Mediterranean light crude: volumes limited and sold locally, weighing on freight demand

Vortexa analyses flow developments in the Mediterranean, assessing the impact on freight rates and inferring on what lies ahead.

Supply issues in Libya and Kazakhstan are illustrating the relevance of Mediterranean light crude supplies, including those flowing from the Caspian and Black Sea regions. We will review flows out of the region, the interaction with freight rates and provide a view on what lies ahead.

Flows behaviour: similar but not the same

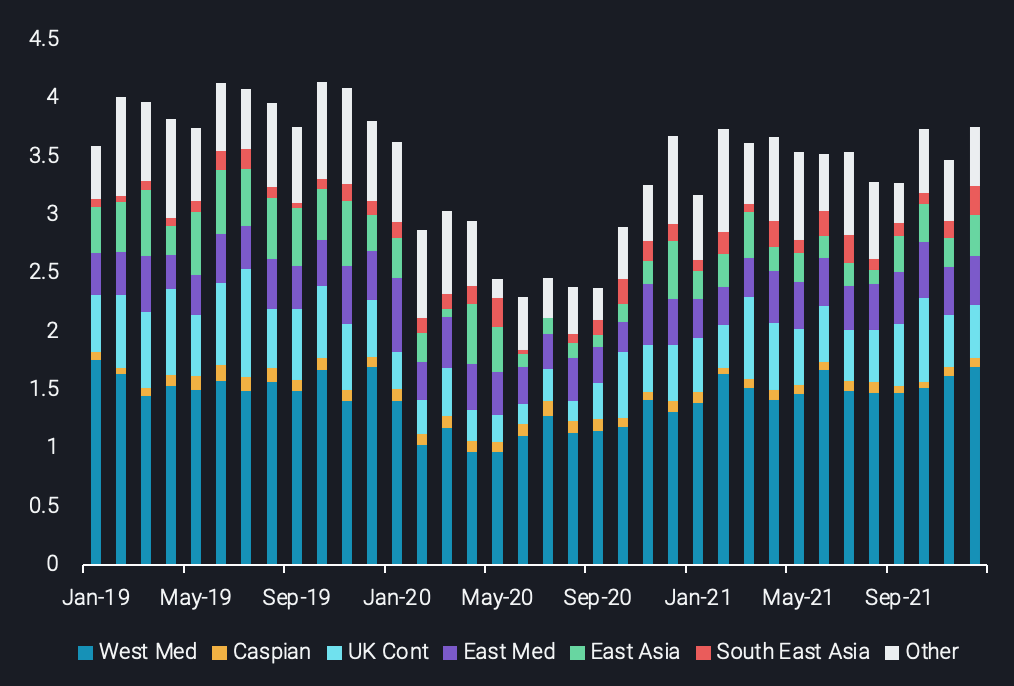

Exports from Black Sea & Mediterranean by destination region (mbd)

Light crude supply from the wider Mediterranean experienced a 700kbd y-o-y increase in 2021 to close to 3.5mbd, but still experienced a shortfall of more than 400kbd versus 2019 levels. Lower levels in 2020 were largely a function of oil terminal blockades in Libya which evaporated exports out of the country, added to by the OPEC+ supply constraints affecting Azeri and Kazakh barrels. The latter had still an impact on 2021 volumes, but it is questionable how much additional supplies will come out of Azerbaijan and Kazakhstan going forward, giving natural decline affecting production, and some barrels being rerouted via the Russian pipeline system to Northwest Europe.

In terms of destination markets, local supplies to the Mediterranean have been stable over time, with the temporary 2020 losses as well as the structural declines affecting predominantly longer-haul markets. In 2020, only 260kbd were directed towards East Asia, down by a massive 200kbd when compared with 2019. This is only partially offset by an extra 50kbd headed to Southeast Asia over the same timeframe, which has a negative overall effect on tonne-miles as displayed on the graph below.

