Observations from an autumn of Panama Canal transit woes

We examine key takeaways from ongoing Panama Canal transit issues.

Panama Canal transit issues appear to be here to stay. The Panama Canal Authority is further reducing the number of transits in January and again in February, and booking fees to secure slots are breaking records. Throughout November we observed significant declines in transits for all oil and gas carriers through the canal. The current number of daily transits is about 40% lower than at the start of November, reaching yearly lows, and this follows from congestion issues which have fluctuated in severity since August. After an autumn of this new reality of decreased transits, we examine some key takeaways.

MRs increasingly transiting from the US Gulf to West Coast LatAm via alternate waypoints

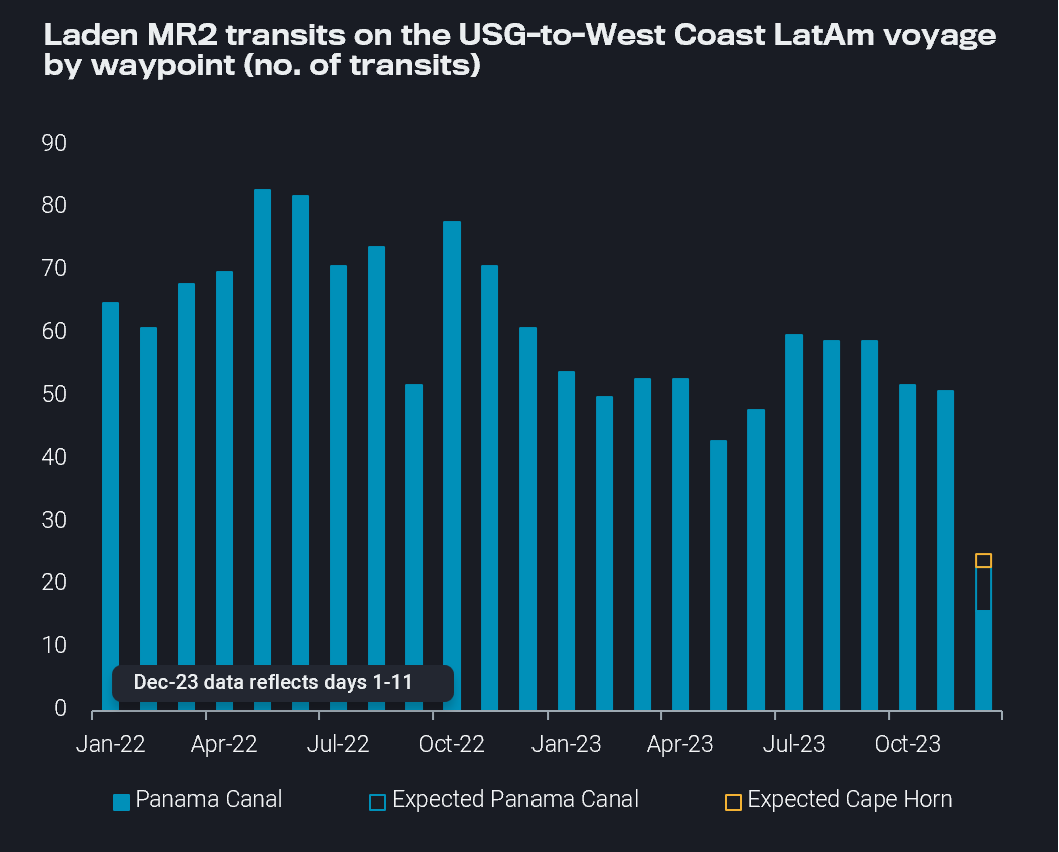

Since securing transit slots remains difficult and astronomically expensive, some MRs are forgoing the Panama Canal and transiting via Cape Horn, thereby adding days and thousands of nautical miles to the voyage length. Two tankers are currently heading towards Cape Horn (GREEN SKY and CURURO) and are expected to transit, underscoring the exceptional circumstances created by the lack of Panama Canal transit slots. Before December finishes, it is likely we will see even more tankers utilise this route.

Laden MR2 transits on the USG-to-West Coast LatAm voyage by waypoint (no. of transits) (Retrieved via Freight API/SDK)

Transpacific MR voyages not yet materialising, but could increase again

This begs the question, if MRs are taking desperate measures to reach West Coast LatAm (South America West Coast, West Coast Mexico), have we seen a concurrent increase in transpacific utilisation from APAC to West Coast LatAm? So far, transpacific MR utilisation APAC-to-West Coast LatAm has remained low. We have yet to see a repeat of the massive increase in tonne-mile demand in Sep/Oct for road fuel to West Coast Latam. However, recent broker reports reference higher enquiries for this route, so charterers may be considering it as a viable option instead of transiting around Cape Horn. A handful of diesel cargoes are currently en route from East Asia to South America West Coast, but tonne-mile demand for transpacific MRs to West Coast LatAm is currently about 80% below the peak reached in October. China’s CPP exports are currently still prioritised for Asian markets and capped by limited export quotas, making a considerable rise in exports to West Coast LatAm unlikely, at least not before next year’s CPP export quotas are released.

