The EU import ban on Russian refined petroleum products has triggered a new reality on clean petroleum product (CPP) trading patterns. By utilising our flow and freight datasets, we attempt to answer the most relevant questions surrounding Russia CPP exports.

Record CPP on water signals mixed as alternative buyers emerge

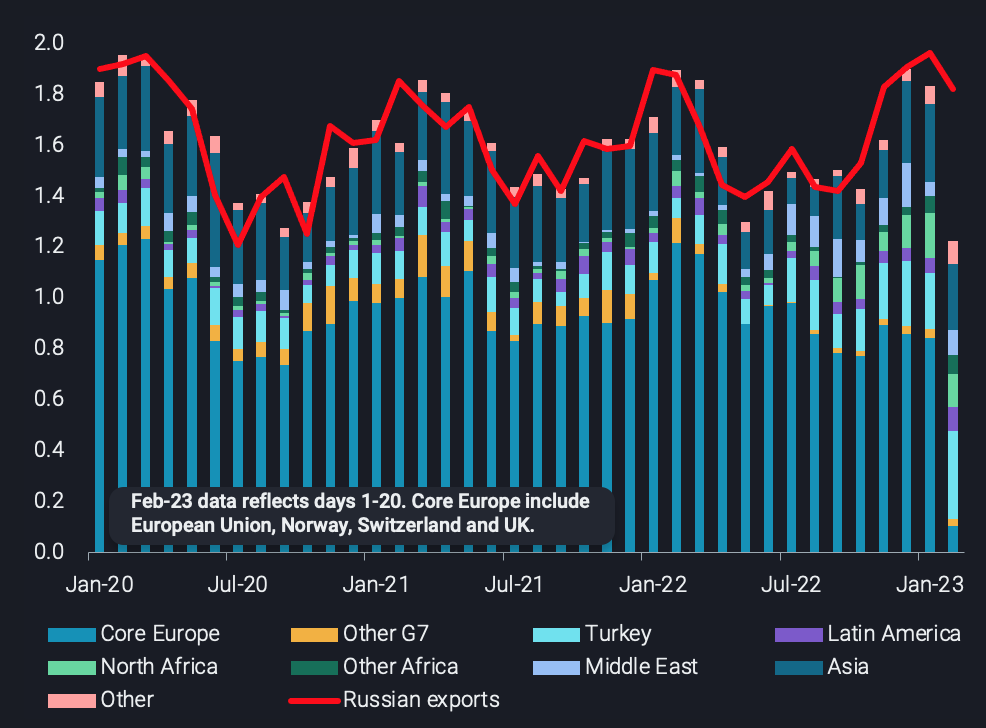

Russian CPP exports have moved slightly lower on a m-o-m basis in the first 15 days of February (red line), however the decline is less than 200kbd from a near three-year high of 1.9mbd in January. Despite the monthly decline, February’s diesel exports still remain 10% above pre-invasion average (Jan 2020 – Feb 2022).

As for imports of Russian CPP, average arrivals in the first 15 days of February into core European markets have tumbled by 700kbd to just 130kbd.

Interestingly, this has not been matched by imports into alternative markets which so far remain largely unchanged from last month. This disconnect between imports and exports is driven by a surge in Russian CPP on the water and begs the question whether Russia had lined up enough new buyers ahead of the EU import ban. In other words, is this surge caused by vessels travelling longer distances or are these exports sitting idle due to a lack of buyers?

