Crude tanker fundamentals signal short-term support, strength in Atlantic Basin

Recent increases in crude tanker rates may signal the end of the dire straits of Q3, but despite bright spots in the Atlantic Basin freight rates are unlikely to soar to high levels seen in Q4 2022 due to limited MEG demand.

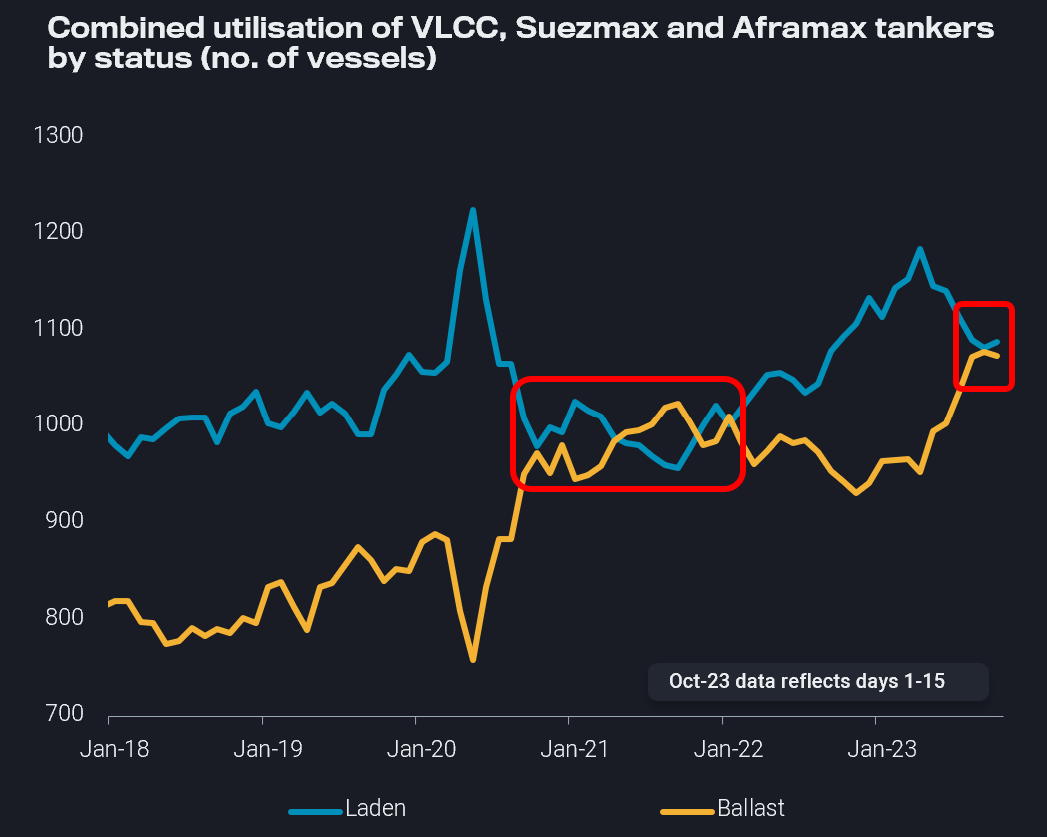

Throughout 2023, the number of laden crude tankers has continuously declined and is currently at par with ballast crude tankers. Since January 2018 parity was reached for the main crude tanker classes only during the Covid period and currently since August, driven by limited crude supply, especially in the context of OPEC+ voluntary cuts. Despite these unfavourable market fundamentals, freight rates have rallied over the past week and are currently at levels last seen in Q2. Clues in recent tanker behaviour can offer us insight into what is happening and whether this rally is likely to continue.

