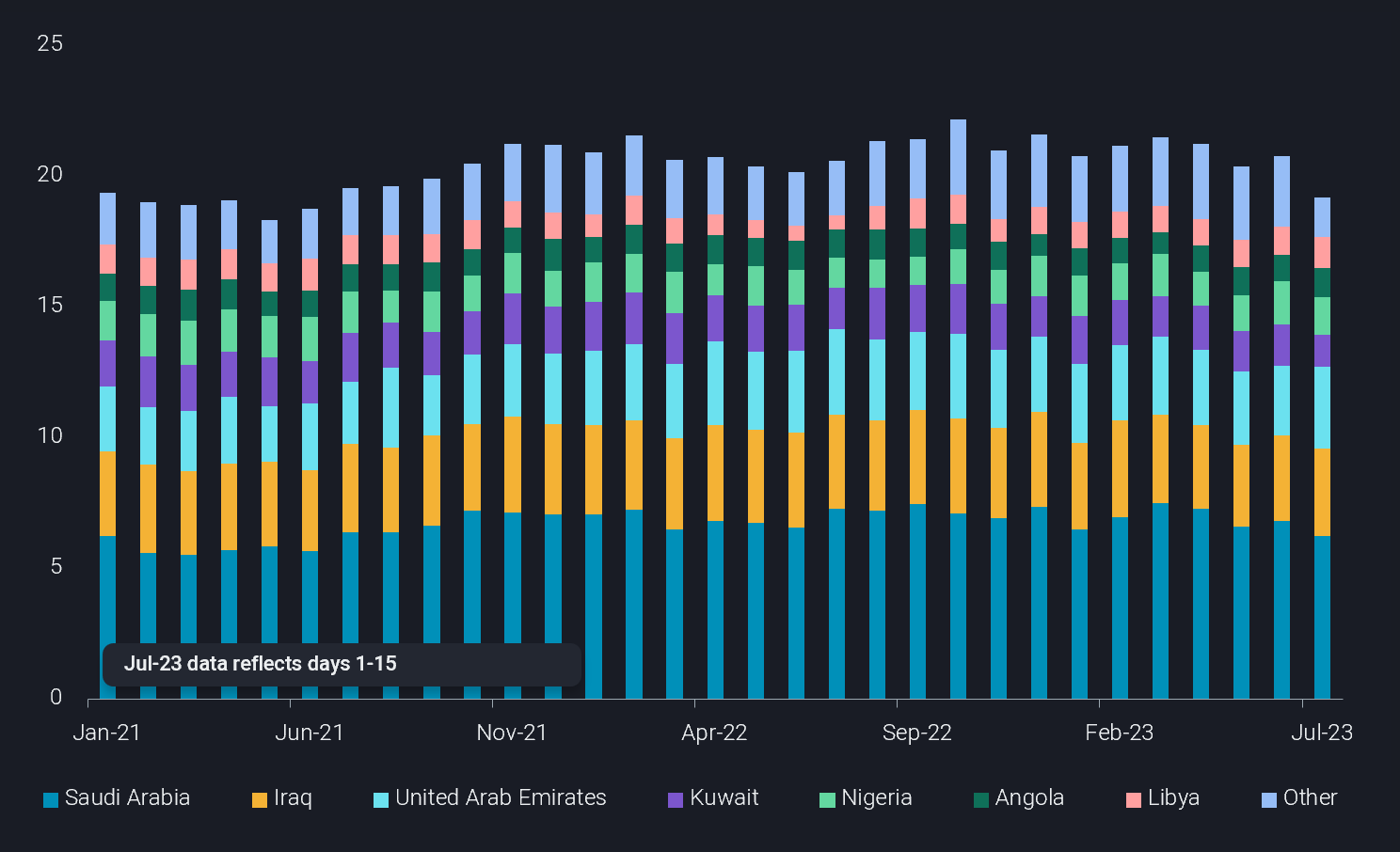

OPEC crude/condensate exports decrease

- Preliminary data for crude/condensate exports from Saudi Arabia for the month of July (days 1-15) show a decline of 0.6mbd vs June.

- Similarly, exports from other OPEC member countries like Kuwait, Nigeria and Algeria are also down by another 0.6mbd vs June.

- On the contrary, UAE’s and Iraq’s exports increased by 0.5mbd in July (days 1-15), somewhat offsetting the decline from Saudi Arabia.

- This decline in OPEC exports, especially from Saudi Arabia, could point to recently announced voluntary production cuts (group and unilateral) finally showing its effects and driving tightness in sour crude markets.

