LRs snatch MR business as East Asian naphtha demand remains weak

Clean tanker rates in the East of Suez have remained at a high level despite erratic demand in the region. The main driver of this situation lies on the supply side. In this insight we dive into the dynamics behind rates in the East, and link the chain of events to trace the freight rate trajectory.

Clean tanker rates in the East of Suez have remained at a high level despite erratic demand in the region. The main driver of this situation lies on the supply side. In this insight we dive into the dynamics behind rates in the East, and link the chain of events to trace the freight rate trajectory.

This year has seen incredible volatility in the freight market. After the Russian invasion of Ukraine in late February, freight rates surged across the board as uncertainty and insurance premiums took hold. Since then, freight rates have experienced volatile movements in both directions. As the complexities of the freight market continue to evolve, we focus on the recent behaviour and the fate of LR tankers.

Weak naphtha demand, unscathed freight rates

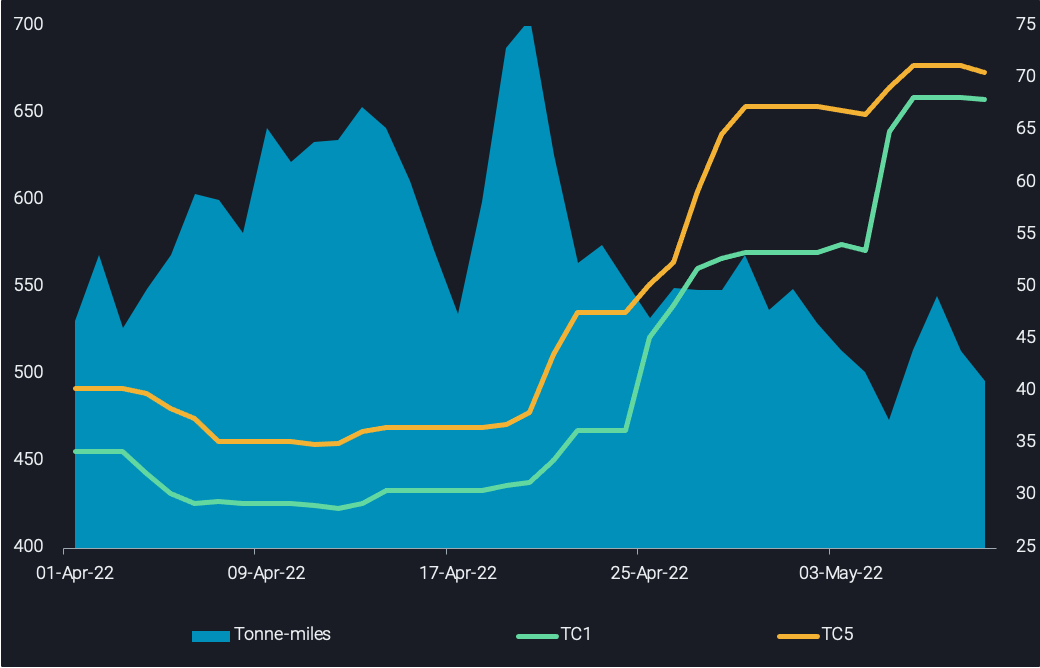

First, we begin with a look at the naphtha market. Low demand for naphtha in East Asia has persisted into Q2 of 2022, with slightly higher refinery margins in April not being sustained. Despite this low demand, LR freight rates from the MEG-to-East Asia (TC1 and TC5) have been on a rally, eventually reaching a 2-year high. This begs the question as to the factors that have contributed to this rise. The reason is twofold:

- MR tankers have been continuously heading West to cease opportunities in the Atlantic Basin.

- LR tankers are taking this opportunity to penetrate traditional MR routes away from the MEG.

LR naphtha tonne-miles (mn, LHS) vs TC1 & TC5 freight rates ($/ton, RHS)

First, we begin with a look at the naphtha market. Low demand for naphtha in East Asia has persisted into Q2 of 2022, with slightly higher refinery margins in April not being sustained. Despite this low demand, LR freight rates from the MEG-to-East Asia (TC1 and TC5) have been on a rally, eventually reaching a 2-year high. This begs the question as to the factors that have contributed to this rise. The reason is twofold:

- MR tankers have been continuously heading West to cease opportunities in the Atlantic Basin.

- LR tankers are taking this opportunity to penetrate traditional MR routes away from the MEG.

