Is there light at the end of the tunnel for crude tankers in 2023?

As crude tanker rates reach new lows for 2023, we drill down into the drivers behind this, how this has shifted dynamics within the crude tanker market, as well as how support could materialise in the last quarter of the year.

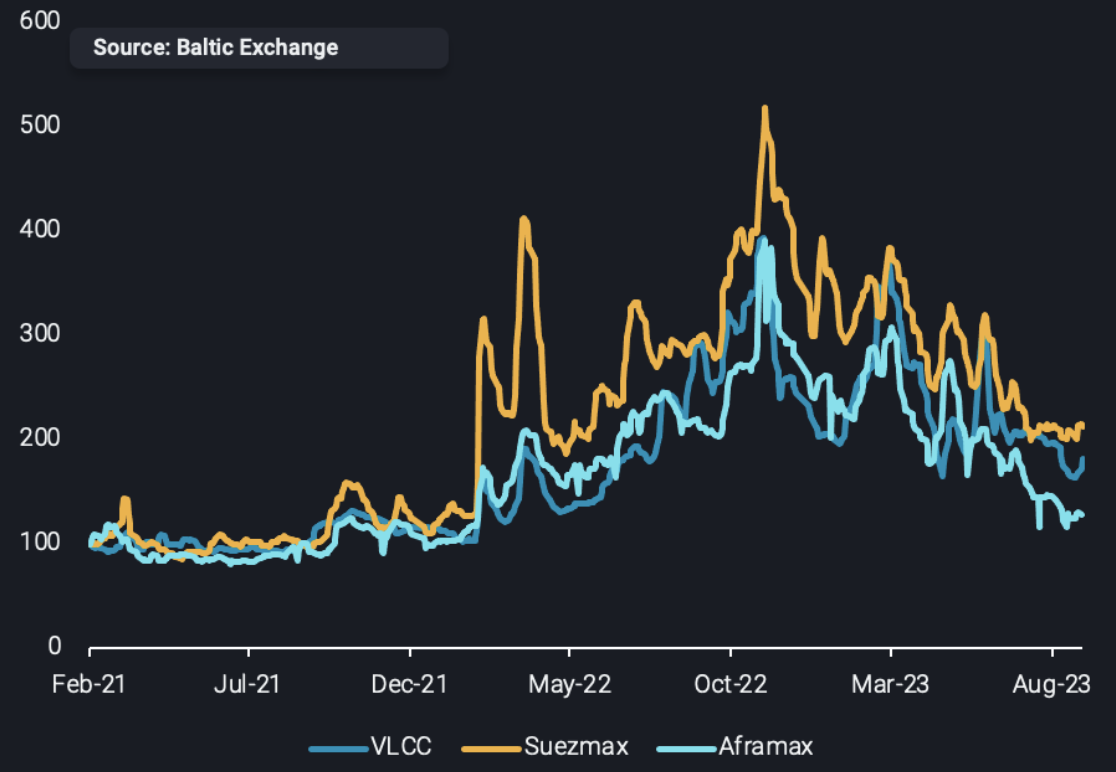

Crude tanker rates have been sliding across the board in the last couple of months. Since July, indices for the three main crude tanker classes have dropped by 20%, 15% and 30% for VLCCs, Suezmaxes and Aframaxes respectively, reaching new lows for 2023. This comes in the wake of two key demand side developments: the implementation of Saudi-led OPEC+ cuts as well as a seasonal decline in Russian crude exports. This has led to lower utilisation of crude tankers and triggered an increase in global crude tanker supply, adding further downward pressure to freight rates. This situation has seen further reshuffling of crude tanker dynamics in key regions.

Crude tanker indices per vessel class

Crude tankers show adaptability, switching to alternative markets

In the Aframax and Suezmax segments, most of the decline in utilisation stemmed from lower levels of Russian trade. This has prompted these tankers to participate in other markets, most notably in the Middle East according to data from our freight API/SDK. This has supported utilisation of these tanker classes out of the region, particularly towards the Mediterranean. However, due to OPEC+ cuts, the opportunities for tankers in this trade remains limited. Evidently, the increase in tanker demand has already begun to falter. As more tankers look to participate in Middle East-to-Med trade, tanker supply in the Middle East could continue to build. The likelihood of tankers previously involved in Russian trade migrating to growing transatlantic trade remains low, however, displaced “mainstream” tankers in the Middle East-to-Med trade could be pushed towards the Atlantic Basin.

