Clean tankers seeking stability after a turbulent 2022

Clean tanker markets have seen a freight rate decline across the board so far this year despite strong momentum in late 2022. Our freight team analyses the drivers behind this development and what lies ahead for clean tanker markets in 2023.

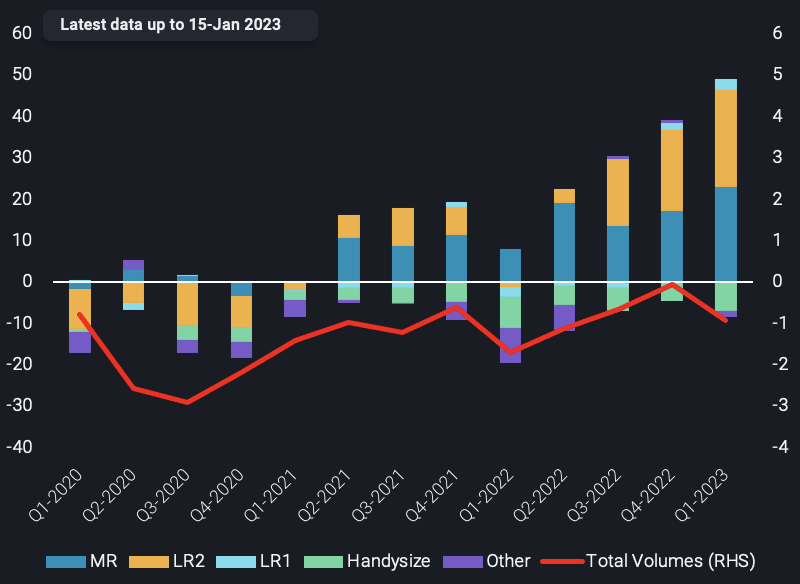

CPP tonne-mile (bn, LHS) and volume (mbd, LHS) changes vs 2019 average

What we have seen so far

As we approached the end of 2022, clean tanker tonne-miles showed another increase relative to pre-pandemic levels. This was driven by high levels of seaborne diesel exports globally. Specifically, Chinese clean exports increased on the back of record high quotas and Europe rushed to secure both diesel cargoes out of the Baltic as well as from alternative long-haul sources, ahead of the Feb 5 ban on Russian oil products. In January, preliminary data for Q1 shows an increase in CPP tanker tonne-miles, but a simultaneous dip in export volumes for CPP. It is likely that this preliminary increase in tonne-miles represents volumes which departed late last year and are still on the water. The current dip in export volumes indicates a slowdown in the CPP market, which is further reflected in the considerable decline of freight rates across the board.

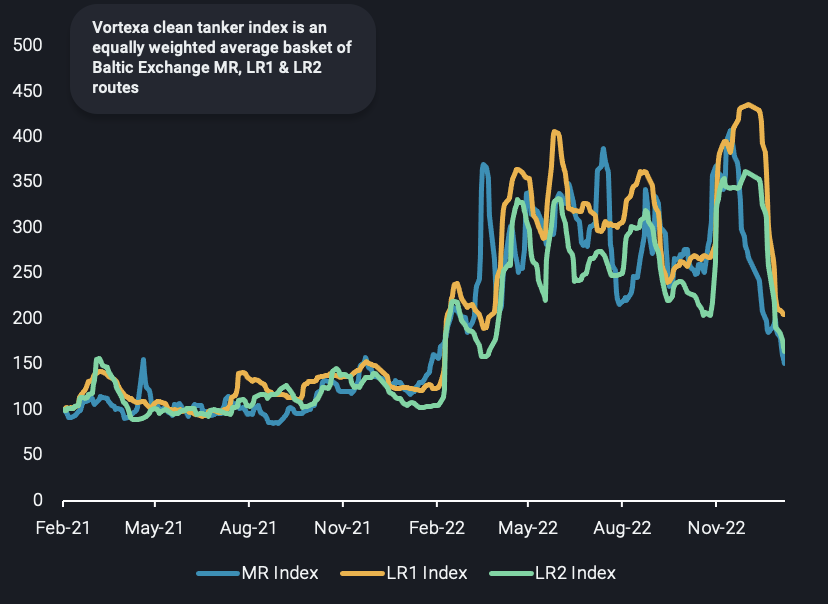

Vortexa index of clean freight rates per vessel class

Although vessel demand fundamentals played a role in this increase in clean rates during 2022, uncertainty around Russia-related reshuffling and energy security contributed significantly to higher shipping costs. Currently, rates are at a 10-month low but remain above 2021 levels, as the volatility seems to get milder.

