Have CPP rates reached an inflection point?

What are the current pillars of CPP tankers and how strongly will they support rates for the remainder of the year?

CPP tanker tonne-miles ended the first quarter of the year on par with Q4 2022 (0.1% decrease). When comparing tanker demand to pre-Covid levels (2019 average) there is a distinct trend that has emerged. After a gradual increase for the majority of 2022, global CPP volumes are hovering around pre-pandemic levels over the past two quarters. On the other hand, tonne-miles are clearly surpassing 2019 levels, pointing to the fact that the length of voyages is weighing more to shape tanker demand currently, than it did in the pre-pandemic period.

CPP tonne-mile change per vessel class (LHS, bn) and global seaborne CPP exports change (RHS, mbd) vs 2019 average

As illustrated by the chart, two vessel classes have outperformed the others: MR and LR2s. This is mainly a product of the unwinding relationship between Europe and Russia in the CPP (specifically middle distillates) trade. LR2 tankers are increasingly operating on middle distillate routes towards Europe (primarily from India and the Middle East), whilst MR tankers have taken the spotlight for diesel/gasoil flows out of Russia which are travelling further post EU-ban (e.g. West Africa and South America).

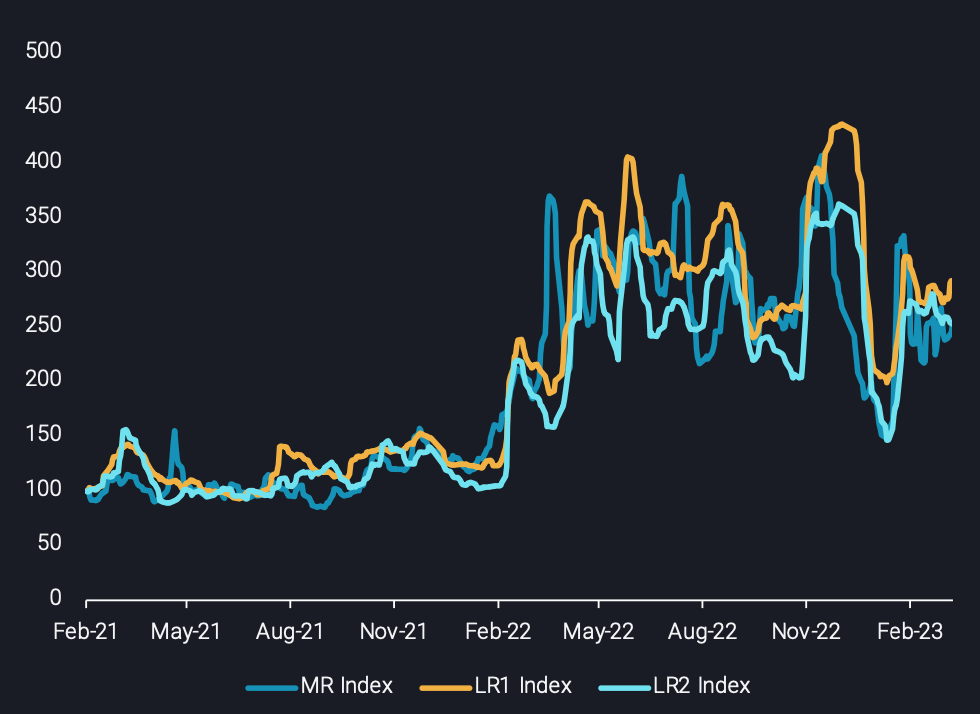

Similarly, the volatile freight rates seen in the majority of 2022 reflect the plateauing behaviour observed in tonne-miles, following a surge post-2021. This begs the question, what’s in store for CPP freight rates for the year?

Vortexa Clean Tanker Index per vessel class (Reference data = Feb 2021 where index = 100)

Global diesel imports continue to break seasonal records, while energy security fears in Europe have dissipated, partly owing to the fact the region found alternative suppliers relatively easily and partly due to a milder than expected winter. Evidently, this casts doubt on whether these record-high diesel flows can continue. At the same time, refined product imports in key consuming hubs such as North America and South East Asia are trending lower. Finally Russia’s record-high oil exports recorded in March will likely slide as domestic demand makes a comeback post-winter season along with a refinery maintenance schedule which will likely curb CPP exports out of the country. The lack of seaborne product demand will likely lead to a slowdown in overall CPP tanker trade. Nevertheless seasonal trades in the Western hemisphere, such as jet/kero flows to Europe and North America or transatlantic gasoline flows could provide a limited upside for tanker demand.

From a vessel supply standpoint a different story is unfolding which looks more encouraging for shipowners and operators alike. Analysis from our continuous tracking of Russian developments suggests that the number of vessels joining the Russian CPP trade – especially on the MR side – continues to rise, effectively tightening the supply of the “mainstream” trade. Additionally, the behaviour of these vessels – which perform not only long but also round and inefficient voyages – underlines the “stickiness” of the fleet in this rather opaque trade which results in further increases in fleet requirements. And on top of this, 2023 deliveries of MRs are set to be at their lowest since 2002, according to figures from Braemar.

Overall, it might be possible that the effect of tonne-miles due to reshuffling flows post-EU ban has largely already materialised. Softer demand fundamentals than those witnessed in the first quarter of the year, could mean that CPP freight rates have peaked. However, a prospective fall in freight rates will not be a dramatic one, as fleet supply restrictions are ultimately providing a floor at higher levels than the ones reached in 2021.