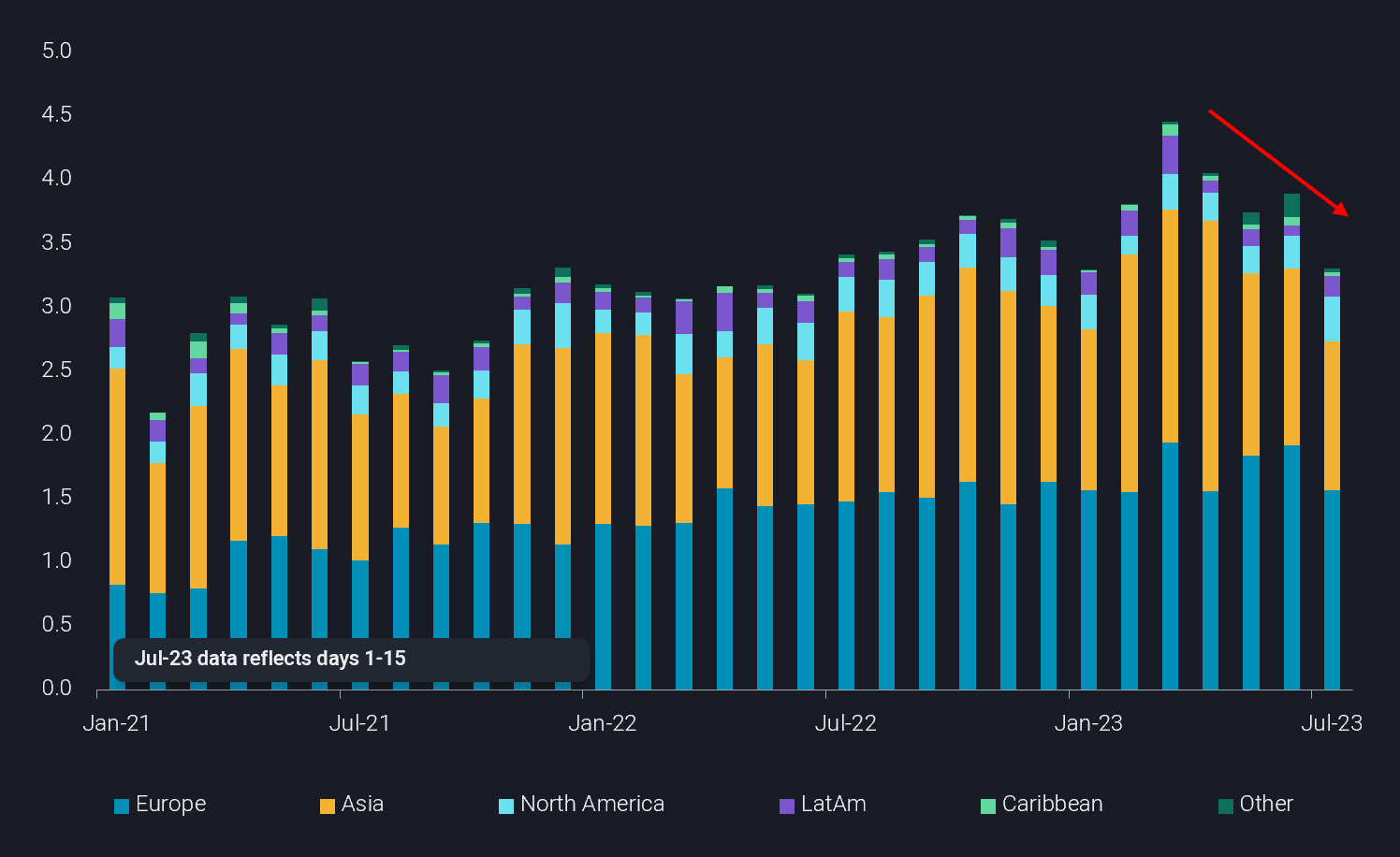

US domestic refining demand pulls barrels away from exports

- US seaborne crude/condensate exports are finally showing signs of slowdown, after robust exports in previous months, as preliminary data for July (days 1-15) puts exports 570kbd below June.

- Slowdown in demand for light sweet crudes in markets like Asia and an oversupply in Europe, along with summer US refinery demand, can be attributed as the key reasons for this decline.

- We should also take these preliminary indications with a caveat that US exports could rise as the September trading window starts given how light sweet crudes are being pressured by sour crudes selling at premiums.

