Highlights from geopolitical risk webinar

On the 16th October, Vortexa hosted a geopolitical risk webinar, posing the question of “Is sanctioning tankers a game-changer for Iran & Russia’s oil flows?”. This insight provides a summary of the webinar, focusing on sanctions impact, flows and freight analysis.

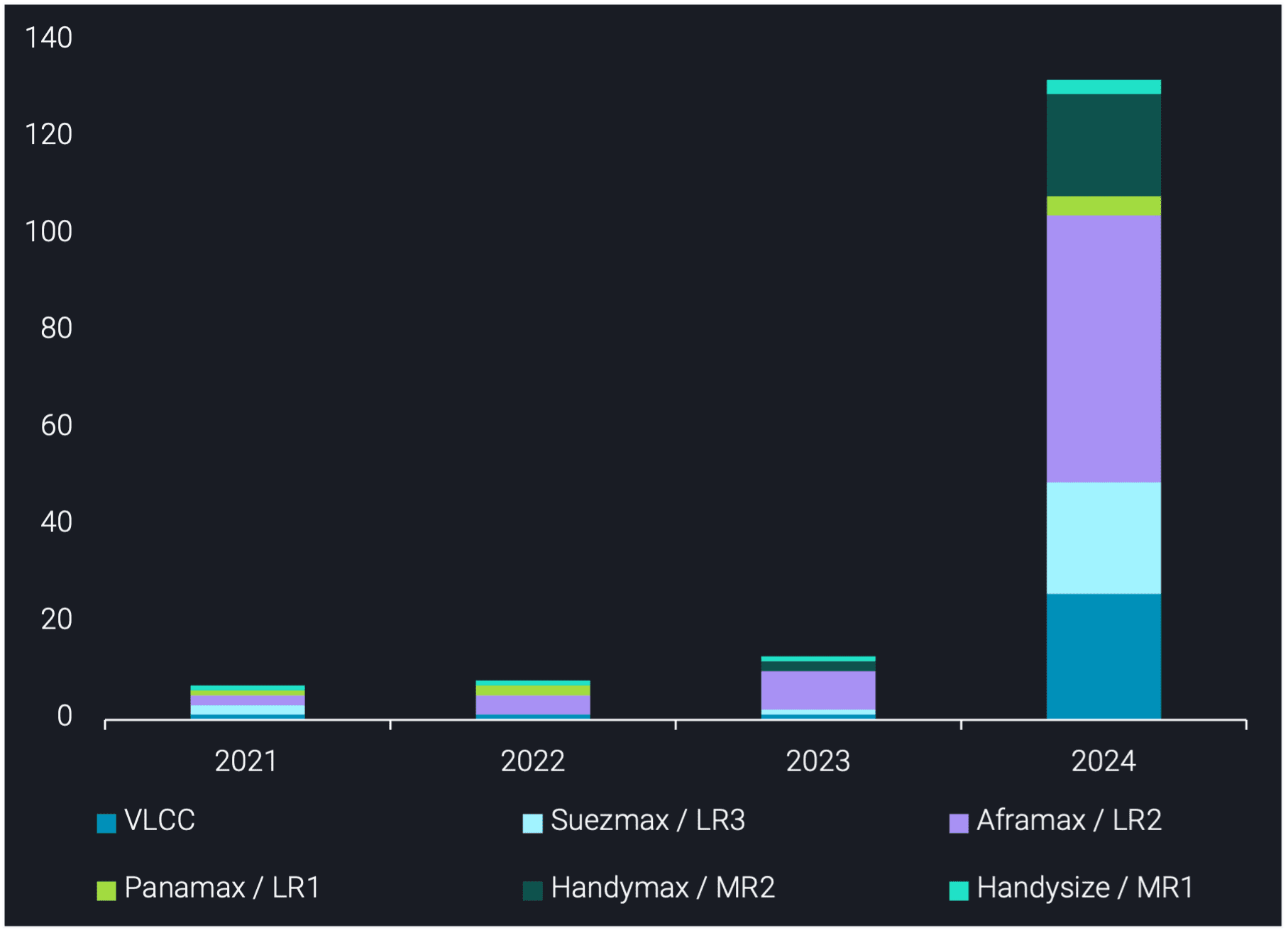

Record number of tankers sanctioned in 2024

At the time of the webinar, over 130 oil tankers had been sanctioned by the EU, UK and US in 2024, a record-high, with VLCCs and Aframaxes being the predominant target. These tankers were sanctioned for Russia and Iran designations, with the aim of reducing these tankers’ employment in these respective trades.

On the 17th October, an additional 25 oil tankers were sanctioned for Iran & Russia designations, by the US and the UK. This suggests that governments continue to apply pressure, focusing on slowing down fleet employment in these sanctioned trades.