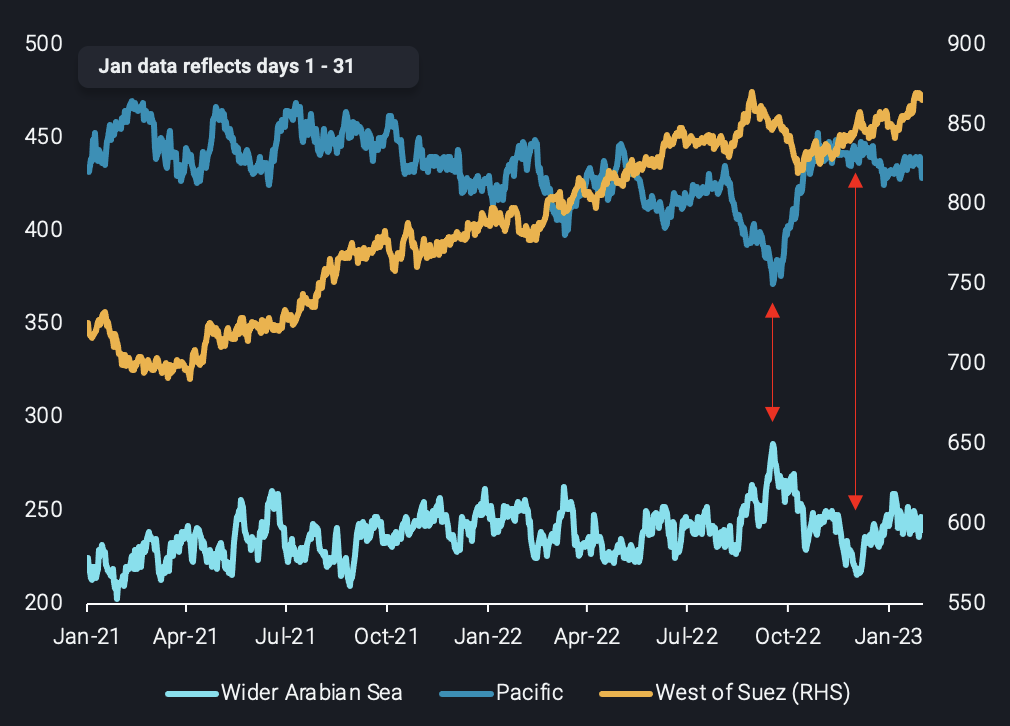

MR tanker supply glut forming in the West

Distribution of MR tankers per selected region (no. of vessels)

MR tankers benefited from increased tonne-mile demand on short-haul routes towards Southeast Asia due to record CPP exports from China in the final quarter of 2022. This saw a sharp redistribution of MRs from the Wider Arabian Sea region to the Pacific. However, increasing Chinese domestic demand and a change in the official export policy is cooling off CPP exports. This has seen MR tonne-miles from China to Southeast Asia drop sharply by around a third in January.

In the West of Suez, MR vessel supply is trending higher, which is partly due to growing utilisation on the Russia-to-Europe route as European countries secure their last cargoes of Russian diesel ahead of the approaching oil products ban. In the Atlantic Basin, diesel tonne-miles on MR tankers out of the US Gulf have fallen sharply this year, reflecting the effects of past refinery outages and upcoming spring maintenance on tanker demand. Additionally, as Russia-to-Europe MR utilisation draws to a close, more MR tankers will likely enter markets in the Pacific as well as the Atlantic Basin, increasing tanker supply as well as competition.

Overall, MR tanker demand is declining, with little support to the upside at least for the next couple of months. This is currently causing a supply glut of MRs in the Pacific as well as in the Atlantic Basin, as there is currently no incentive for East-to-West or vice versa tanker supply shifts.