MRs transiting back to the USG from West Coast Americas via alternate routes

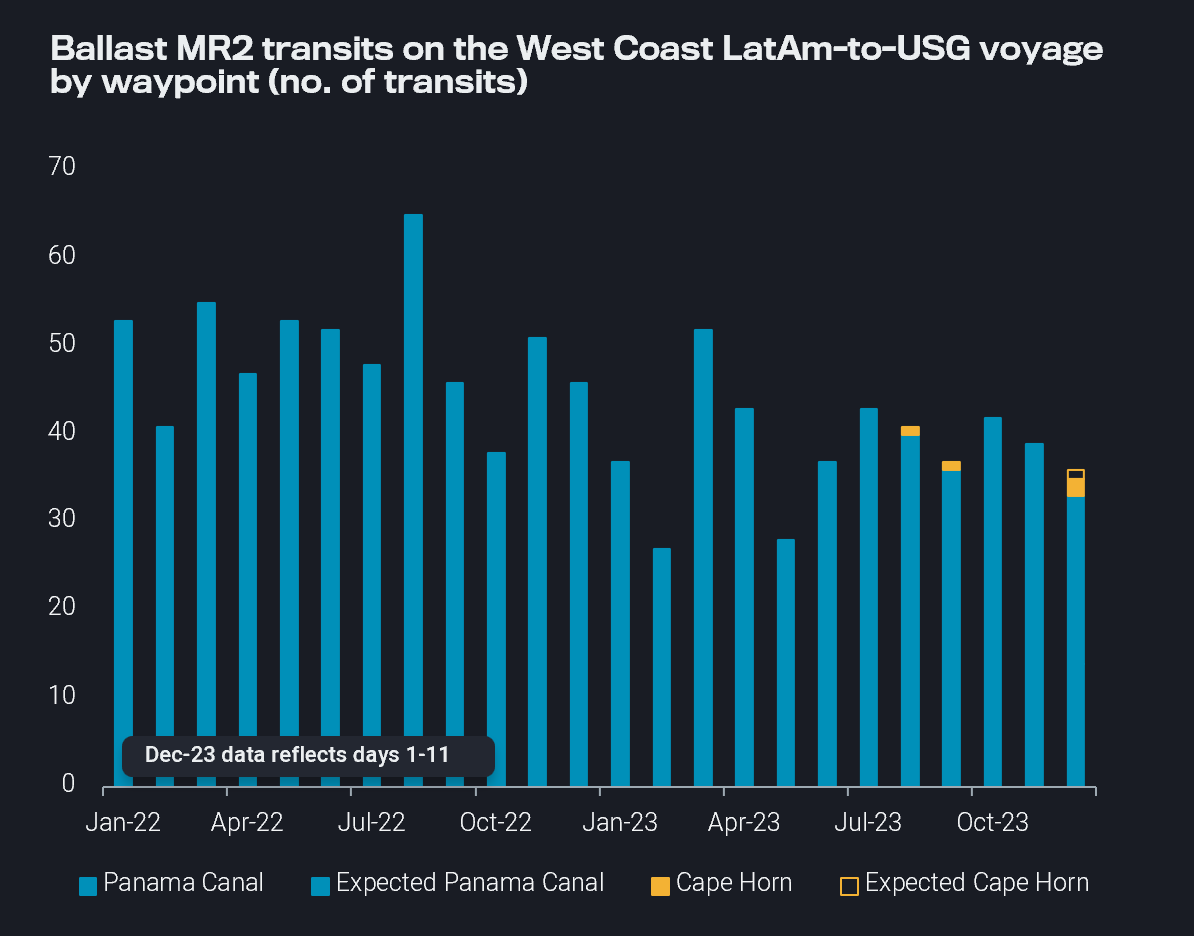

Additionally, once MRs reach the West Coast Americas, there are not many opportunities for further employment in the region. Ballasting across the Pacific is not a viable option, with Pacific Basin earnings currently about half of Atlantic Basin earnings (Baltic Exchange) as US Gulf freight rates climb. MRs are then faced with difficulties in transiting Northbound through the Panama Canal.