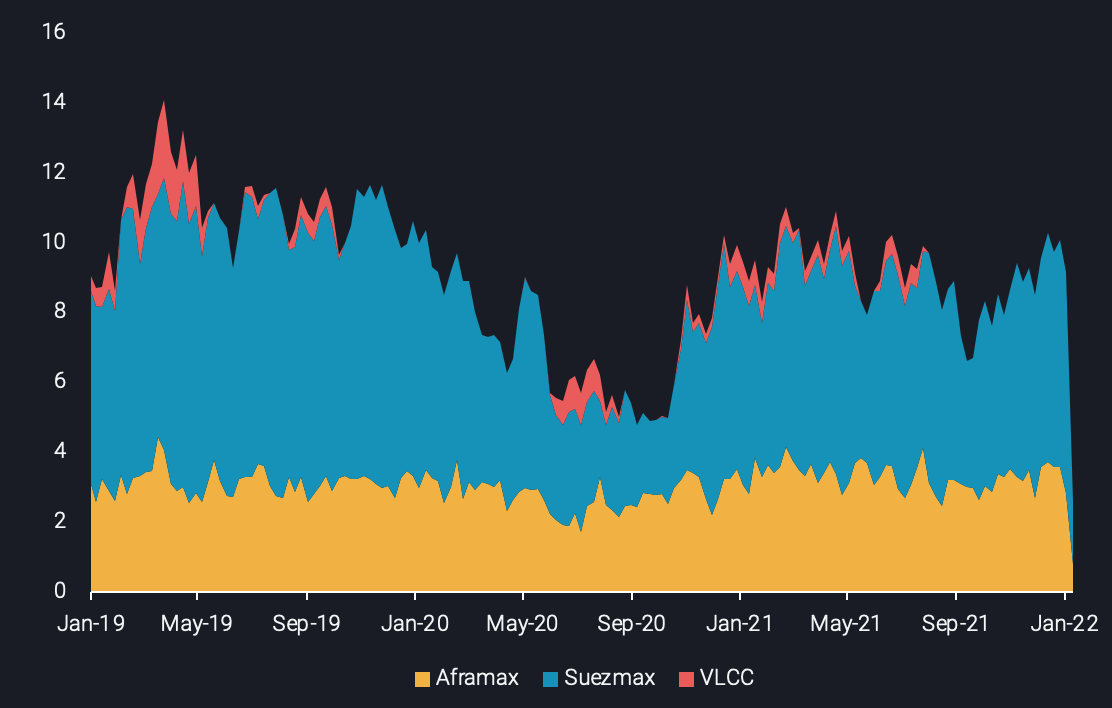

Tonne-miles out of Black Sea and Mediterranean by vessel class (bn tonne-miles)

Suezmaxes bear the brunt of falling tonne-miles

When splitting the overall tonne-mile demand by vessel class, it is obvious that Suezmaxes took the heaviest hit. Despite carrying more cargoes towards the West Med and Southeast Asia, the smaller exposure of the segment on East Asia and West Coast India destinations decreased the overall distance travelled.

On the other hand, Aframax tonne-miles have remained relatively stable since 2019. Though less volumes headed to the West Mediterranean at the expense of the eastern part of the region, a small but increasing number of cargoes carried on Aframax tankers found home in long-haul destinations such as Southeast Asia and the US Atlantic Coast.