Diesel reshuffling supports LRs, but naphtha causes headwinds

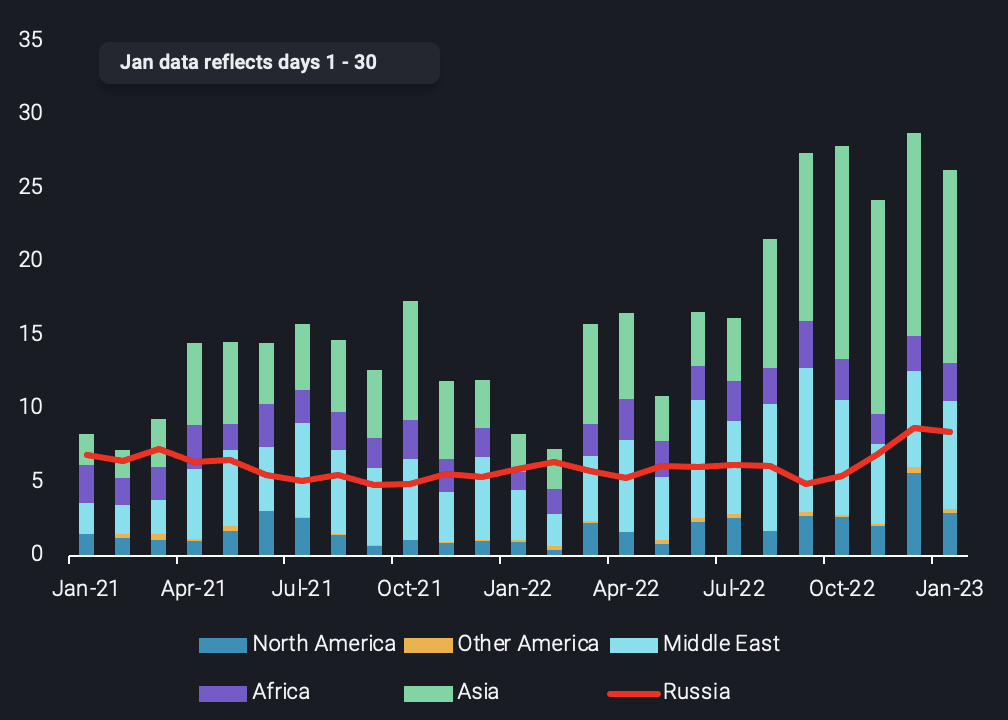

Similarly to the MR fleet, robust CPP exports from China also benefitted LRs, due to the increased demand for longer voyages to regions such as Europe. These longer voyages in turn point to a wider supporting factor for LR2s: Europe’s diesel diversification.

EU seaborne diesel tonne-miles by selected shipping region (bn)

Diesel tonne-miles to the EU from origins excluding Russia are at an almost three-year high, demonstrating Europe’s desire to diversify supplies, offering further support for the LR2 tanker segment due to longer voyages from regions such as India and the Middle East. Nevertheless, the expected drop in Chinese CPP exports will have a negative effect on LR tonne-mile demand.

Russia’s reshuffling of its flows provides some support to LR2s. This support could be potentially more pronounced as more cargoes head further away from Europe such as North, West or East Africa, for example.

While a particular strength is evident in the diesel market, the performance in other products is less supportive. A particular area of weakness for LRs is naphtha flows to East Asia, which have seen tonne-mileage decline by 25% m-o-m since the start of 2023 as cracker utilisation has remained lacklustre. This could see more LR2 tonnage enter middle distillate markets and potentially cap tanker earnings in the short term if diesel demand cools.

What lies ahead for clean tankers?

Looking ahead, CPP volumes are likely to move lower and stabilise after the December peak in exports, as the current freight levels suggest. Given the particular emphasis on diesel volumes last quarter, as well as a mild recessionary environment, we may see a shift away from diesel as global supply exceeds demand.

As a result of Russia’s reshuffling of flows and Europe’s diversification of diesel sources, LR2 tankers are likely to dominate the diesel market going forward. However, in this well supplied market, and with prospective declines in Chinese CPP exports, diesel trade could see a slowdown in the coming months. While MR tanker activity remains subdued for now, employment will likely pick up on transatlantic routes. Additionally, in the Pacific, a recovery in the jet market could offer support for tanker demand in the region, leading to the conclusion that MR tankers will be utilised increasingly in non-diesel, inter-regional markets.

These demand factors could absorb excess tanker supply and decelerate the current decline in clean freight rates. With the EU oil product ban around the corner, the rates could see more volatility once again as CPP reshuffling continues. A potential rise in trade flows for other clean products bar diesel – where MRs could find solace – might be able to balance the market and limit volatility in freight rates. This could see clean tanker freight rates settle at lower levels than 2022, but still above the averages seen in 2021.

Written by Dylan Simpson, Freight Analyst, Mary Melton, Graduate Freight Analyst and Ioannis Papadimitriou, Senior Freight Analyst