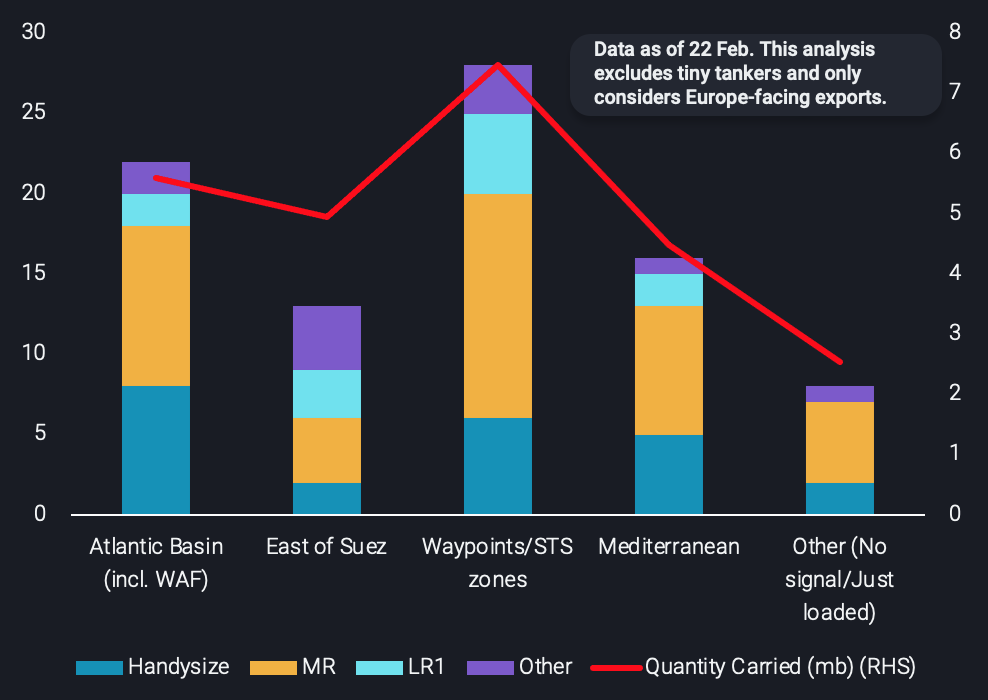

Taking a closer look at Russian diesel in-transit volumes, its prized export product, there are currently 87 vessels laden with Russian-origin diesel, including 63 vessels carrying 18mb that are currently signalling non-European/non-Med destinations, or Med waypoints/STS-zones.

The remainder are mainly signalling the Mediterranean, a trend that was starting to appear prior to the ban, with the ultimate destinations being North Africa and to a greater extent Turkey – an opportunistic post-war buyer of Russian oil and gas.

Destination signalled by vessels carrying Russian diesel (no. of vessels, LHS) vs. quantity carried (mb, RHS)

These alternative destination signals however, to regions such as the Middle East, West Africa and especially more recently to Brazil are a clear indication of a strong appetite for Russian diesel emerging outside the Mediterranean. The location of these buyerslocated farther away from traditional (pre-sanction) Russian outlets has so far boosted demand for clean tankers.

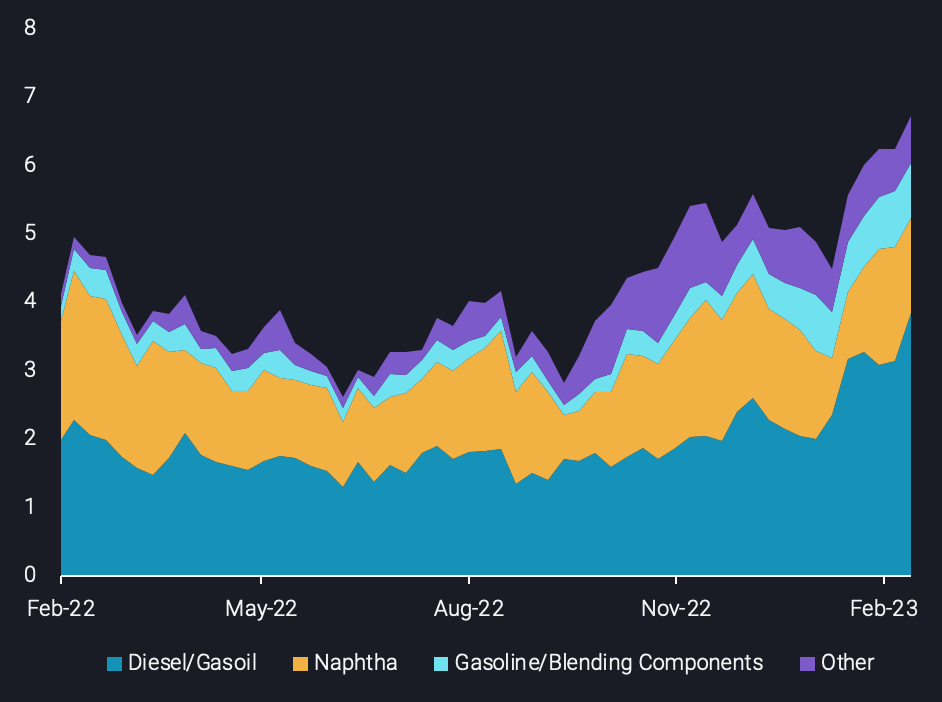

CPP tanker tonne-miles out of Russia are at record highs for the week ending 19 Feb and this incremental rise in tonne-mile demand is predominantly driven by the reshuffling of diesel trade flows.

CPP tonne-miles out of Russia by product carried (bn tonne-miles)

The increased tonne-miles, voyage length and pivot towards more STS locations is a common theme for both Russian CPP and crude exports. However, for those tankers heading to STS locations, a marked difference between CPP and crude is the STS zone of preference.

