Opaque market players’ crude exports reach 4-year high

This insight explores how Iran, Russia & Venezuela, comprising the opaque market, have seen their combined crude exports reach a 4-year high in 2023.

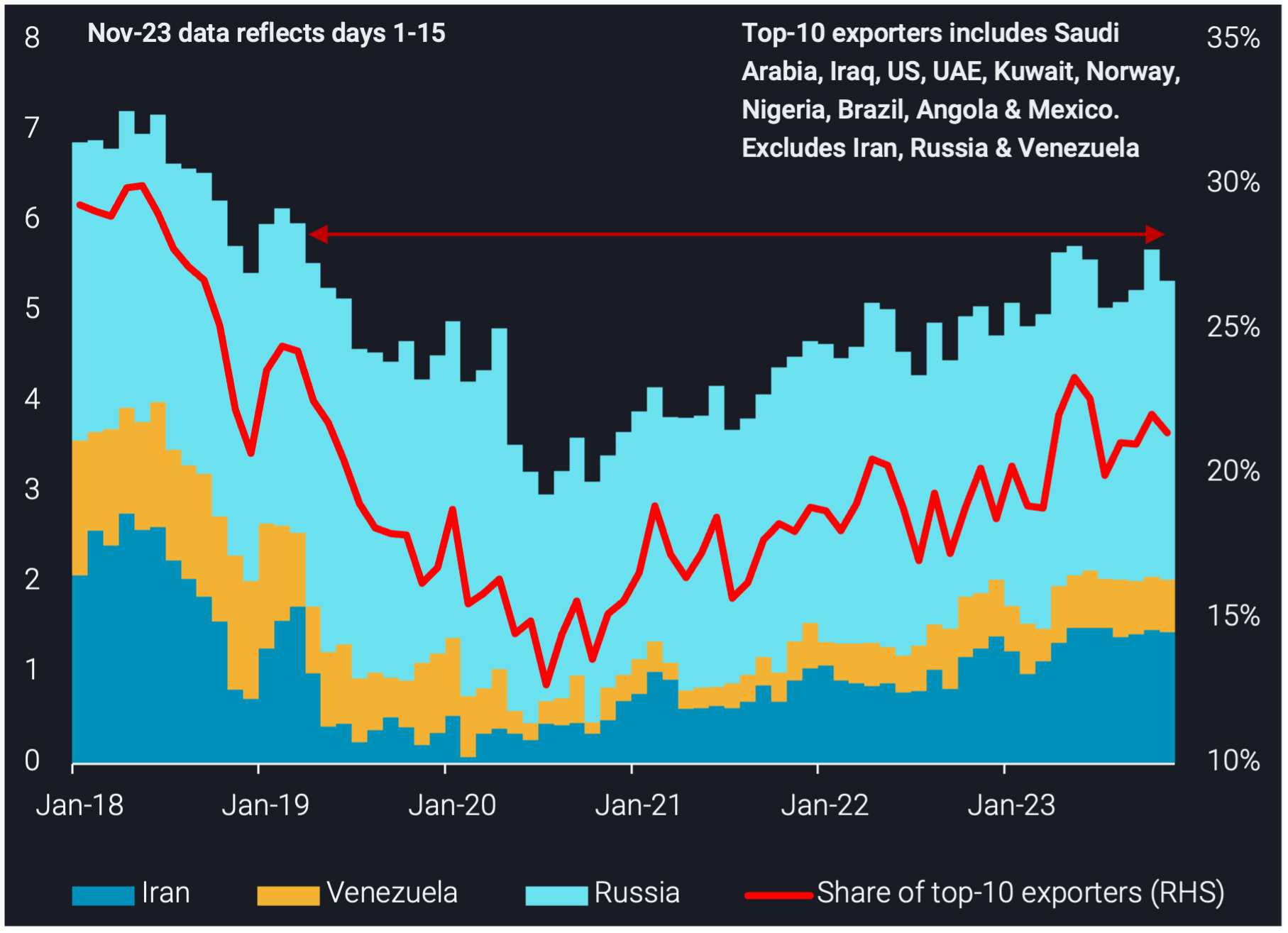

Iran, Russia and Venezuela’s (opaque market) combined crude exports reached 5.7mbd in May, a 4-year high and a 15% increase y-o-y. The opaque markets’ crude exports averaged 5.2mbd in 2023, a 500kbd increase y-o-y, contributing an increasingly important share to global crude supply.

This 4-year high was driven by record-high Iranian crude/condensate exports and Russia increasing its crude exports despite sanctions. Iran’s crude/condensate exports surpassed 1.5mbd in May, driven by strong demand from China and increased production. Russia also increased its crude exports (excl. CPC Blend & KEBCO) to 3.6mbd in May, despite the EU import ban and OPEC+ cuts.

Russia has been successful in finding alternative buyers for its crude – India accounts for 50% of Russian crude imports in 2023, compared to 20% in 2022. China accounts for 40% in 2023, a 10pp increase y-o-y.

Venezuela’s exports have increased due to higher production and US increased purchases of Venezuelan crude via Chevron. The recent easing of US sanctions may see exports lifted further, though this could be limited if production doesn’t increase from current levels, while the persistence of the waiver is everything else than certain.

