Saudi Leads “Big Three” Cutting Crude Exports in May

In this insight we explore how the top three global crude suppliers are lowering exports in May and what that means for global oil markets.

Global waterborne crude supplies are being constrained in May as the three top suppliers reduce exports strongly from April levels.

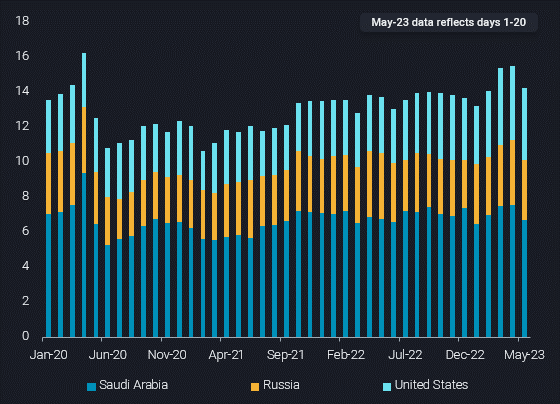

In the first month of its additional voluntary production cut, Saudi crude exports have fallen sharply from April levels. Meanwhile US exports have fallen for the second consecutive month while Russia’s exports are at the lowest level since February.

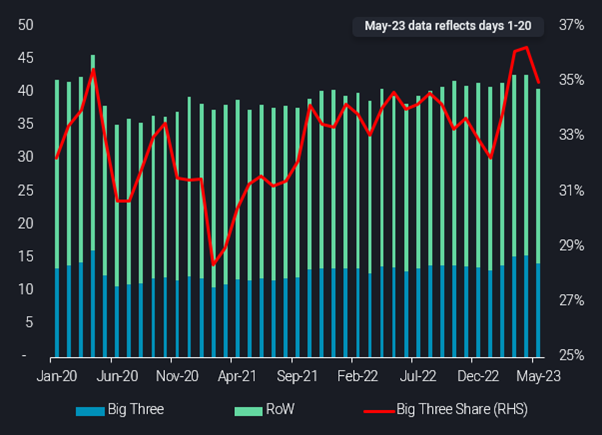

On a combined basis, total exports from the big three exporters (Saudi Arabia, Russia and US) are around 1.3mbd lower so far in May (days 1-20) from April full-month levels. However, while this 1.3mbd might initially seem high, when viewed with historical context, the total export volume of 14.2mbd is still at the upper end of ranges (see chart).

Focus on Saudi Arabia

As May comes to a close, market participants are keenly looking for evidence of Saudi Arabia’s 500kbd voluntary production cut. Export volumes provide an imperfect proxy in understanding to what extent production cuts are tightening supply.

Preliminary data for May (days 1-20) shows Saudi Arabia’s crude/condensate exports have fallen in the order of 800kbd from April full-month levels. This initially suggests a very strong response to the May voluntary supply cut. However, a more nuanced look shows the recent sharp drop in exports comes after significantly higher exports in prior weeks.

Saudi weekly exports had peaked at almost 8mbd in the first weeks of April before falling to a still high 7.5mbd in the middle of April. Exports have fallen sharply in the past couple of weeks but even at 6.4-6.5mbd, loading activity is actually similar to export volumes seen at the start of the year.

Put simply, it will still take some time to say with confidence production cuts are translating into lower exports. The current low level of exports needs to be sustained through June to show they are really a function of production cuts rather than a tilted loading/export schedule.

Russian exports

Russian exports are down almost 300kbd so far in May, versus full month April levels. The drop is important because it marks the first time volumes have fallen since Russia’s 500kbd cut was announced. May’s decline comes largely from Baltic loadings suggesting that it will impact India’s imports the most – typically the largest post-war importer.

Nevertheless, at 3.5mbd, Russia’s total exports for May are still at the upper end of historical ranges. Despite the drop from April to May, the current level of exports has been surpassed in only three other months (including last month) since April 2020.

US resilience?

Out of the “Big Three” suppliers, the US seems more resilient in dropping exports, at least for now. Total loadings from the US, which include Canadian crude loaded from PADD 3 in May, have only fallen by around 100kbd from April – however full month volumes for May could end up slightly lower.

This relative strength of US exports is supported by the strong structural pull for US cargoes from Europe, as the latter has weaned itself off Russian crude. But a more recent phenomenon is the inclusion of WTI crude in European North Sea crude market assessments.

Given that WTI delivered to Europe will have a stronger influence on North Sea pricing, it makes sense to see flows at least remain high, if not climb higher. We see this especially in the case of Aframax loadings to Europe (matching the 600-700kb assessment sizes) rising in May by 300kbd m-o-m, to levels last seen in October. Meanwhile flows from the US to Asia look to be weakening and could crimp total US exports, but still creating the potential for even more flow to head to Europe in the coming weeks.

Impact on global oil supplies

Zooming out to a global level, our May data shows that lower exports from the “Big Three” are having an outsized impact on reducing global supplies. These three key countries have become increasingly important over the past couple of years in raising crude exports faster than the rest of the world. The Big Three’s share of total global crude oil exports hit a peak of 36% last month, up from 28% in February 2021, but has dropped sharply so far in May. The key question going forward is whether this decline is a short-lived tightening in supplies, or a change in direction for the coming months.