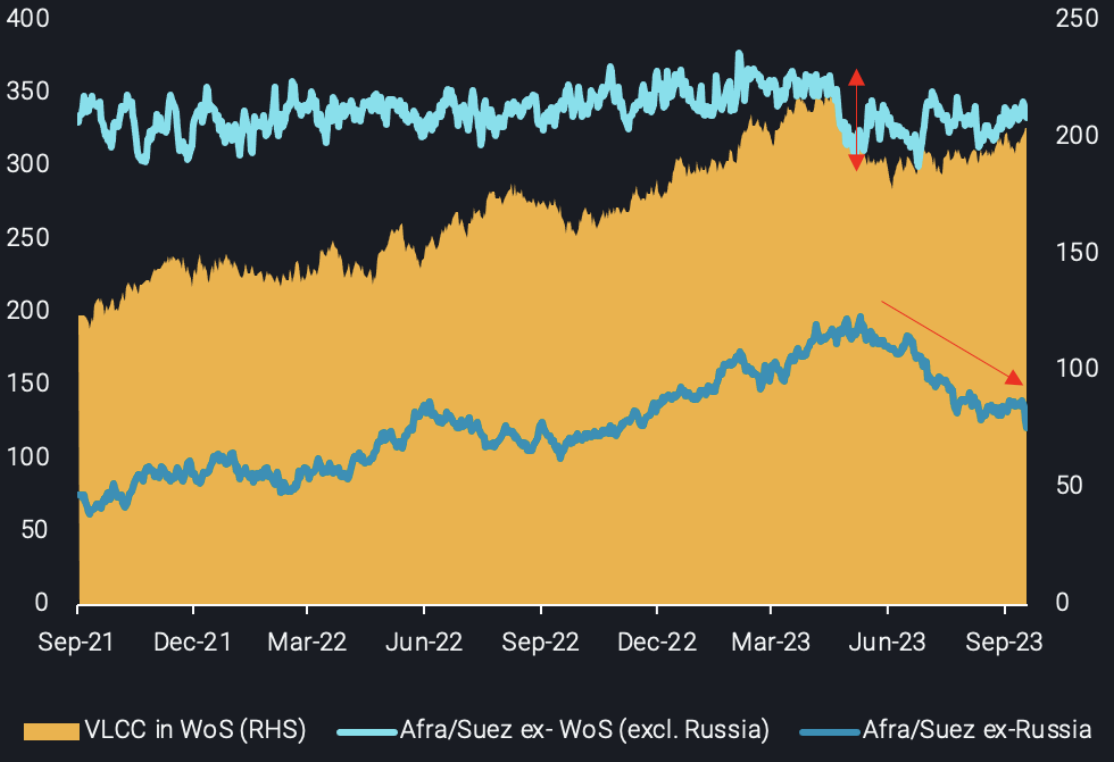

The VLCC segment has borne the brunt of reduced exports out of Saudi Arabia, which is reflected in their declining tonne-miles out of the region. This has triggered a rebound on the migration of the VLCC fleet into the West of Suez, which is an attractive, albeit smaller alternative for ship owners given the robust crude flows towards Europe. That said, the transatlantic trade is not able to fully absorb this additional tanker supply and support crude tanker rates at Q2 levels.

Aframax/Suezmax utilisation from selected West of Suez origins (LHS, no. of vessels) vs. VLCCs located in West of Suez (RHS, no. of vessels)

Rising crude prices and seasonality to the rescue?

Preliminary month-to-date export figures suggest a potential m-o-m increase in Saudi and Russian crude exports for September. Although no official announcement has been made on whether this spells a recovery in export levels, it could indicate that crude tanker rates have reached their 2023 floor. Moreover, with crude prices trending higher, a reduction of the OPEC+ voluntary cuts could be on the cards. This, coupled with a seasonal recovery in Russian crude exports (as these normally trend higher in Q4) could provide enough demand side support to absorb excess tanker supply, supporting crude tanker rates as we close out 2023.