US Gulf Coast sour crude markets tighten

US Gulf Coast sour crude crude markets have recently experienced tightness amid new developments in the region, chief amongst them being TMX start up

Recent developments in North America have led to a certain tightening of the sour crude market on the US Gulf coast. Chief amongst these is the Trans Mountain Expansion (TMX) pipeline start-up on May 1st which provides an alternative and direct seaborne outlet for exports of Western Canadian heavy sour crude from Vancouver. Other developments include an end to the refinery maintenance season for Gulf Coast refiners matching with the upcoming summer gasoline demand season, as well as the slowdown in Mexican crude exports due increased domestic processing and an upcoming refinery start-up at Dos Bocas. All these developments seem to have driven Gulf Coast medium sour crude differentials to a premium to Nymex WTI and we shall delve further into these developments in this insight.

TMX starts up

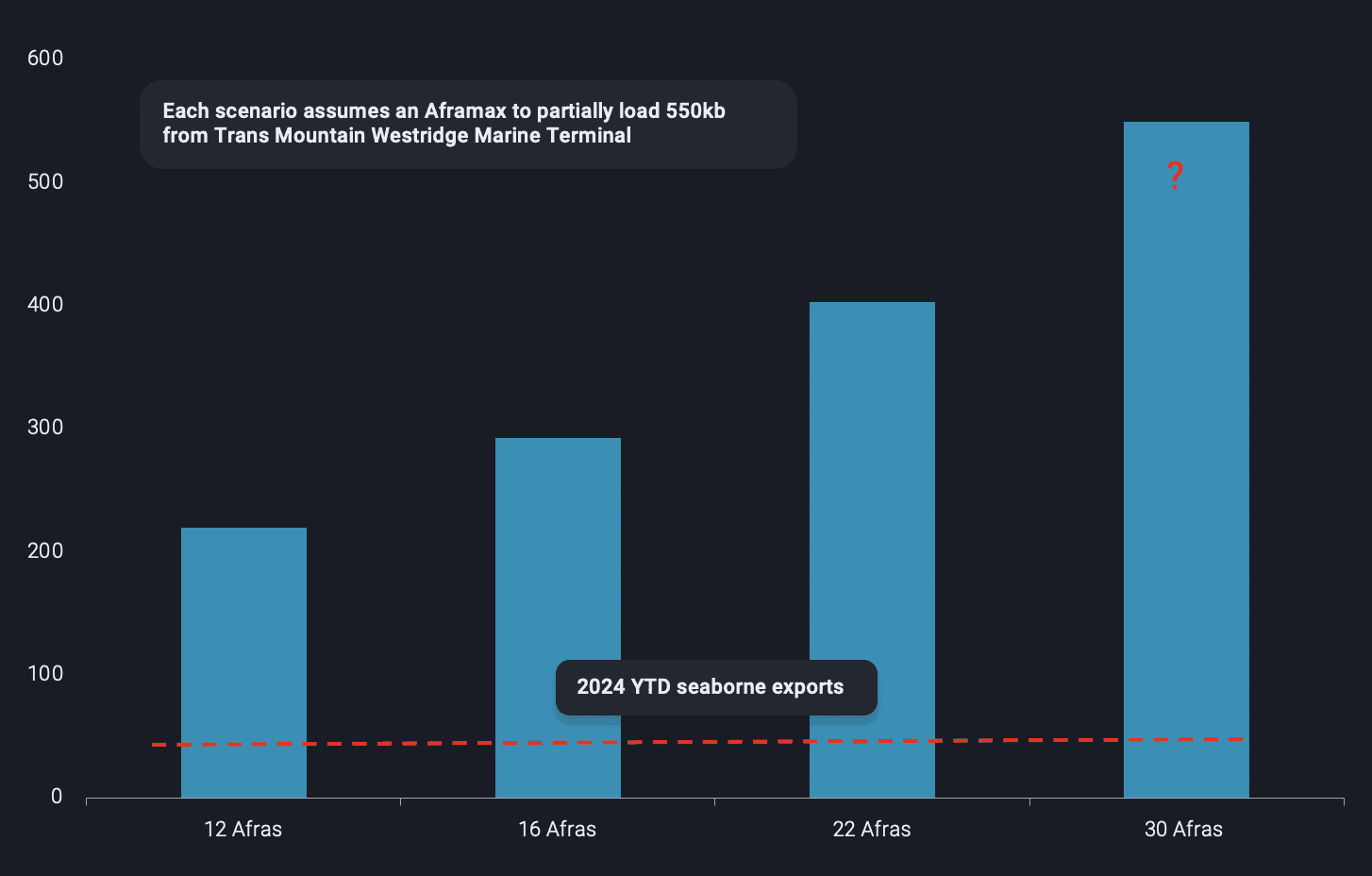

Potential seaborne crude exports per month from Vancouver post TMX start up (kbd)