Count of unique oil tankers sanctioned between 2021 and 2024, split by vessel class and year sanctioned

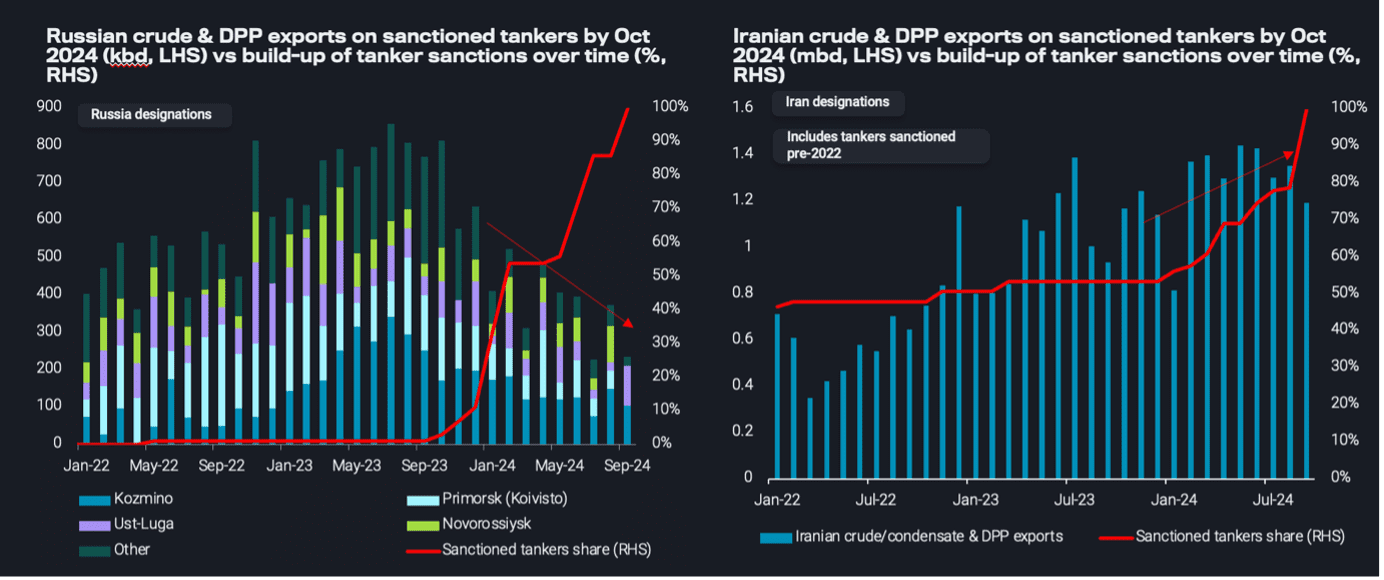

Russia and Iran respond differently to sanctions

Tankers sanctioned for Russia designations resulted in a 400kbd cut in crude and DPP exports y-o-y specifically on these tankers, because of difficulties finding employment. On the other hand, Iran has increased its crude exports over this period by 300kbd on sanctioned tankers, suggesting sanctions are having no impact on the Iranian market as exports have grown.

One reason for this difference in response is that whilst tanker-specific sanctions in the Russian market are new, the National Iranian Tanker Company (NITC) fleet have been sanctioned for years. Those tankers continue to trade, mainly conducting Iranian port calls, so the impact from sanctions now on the Iranian market is muted because they have created methods over a sustained period of time to circumvent sanctions.

There is also a difference within Russia’s response to sanctions, depending on which government is making the designations. OFAC (US) sanctioned tankers in the Russian market lost 300kbd crude exports y-o-y whilst EU & UK sanctioned tankers only lost 50kbd over the same period, proving US effectiveness over EU/UK sanctions. This suggests there is higher risk aversion to employing tankers sanctioned by the US as opposed to the EU & UK.

