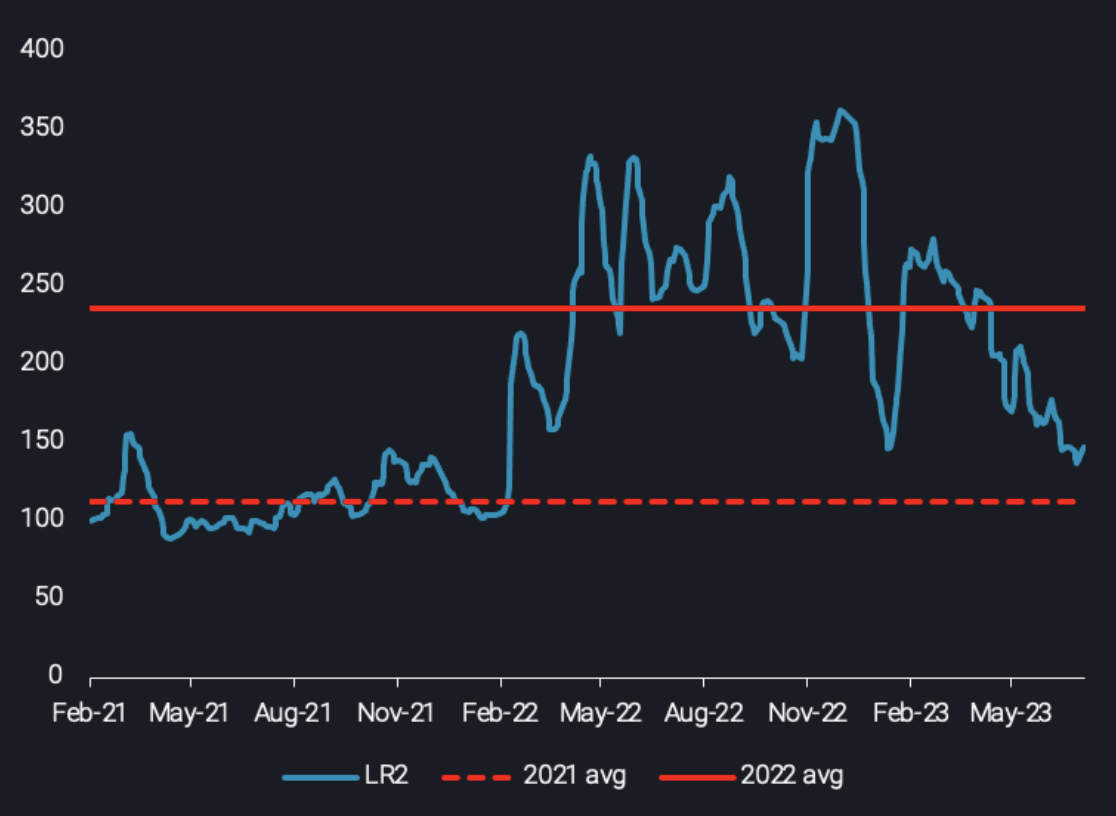

LR2 rates reach pre-war levels as utilisation in key markets subsides

LR2 freight rates have considerably softened from levels seen in Q4 2022, around 65% from late December peaks. The last time that trademark route LR2 assessments were lower than current levels was at the onset of the Russian invasion in Ukraine in late February 2022.

Vortexa LR2 tanker index

The strength in rates experienced late last year was partially caused by uncertainty from the EU’s embargo on Russia’s oil imports impacting Europe’s energy security and Russia’s reshuffled flows. With these questions largely resolved, rates have stabilised at lower levels. That is not to say, however, that fundamentals did not contribute to the current downward trajectory.