Asymmetric East-to-West MR distribution

It is not only LR but also MR tanker rates which have sky-rocketed, with gasoline and diesel demand in Southeast Asia showing strength – reflected in the Asian crack spreads – after many countries in the region re-opened international borders and eased Covid restrictions in April. Another significant contributor to this rise in rates is the repositioning of MRs, which have been flowing towards the Western Hemisphere continuously. There are now far fewer MR tankers in the East of Suez than in the West, and the gap between these numbers has been growing steadily since they began to diverge in February this year. With MR supply in Asia driven into the ground, and demand for vessels on East Asian routes, the opportunity for LRs to step in has presented itself.

LRs cannibalising MR routes

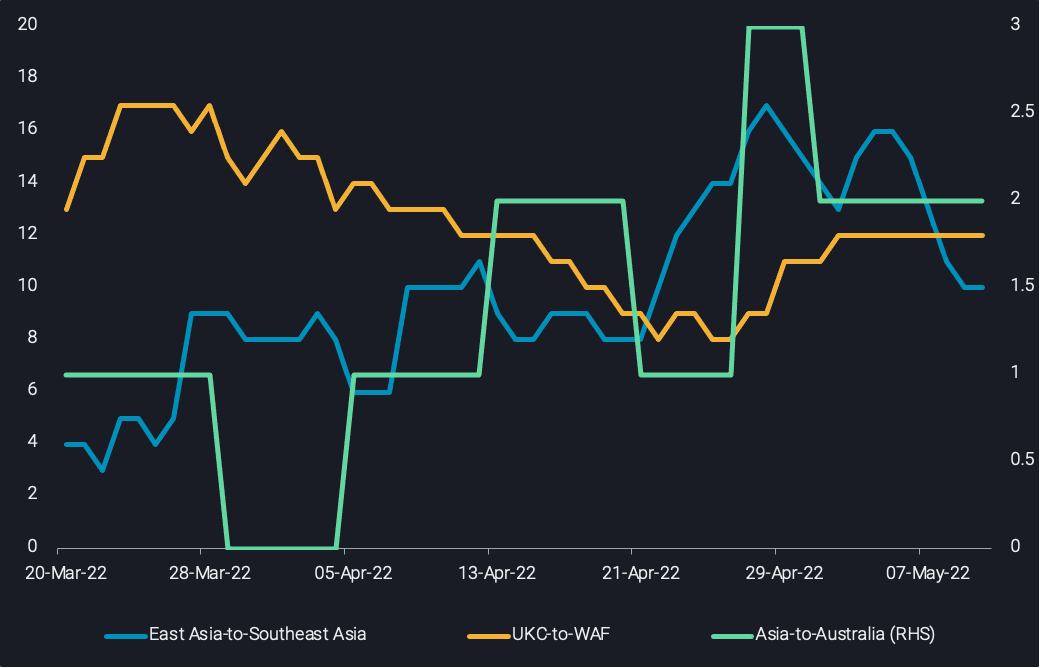

Due to the higher utilisation of MRs in transatlantic flows, LR tankers are beginning to gain market share on routes which are traditionally dominated by MRs, despite the shorter distance of these voyages. This is particularly clear in three routes highlighted by our utilisation screen:

- On the East Asia-to-Southeast Asia (TC11) route, LR tankers have increased their tonne-mile share significantly, with gasoline-carrying LR2s leading the charge.

- The jet/kero flows towards Australia have been ramped up recently, with flows recording their highest barrels per day since December 2019. Similarly to TC11 above, LR2s seem to be the main vessel class stepping in, as the MR tonne-mile share deteriorates.

- Third on the list is the CPP route from the UKC to West Africa. Here we see a general lowering of MR and LR tonne-miles since April. However, as the MR and LR tonne-miles on this route begin to rebound, the MR share has clearly not resurfaced, and this time it’s the LR1s and LR2s sharing the stage as they increase their market share on the route.

LR utilisation on various MR routes

Outlook

The strength in CPP freight rates in the East is almost certainly due to supply pressure on LRs in the East of Suez, particularly in the MEG, where LR availability has been declining steadily since mid-April. The higher freight rates due to declining LR vessel supply in MEG could produce attractive opportunities for shipowners if naphtha demand picks up due to higher gasoline reforming margins in East Asia.

With the MEG refineries ramping up runs after their maintenance season, CPP exports are likely to pick up, with slightly more barrels per day already being loaded in early May compared to April. This in turn will derive further demand for clean tankers, and with vessel supply already thin, this will likely lead to more upward pressure on clean tanker rates in Q2 of 2022.