The TMX start-up has driven Mars oil prices to a 2-week high (Bloomberg) on fears of lower sour crude arriving into the US Gulf Coast. According to Vortexa data, in 2023 approx. 200kbd of Western Canadian crudes were exported out of the US Gulf Coast as opposed to only 40kbd from Vancouver, BC. TMX plans to change this by being able to export directly to Asia from Vancouver and so far there have been reports of cargoes being bought by Chinese players such as Unipec, Sinochem and PetroChina and by Indian refiner Reliance, with the first “Aframax” expected to load in the 2nd half of May.

The reason we emphasize “Aframax” is that it is the only vessel class that is able to load from Vancouver’s Trans Mountain Westridge Marine Terminal. Trans Mountain expects to load around 30-40 Afras a month from this terminal which currently only loads 2-3 Afras a month. To demonstrate a more realistic scenario, we decided to undertake an analysis to showcase what this would mean for export flows out of Vancouver. We have also baked in the port draught restrictions which only allow an Aframax to load up to 550kb as opposed to a full load of ~700kb. These Afras then will either have to travel directly to Asia and ballast back to Vancouver which will mean higher freight cost or travel to US West Coast refiners, a likely scenario we shall discuss further. Another option is ship-to-ship transfer to a VLCC which is not possible off Vancouver due to rough seas, so the likely option will be to STS further south near Panama or California (where permission is required from California authorities for loading VLCCs).

That being said, it does not mean that the TMX start-up will only have a limited impact on Western Canadian crude exports. The pipeline will still displace some barrels that were exported via rail, ~120kbd as of 2023 according to data from Canada Energy Regulator (CER). TMX is expected to replace the portion of these exports that goes to Washington state refineries. The flow on the Sumas leg of the pipeline where the Trans Mountain connects to the Puget Sound Pipeline (240kbd capacity) and delivers to the four Washington state refineries is already at capacity (230kbd of crude was delivered via the pipeline according to 2023 data reported to FERC), with most of these barrels being upgraded light sweet crudes. These flows are expected to continue on the older pipeline. Additional import barrels into Washington state will have to take the seaborne route via the TMX pipeline.

We believe the first two scenarios of 12 to 16 Afras are more likely in terms of seaborne exports, meaning seaborne exports of ~300kbd out of Vancouver every month. Oil should travel to the closest markets first which in this case should be the US West Coast, where it will first impact the long haul barrels from Iraq and Saudi Arabia and then sour crudes from LatAm. ANS flows to the US West Coast should also get impacted and might have to find buyers in Asia. What needs to be seen is how much of this additional flow to the west on TMX will pull Canadian barrels away from the US Gulf Coast fueling further tightness in that market.

Refinery upsets allow Mexico to increase exports for now

Coming to Mexico, which has further fueled this tightness by consistently exporting less crude since November 2023 with exports in April 2024 reaching 625kbd, their lowest in the last 3 years. The key reason behind this move by Pemex is to increase domestic production of refined products by increasing the utilization of domestic refineries and the upcoming start-up of their new 340kbd Dos Bocas (Olmeca) Refinery. So far they have managed to raise their refinery utilisation to 65% in March, in comparison to usually below 50% in the past. But recent fires at Salina Cruz and Minatitlan refineries led to Pemex making 330kbd of crude available for exports to US refiners which should bring Mexico’s crude exports up again but not to pre-October 2023 levels. The increase in motor fuel imports for the month of April points towards the rising demand for motor fuels in the country and the government’s push for producing these barrels domestically on the back of upcoming elections in June are likely to keep some sour crude barrels away from US Gulf Coast markets.