Unlike crude oil, more CPP STS activities are taking place in the Greek peninsula rather than Ceuta. If this phenomenon is a result of Spanish authorities attempting to crack down on STS activities off Ceuta, it will be interesting to see if having only one STS hotspot in Greece’s Kalamata creates logistical bottlenecks for Russian exports in the future.

Fleet profile mimics crude whilst vessel requirements look sufficient

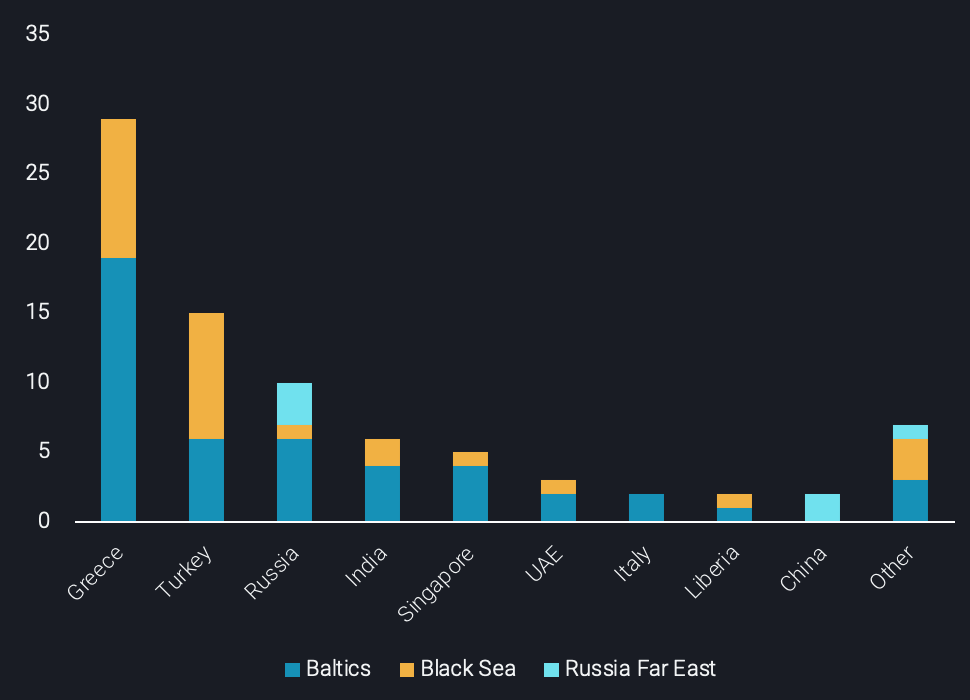

On the subject of Russian CPP tanker operators, we observe more similarities with crude than differences. The graph below illustrates that Greek effective controllers have taken the spotlight as is the case in the dirty trade. In the absence of Russian-operated clean tankers, Turkish operators have picked up the slack for cargoes heading to Turkey and other “Russian-friendly” states.

On the East Asia regional trade, Russian-owned and Chinese-operated vessels are more frequently employed than they are in the West of Suez, similar to the crude trade. It is a recipe which seems to have worked in maintaining Russian crude exports and appears to be re-applied on the CPP side.

The S&P market for older CPP vessels remains quite active (15+ years old the average age of the tankers operating in the Russian CPP trade post-ban) and the willingness of foreign operators to fill the gap of an evident lack of Russian clean tankers is evident..

Number of operator nationality carrying Russian CPP exports post 5-Feb, by loading shipping region

A count of ballasting vessels can also help reveal non-Russian operators’ activity in the Russian CPP trade. As the chart below shows, the number of ballasting clean tankers currently located in Northwest Europe and the Baltic is at historical highs. This is reflected when looking even slightly further ahead, as the number of ballast tankers signalling the Baltic to load in the next 9 days has been ramping up since the start of the February ban.

Number of ballasting CPP tankers located in Northwest Europe and the Baltic (no. of vessels)

In summary, the above data reveals that:

- Vessels do not reflect idle or a ‘wait-and-see’ behaviour at great scale, and hence do not display an enormous challenge in finding a buyer in non-traditional markets. Yet, a closer look should be given on the time it takes for these STS cargoes to find final destinations and whether this could logistically pose a serious threat to Russia’s exports.

- The supply of candidate tankers that can carry Russian products is building and appears well positioned to carry the next round of Russian CPP exports

Hence, in answering the question whether Russia is finding a way to maintain CPP exports in this new reality, the answer lies closer to a yes than a no.