The opaque market exports in 2023 stand at 20% compared to the 10 largest crude/condensate exporters globally, the highest level since 2019.

Opaque market tanker activity peaked in Q2, supporting 4-year high exports

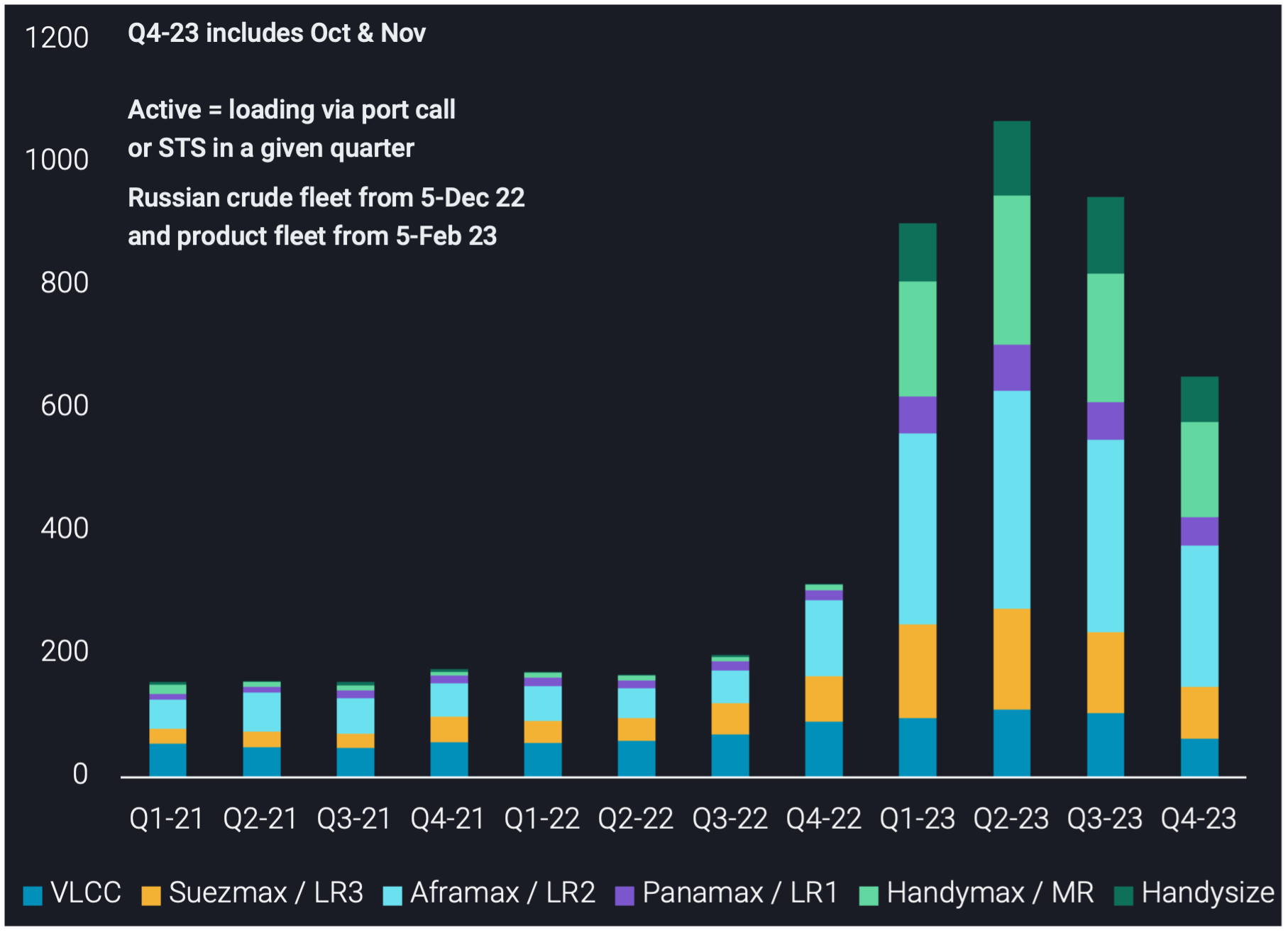

The number of tankers operating in opaque markets reached a record high in Q2, supporting the opaque markets’ 4-year high crude exports. We track 1070 tankers which carried Iranian, Russian and Venezuelan crude/condensate, DPP & CPP in Q2.

Russian crude & product carriers accounted for 80% of all opaque market tanker activity in Q2. The inclusion of Russian crude and product carriers in the opaque fleet since 5-Dec & 5-Feb has resulted in a surge in smaller tankers in this fleet. Aframaxes and smaller classes accounted for 75% of the fleet in 2023, a 30pp increase y-o-y.

Opaque market tanker activity declined 10% in Q3 (q-o-q) reflecting the decline in Iran’s crude/condensate exports and Russia’s crude and CPP exports over this period.

Opaque market tanker activity in Q4 suggests a possible further slowdown, possibly as US efforts to crack down on the implementation of the price cap mechanism in Russian sanctions may limit the amount of players willing to participate in this trade.

Count of unique tankers active in opaque markets per quarter split by vessel class

To find out more about the opaque market fleet, check out our newly published exclusive report here