Medium and Heavy Sour imports pick up

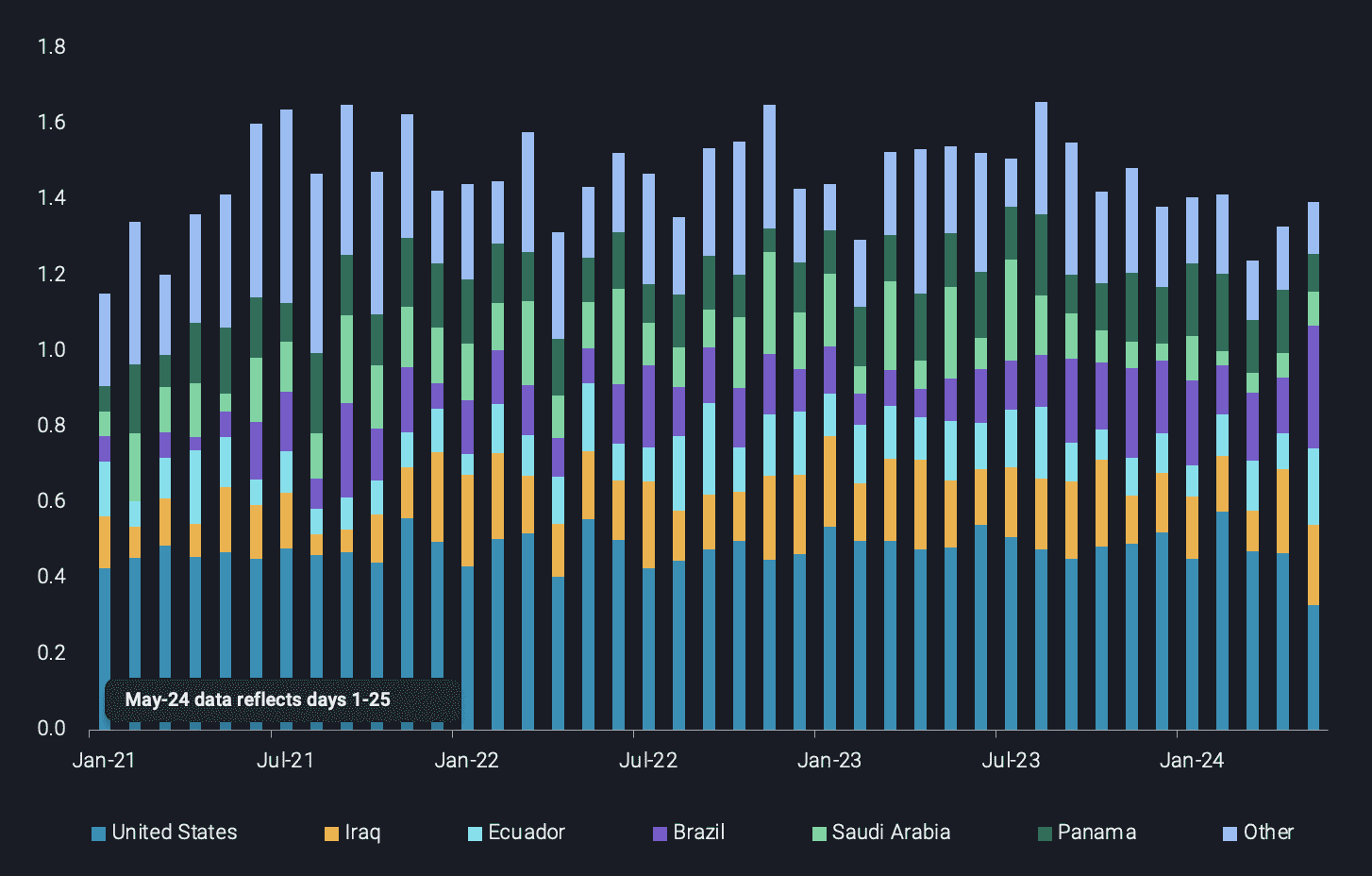

Medium and Heavy sour crude imports into the US Gulf Coast seem to be picking up as refinery maintenance comes to an end. Vortexa data for May (days 1-25) suggests that imports are set to increase by 20% vs April 2024. This is driven by an influx of Saudi barrels which are expected to increase by 500kbd m-o-m in May (days 1-25), more than double the imports in April at 190kbd. On the flip side, imports from Mexico were at their lowest levels historically for the past two months but as discussed above an additional 330kbd of crude from Mexico is now available for exports in May. But going back to Saudi crudes there are six VLCCs carrying Saudi crudes that are either discharging or waiting to discharge in the US Gulf Coast. The majority of these barrels are destined for Motiva Port Arthur Refinery or storage, with this influx likely to relieve some pressure on sour crude prices. Going forward, in a scenario where the Olmeca refinery does not start-up for another 6 months and the exports via TMX from Vancouver remain at 300kbd, the current tightness in Gulf Coast sour crude markets could quickly ease.