Global oil prices are stabilising following weeks of persistent gains. Market fundamentals are increasingly pointing towards a reversal of supply tightness that had gripped the market, with a rebuilding of onshore crude inventories and weakening middle distillate cracks casting growing uncertainties on demand. The cooling of market sentiments following a pause on escalations of geopolitical tensions have capped upsides on oil prices but the risks are far from removed.

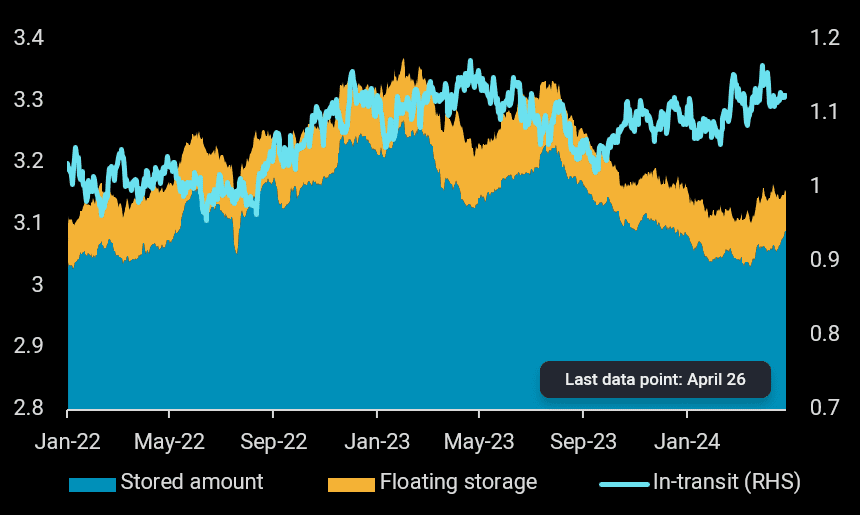

Global onshore crude inventories rebound, in-transit flows climb

After touching a multi-year low in March, global onshore crude inventories have started rebuilding. Prominent increases are seen in the Middle East and Northwest Europe, with levels reaching their highest since last June and September, respectively. Above-ground crude inventories in China, which started drawing since last August through to this February, have reversed to show a slight net build over the last two months. Besides the accumulation of stocks in storage terminals, seaborne in-transit volumes have also been on the rise in recent months, up nearly 4% in April versus January, adding to the length in the market.

Global onshore and floating storage crude inventory (bb, LHS) and in-transit volumes (bb, RHS)

Post-turnaround refinery ramp-ups capped by falling middle distillate cracks

Some may argue that the reprieve on the global crude market tightness could be temporary given peak refinery maintenance season in Asia and Europe this quarter. As with previous years, refiners are likely to ramp up crude runs after turnaround but falling middle distillate cracks could dampen sentiments. The weakness in middle distillate cracks despite ongoing refinery maintenance reflects ample global supplies against a backdrop of lacklustre demand. Elevated crude prices are further eroding refining margins, with several refiners considering refinery run cuts in the weeks ahead.

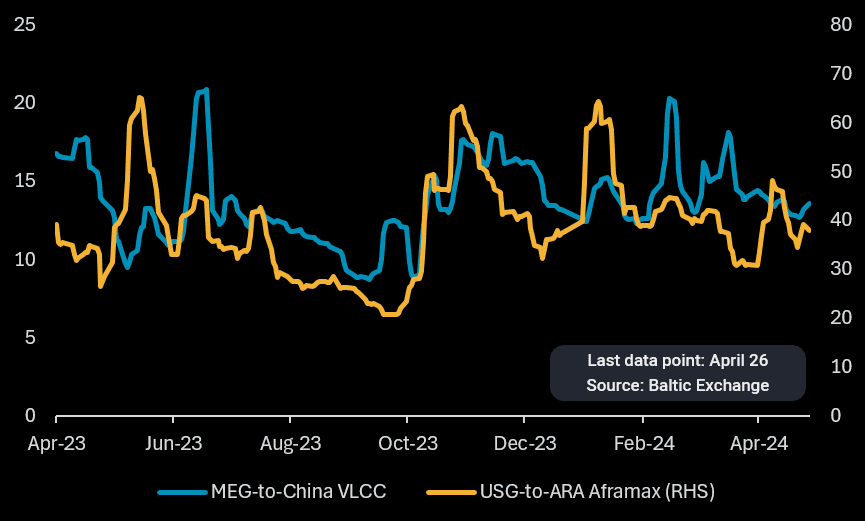

Lukewarm VLCC and Aframax freight rates further confirm the absence of a strong post-turnaround refinery ramp-up in Asia and Europe. A closed US-Asia WTI arbitrage despite tight Middle East crude supplies has led to fewer long-haul VLCC bookings, weighing on tanker freight rates.TD3C (Middle East-to-China VLCC) rates are averaging $13/t as of the last week of April, the second-lowest weekly average so far this year. Meanwhile, TD25 (US Gulf-to-ARA Aframax) rates have risen by 13% w-o-w last week, but remain well below levels seen at the start of the year, suggesting weakness in tanker bookings for US crude deliveries to Europe.

MEG-to-China VLCC and USG-to-ARA Aframax rates (RHS) ($/t)

US sanctions on Iran and Venezuela – political posturing with limited supply impact

Renewed and expanded US sanctions on Venezuela and Iran respectively are unlikely to have any material impact on crude exports from both countries. Major companies like Chevron, Repsol and ENI have received waivers from the US to continue their upstream operations in Venezuela, with the real impact limited to a loss of Venezuelan crude supplies to India, with future cargoes likely to be diverted to China. Meanwhile, expanded sanctions on Iran are unlikely to deter Chinese independent refiners from buying Iranian crude given that most of these buyers do not have any operations outside of China. The US sanctions are more likely a political move to drum up voter sentiments ahead of the US elections this year, with no real impact on crude supply.

Current demand fundamentals are signalling growing downside risks on oil prices but uncertainties remain. While major economies have been reporting improving economic activities, we are yet to see a clear and sustained recovery. Supply-side risks from geopolitical tensions and OPEC+ production targets in the second half of the year could swing oil prices in either direction. An upside for oil prices lies with the need for countries to rebuild their crude stocks, which are currently at multi-year lows, but stock building will only be done when the timing and pricing is right.