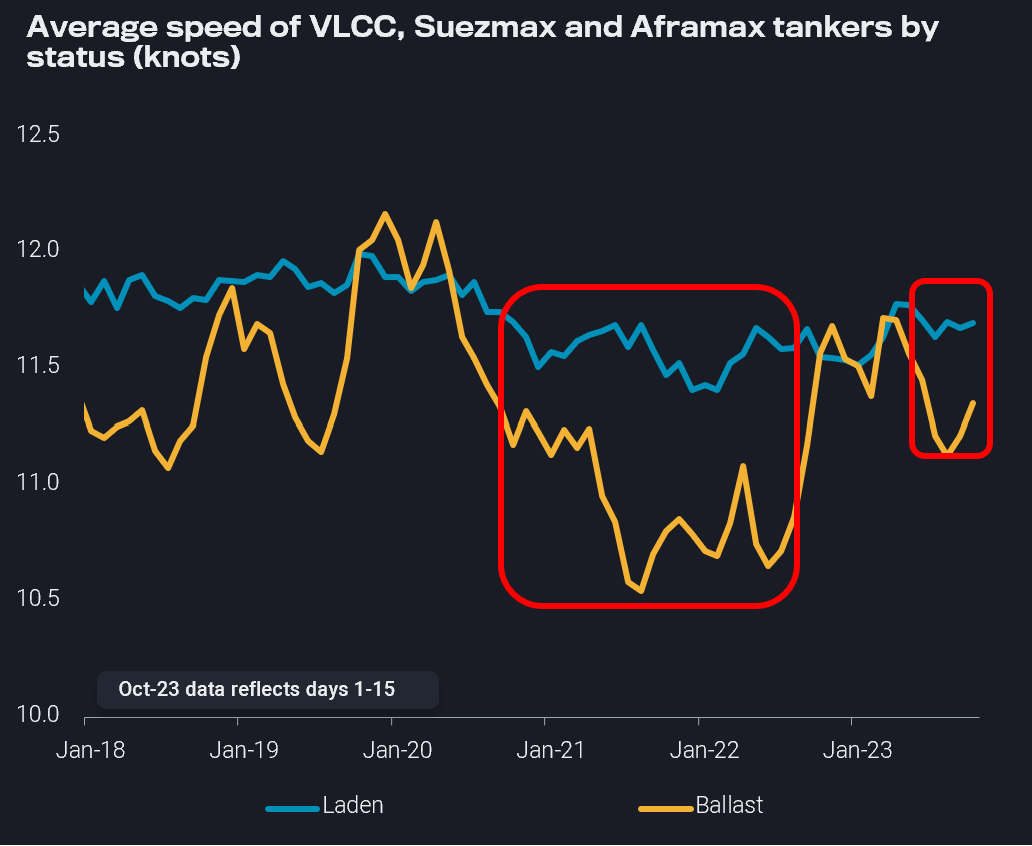

Ballast vessel speeds declined continuously since April, reaching an 11-month low in September. Before that, the only period since 2018 of sustained declining ballast speeds was during the Covid period. Declining speeds are a signal of a weak market, as vessels slow down to cut down on bunkering costs in a weak freight environment. However, during the first half of October, average ballast vessel speed has increased to a three-month high. This gives us an early indication of vessels speeding up to capitalise on higher rates, reducing vessel supply requirements.

Recent tonne-mile demand strength for US Gulf loadings offers some short-term optimism in addition to the global ballaster speed increase. New Chinese crude import quotas could offer a slight boost, and bookings East have increased (source: Argus). At the same time, Atlantic Basin vessel supply is limited as the number of ballasters to the West of Suez has continued to decline, likely providing further momentum for increasing rates as US Gulf exporting availability increases.

However, this pocket of strength over in the Atlantic Basin is not likely to herald sustained crude tanker demand through the remainder of 2023. Though increased, China’s bookings are now at normal levels after a slow August/September, and the country will likely continue with stock drawdowns instead of seaborne imports. Additionally, the nexus of tonne-mile demand comes from the Middle East, with global crude tanker tonne-miles from MEG origins contributing to around one-third of all crude tanker tonne-miles. In the context of ongoing Saudi cuts, Saudi crude exports have recovered from August low levels. Nevertheless, we are unlikely to see crude tanker rates approach the multi-year highs reached in Q4 2022 unless volumes from the MEG continue to increase significantly. Ultimately, there is also uncertainty due to the possibility of rising tensions in the Middle East, which could introduce significant volatility to the crude tanker market.