Freight rates: A vessel supply story

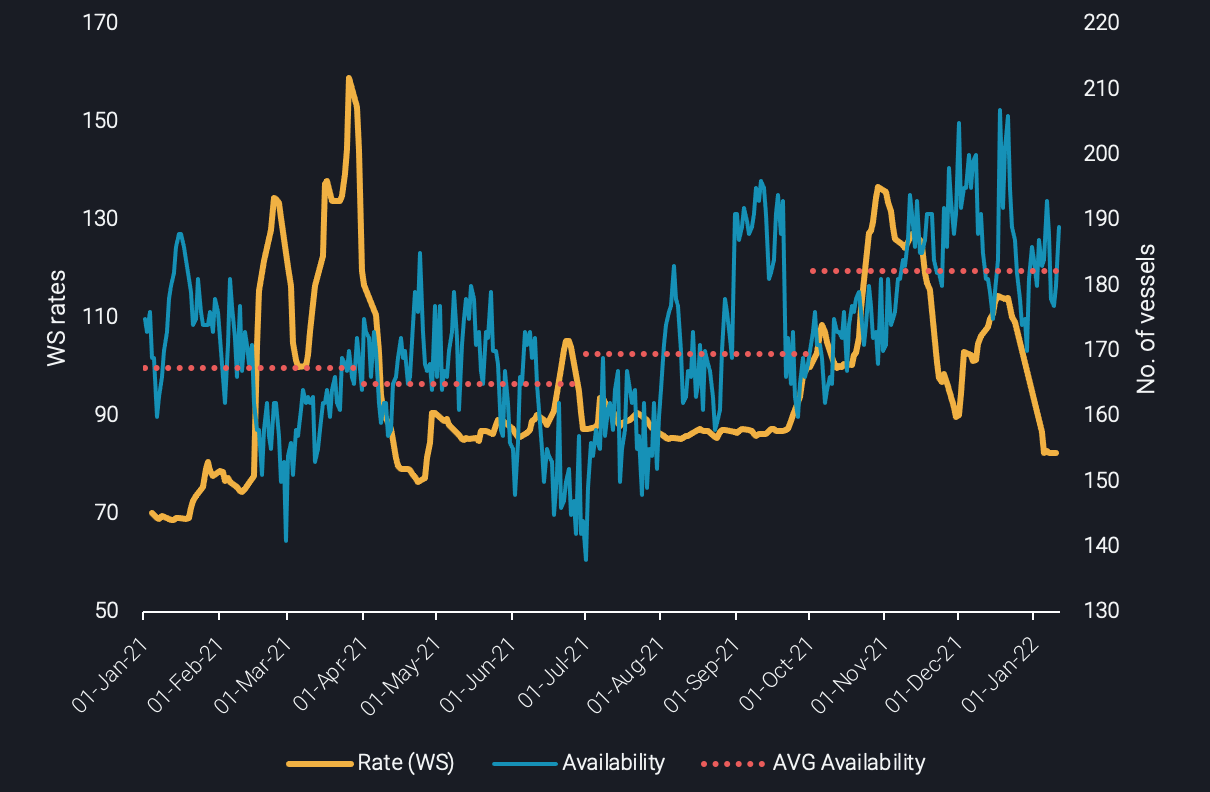

The next question to pose is whether this tonne-mile fluctuation impacted freight rates for Aframax and Suezmax tankers. The short answer is no. Looking at Vortexa’s freight pricing data in 2021, for the benchmark Aframax route TD19 (Cross – Mediterranean) it is clear that the rate for this route is correlated with vessel supply. The chart below shows that the majority of times where vessel availability was found below the average levels for each quarter, rates spiked.

TD19 (Cross-MED) rates (WS) vs Vessel Availability (no. of vessels – RHS)

The following specific examples underpin this picture:

- March 2021: The Suez Canal Blockage, limited availability of Aframaxes stemming from the East of Suez.

- November & December 2021: Higher Aframax demand was seen in the Baltic Sea as well as PADD 3 as Russia and US respectively boosted their production and in turn exports. This left a lower number of available vessels in the Mediterranean and the Black Sea, at a time when vessel congestion was also observed in Turkish straits, limiting supply further.

A similar sensitivity between vessel supply and rates is observed for the Suezmax trademark route in the region under investigation: TD6 (Black Sea – Mediterranean)

Outlook

Looking ahead, not much supports a sustainable freight recovery in the Mediterranean and Black Sea region this year. Oversupply is plaguing the sector and higher y-o-y Suezmax deliveries will only increase the pressure. On the Aframax front, scheduled deliveries are expected to remain stable. However, the sector is in dire need of higher scrapping activity, but strong activity in illicit trades and related high second-hand prices seem to prohibit this for the time being.

The tanker demand side does not look encouraging either. Tonne-miles will unlikely find any support from long-haul destinations such as East Asia and more specifically China. The country’s clampdown on its refining sector, administered via crude import and product export quotas and the recent resurfacing of Omicron cases at key ports, all point towards lower crude purchasing activity. Furthermore, competitive exporters such as the Middle East and the US are ramping up exports, raising competition in long-haul markets for Mediterranean light crude barrels, the availability of which is at best to move sidewards. Having said that, there is the potential of seasonal rate spikes, likely to be related to Turkish Straits congestion due to adverse weather conditions. This as said before will limit regional supply, thus letting Mediterranean-operating vessels take a breather.

More from Vortexa Analysis

- Jan 11, 2022: China sets tone for refiners with tight oil quotas in the new year

- Jan 6, 2022: Global crude exports end 2021 on a high

- Dec 31, 2021: Making Waves: Looking back at a year of Freight

- Dec 22, 2021: Omicron infiltrates tankers in the Atlantic basin

- Dec 21, 2021: Asian refiners find silver linings amidst an ominous Omicron outlook

- Dec 16, 2021: Volatile global flows and hydrogen economics leave Europe short in naphtha

- Dec 14, 2021: 2022: The Freight Forecast

- Dec 9, 2021: Big oil producers shine as refiners

- Dec 8, 2021: Russia and Ukraine: What’s at Stake for Oil?

- Dec 7, 2021: LPG flood reaches Asia and Europe in December

- Dec 2, 2021: Omicron obscures outlook for tanker markets

- Dec 1, 2021: Rising flows, wrong time?

- Dec 1, 2021: What a time(ing)!?