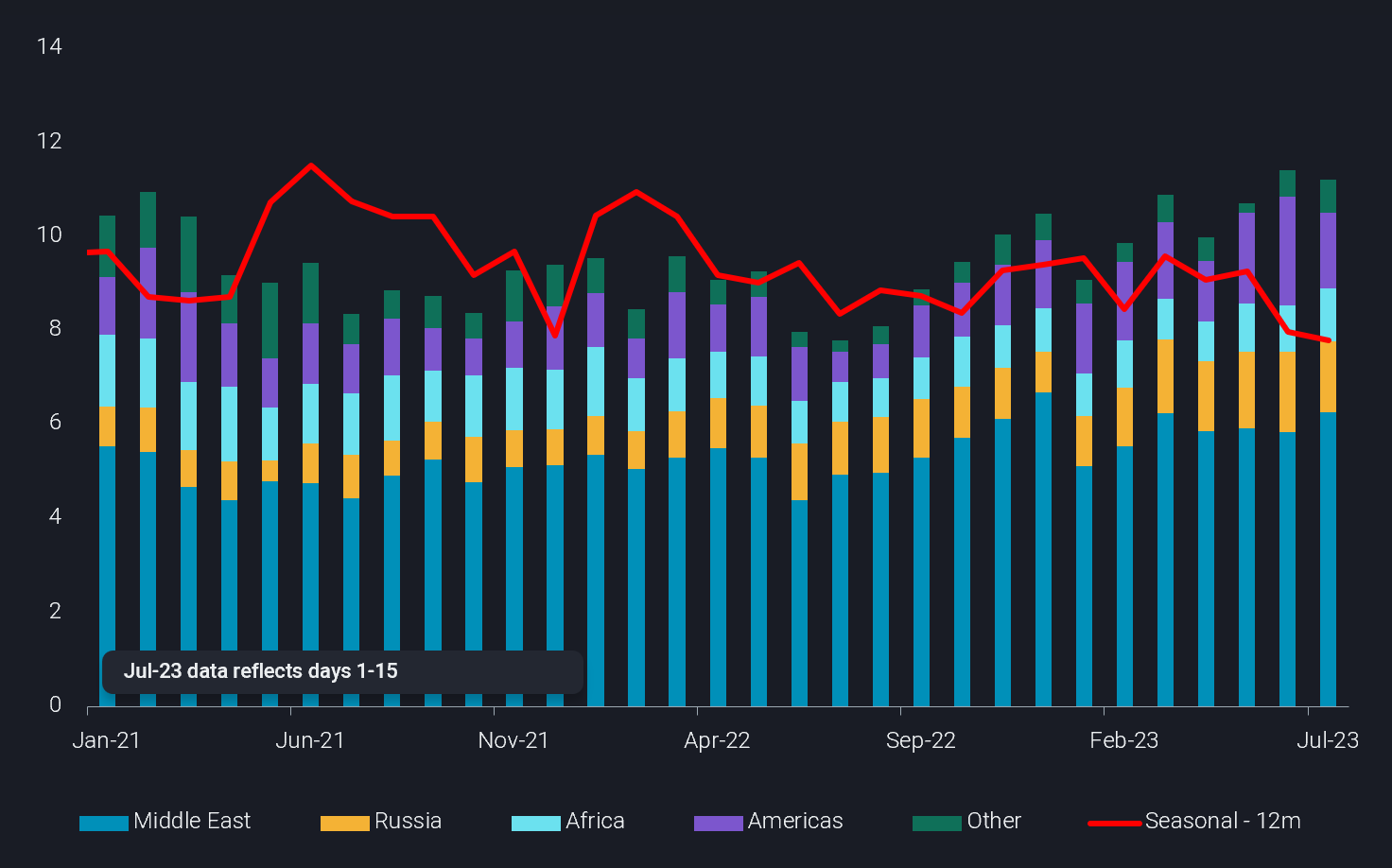

China’s crude imports remain strong

- China’s seaborne crude imports in July (days 1-15) came in at 11.2mbd, just shy of the multi-year high imports seen last month. While a lot of crude is in transit to China, we estimate that the final monthly figure will be markedly below 11mbd.

- These strong imports though, are not an indicator of Chinese demand returning to pre-pandemic levels as stock builds suggest relatively weak crude processing rates at Chinese refiners – Shandong teapot refiners are cutting runs amid restricted feedstock access and state-run refiners undergoing turnarounds.