Evidently, global LR2 tonne-miles have dipped in July for the 4th consecutive month since peaking in March, according to preliminary figures. This progressive drop in employment has been be reflected in 3 key flows where LR2 had found support previously: Diesel flows towards Europe, CPP flows out of Russia as well as the naphtha trade to Asia

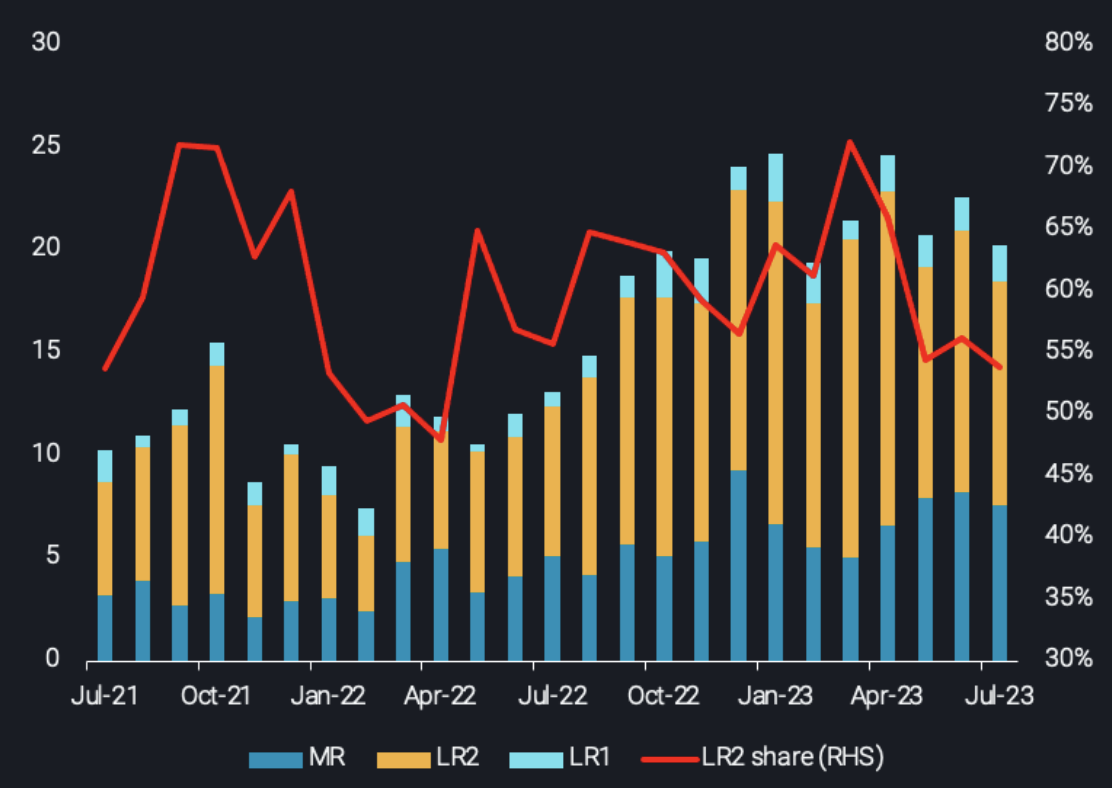

Late last year Europe commenced importing diesel increasingly from places such as India and the Middle East – and also partially from China for a brief period. These long-haul cargoes were carried onboard LR2s, boosting the demand for the vessel class. As Europe, however, recently turned its focus on the US for diesel and as these transatlantic cargoes are predominantly carried on MRs, LR2 market share for flows to the region narrowed.

Diesel tonne-miles to Europe by vessel class (bn, LHS) vs LR2 % share (RHS)