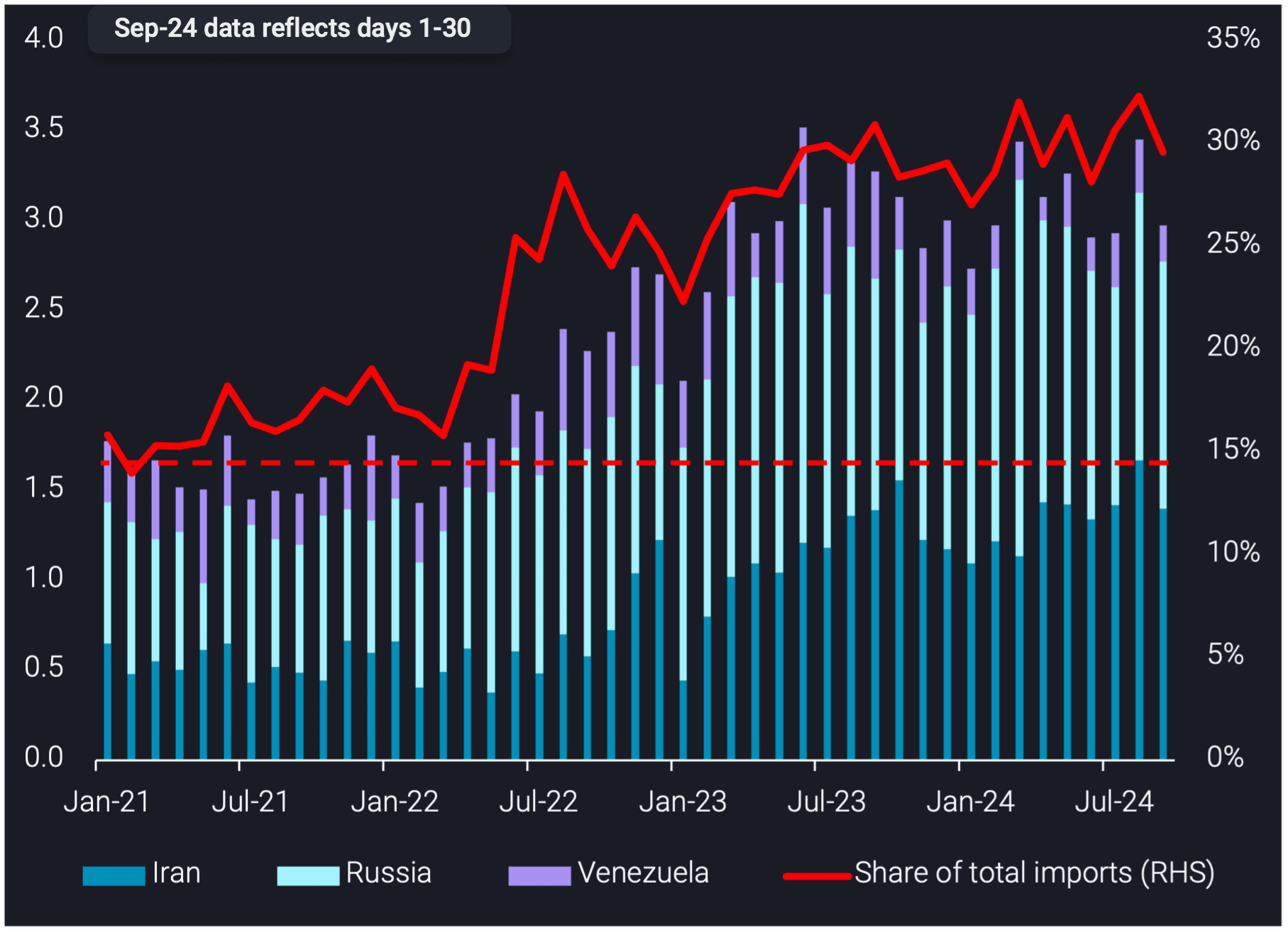

Discounted feedstock accounts for 30% of China’s imports

China’s imports of discounted feedstock (crude & DPP) accounts for 30% of its total imports. This was supported by China’s imports of Iranian crude surpassing 1.6mbd in August, a record-high. This further supports the argument that vessel-specific sanctions are having a muted impact on the Iranian market, as China continues to import these barrels.

Discounted crude imports to Shandong and Jiangsu, two key provinces in China which import these barrels, have displaced 500kbd of non-sanctioned crude supplies, namely from Brazil and Angola. The rise in share of discounted barrels relative to mainstream crude supplies suggest a growing importance of these markets to China and the declining impact of sanctions.

As long as China continues to buy Iranian crude, we could expect an increase in STS activity. Non-sanctioned tankers will load via STS from sanctioned tankers to then discharge in China, something we have already observed, but as sanctions increase, we could see longer STS chains to ensure non-sanctioned tankers are the last leg in the STS.

Tankers in Iranian trade near record-high in 2024

Nearly 250 tankers handled Iranian crude & DPP in 2024 so far, with VLCCs accounting for over 50% of the fleet. VLCCs in this trade have hit a record-high in 2024, supporting the growth in Iran’s crude/condensate exports to the multi-year high of over 1.8mbd in 2024.

The overall fleet has grown y-o-y, and the data suggests that 2024 full year will show a larger fleet than 2023 given 2024 so far (Jan-Sep) is very near the full-year 2023 fleet size.

Count of unique tankers operating in Iranian crude & DPP trade per year split by vessel class

Outlook

At this point, there are no strong indications that steadily adjusted sanctions are keeping oil from flowing, which for the case of Russia is generally not really the intention. Of course, governments could target to crack down even further on involved parties and logistics, but ultimately the question will be whether China is willing to take the delivery of the oil, something that so far is clearly the case. We could observe STS activity rise as vessel-specific sanctions increase and see an increase in the number of tankers trading in these markets, to further facilitate the trade.