- These high imports and subsequent stock builds seem to be an insurance for Chinese refiners expecting domestic demand to improve, while global crude supply starts getting tighter in the coming months.

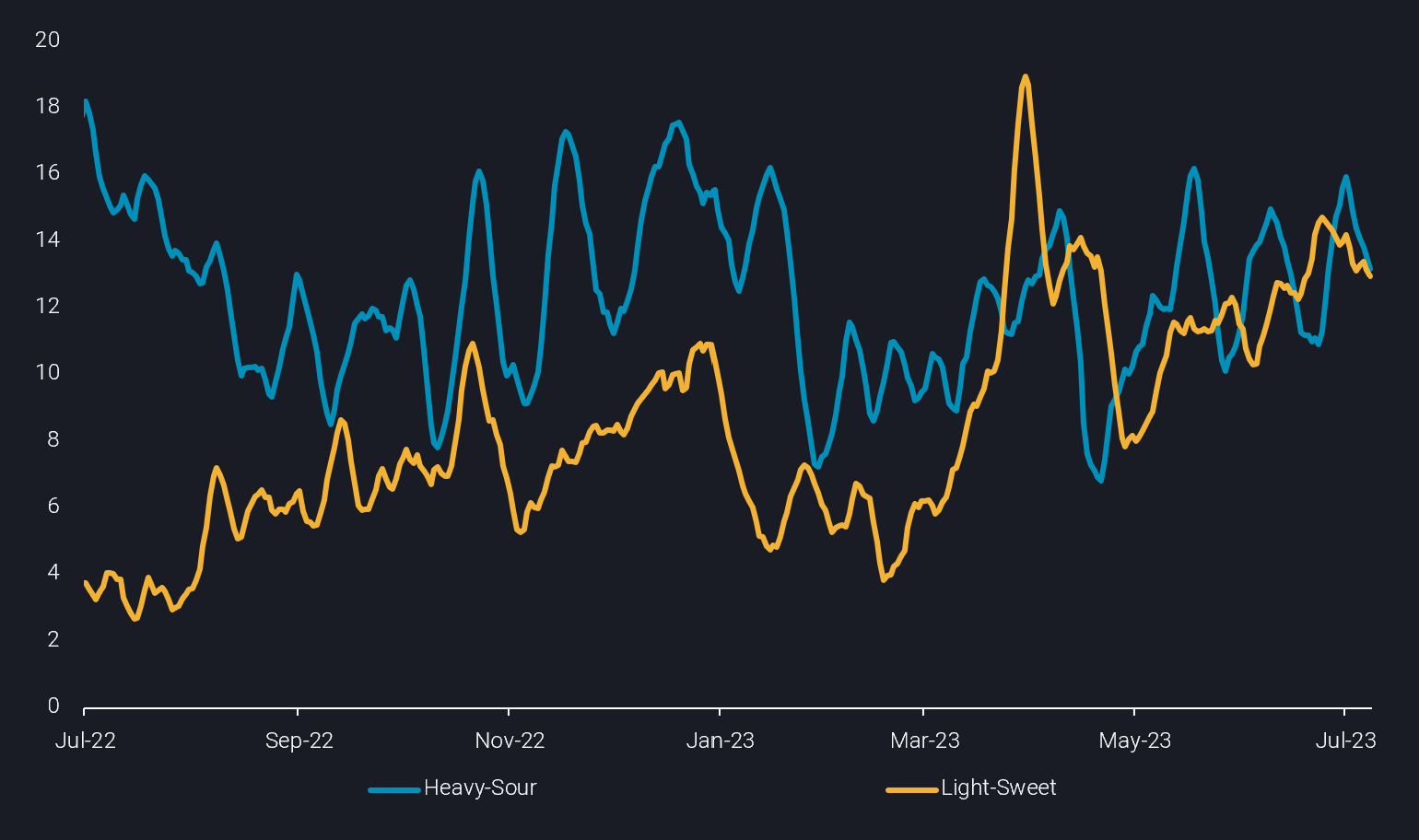

Global crude floating storage seen declining

- Floating storage for both light sweet and heavy sour crudes have remained around similar levels since April following record high levels of US light sweet crude making its way to export markets.

- However the path to current levels for both types of crude are very different with volumes for light sweet rising in a more sustained manner, especially in the past few weeks.

- US light sweet crude tankers continue to float offshore Rotterdam gradually discharging while Saudi crude previously floating off Ain Sukhna has been discharging.

- Going forwards, both types of crude in floating storage are likely to decline given the lack of economic incentive to remain afloat.