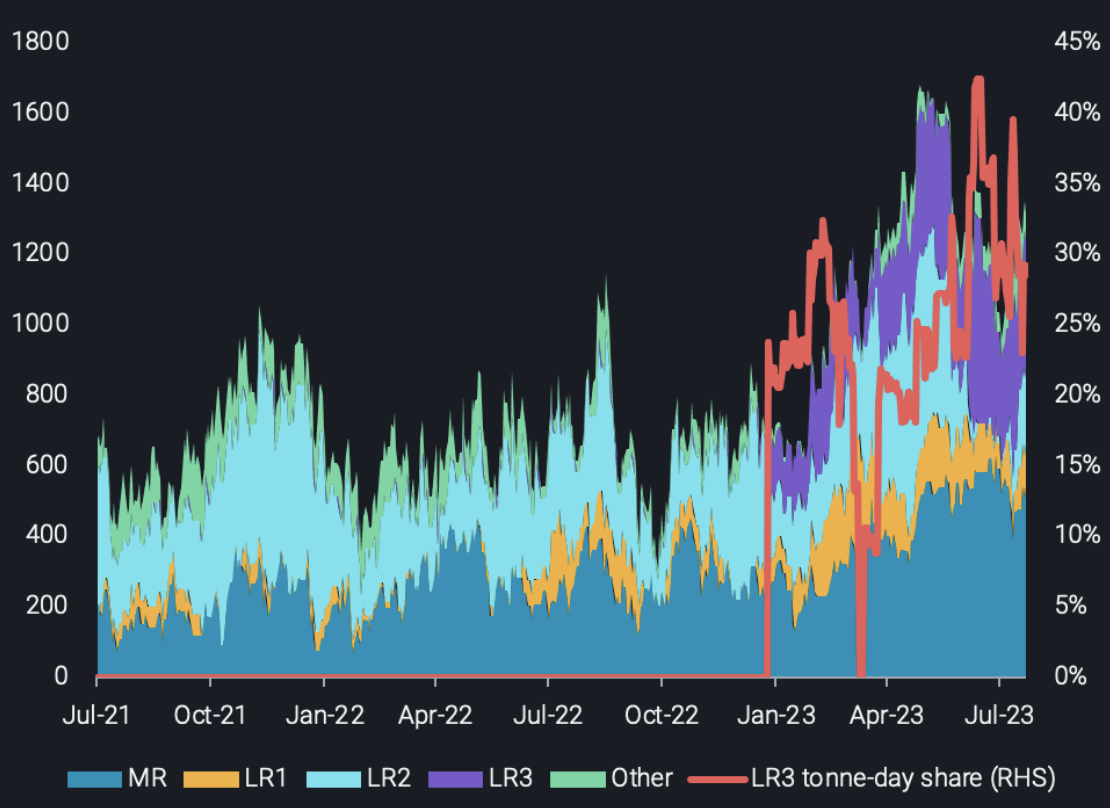

As in the non-Russian trades, LR2 tankers lost their share on the CPP Russian flows, but this time from their bigger-sized counterpart. This was mostly evident in the Russian naphtha trade where LR3s gained ground at the expense of LR2s. Since the beginning of June, the LR3 tonne-days share has averaged close to 30%, while the LR2 tonne-days share has averaged about 5%. This has forced a portion of LR2 operators to look for employment away from Russia trades.

Tonne-days by vessel class for Baltic-origin Russian naphtha (LHS, kt) vs. LR3 tonne-day share (RHS)

For now it is not clear whether these vessels will follow the pattern of some Suezmaxes where operators increasingly operate in both tiers (in Russia and out of Russia) to increase profitability, or are altogether departing the Russian trade, which adds vessel supply-side pressure for the non-Russian trades. Contrastingly, these LR3s that carried Russian naphtha to the east had ballast back to Russia, signalling that they will likely remain in the Russian trade.

These market developments are weighing further on LR2 tanker demand which have been unable to find support from its more traditional pillar, naphtha demand in East and Southeast Asia, which is ailing due to thin petrochemical margins and steam cracker maintenance.

It is not all doom and gloom for LR2 operators, however. Europe’s shift to US diesel triggered a surge of diesel flows towards Asia on LR2s, predominantly from India as well as from the new, more economical refineries in the Middle East. The introduction of these refineries could potentially trigger a consolidation in the Asian refining sector (excluding Indian and Chinese refineries). If this materialises, more CPP supplies from the Wider Arabian Sea could be channelled towards Southeast Asia and Australia, supporting LR2 demand.