Again, we see an increase in voyages around Cape Horn, but this time for ballasters. We observed this behaviour with one MR in August and one in September last time congestion issues at the canal were very high. However, we have already observed two tankers transiting via Cape Horn so far in December (days 1-11) and are likely to see this behaviour persist as reduced canal transits remain.

Ballast MR2 transits on the West Coats LatAm-to-USG voyage by waypoint (no. of transits) (Retrieved via Freight API/SDK)

VLGC diversions increasing

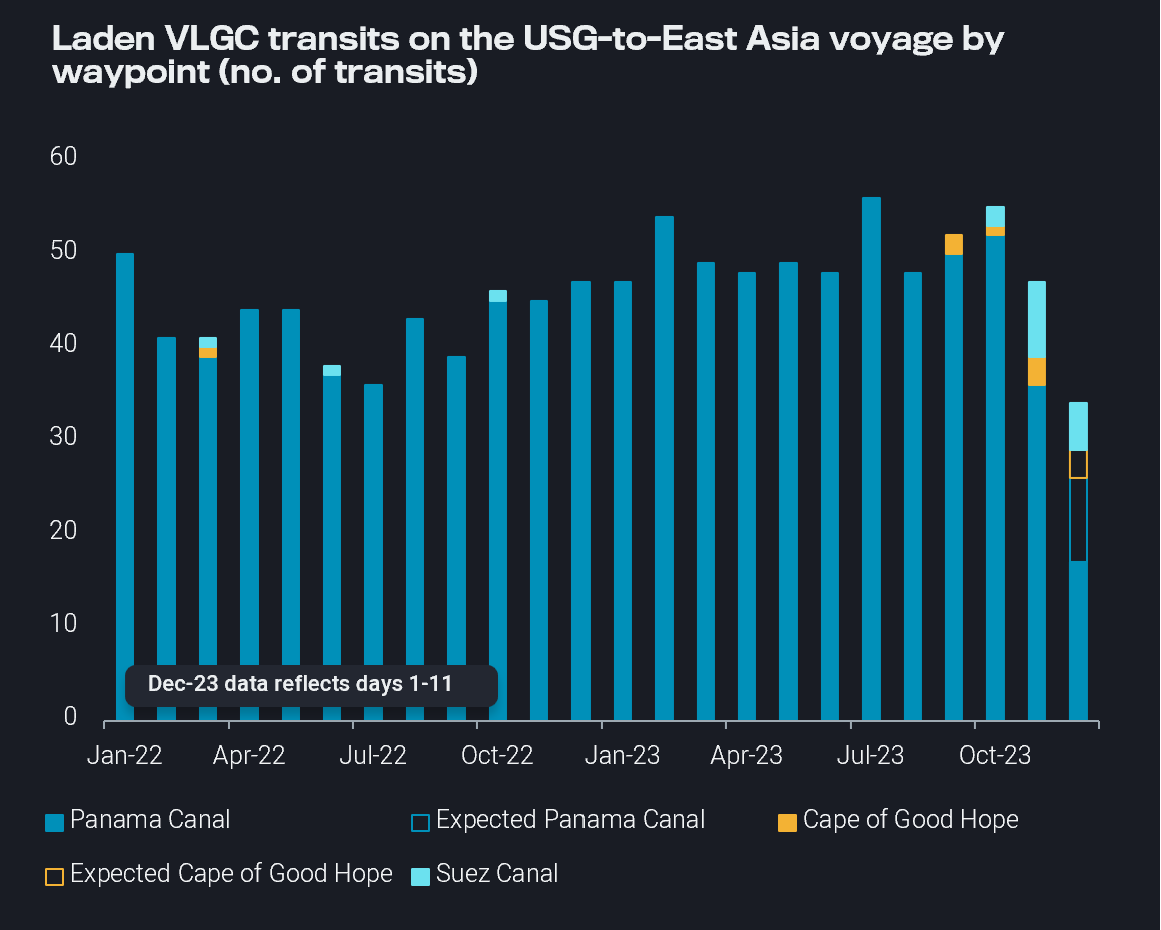

As VLGCs continue to be prioritised below passenger ships and container ships, securing transit slots has remained difficult, especially when transit slots will be further reduced in January and February. Starting in September, we observed some VLGCs diverting from the Panama Canal and transiting East via either the Suez Canal or Cape of Good Hope. These diversions have continued to increase, with more VLGCs utilising alternate waypoints in November and December.

Laden VLGC transits on the USG-to-East Asia voyage by waypoint (no. of transits) (Retrieved via Freight API/SDK)

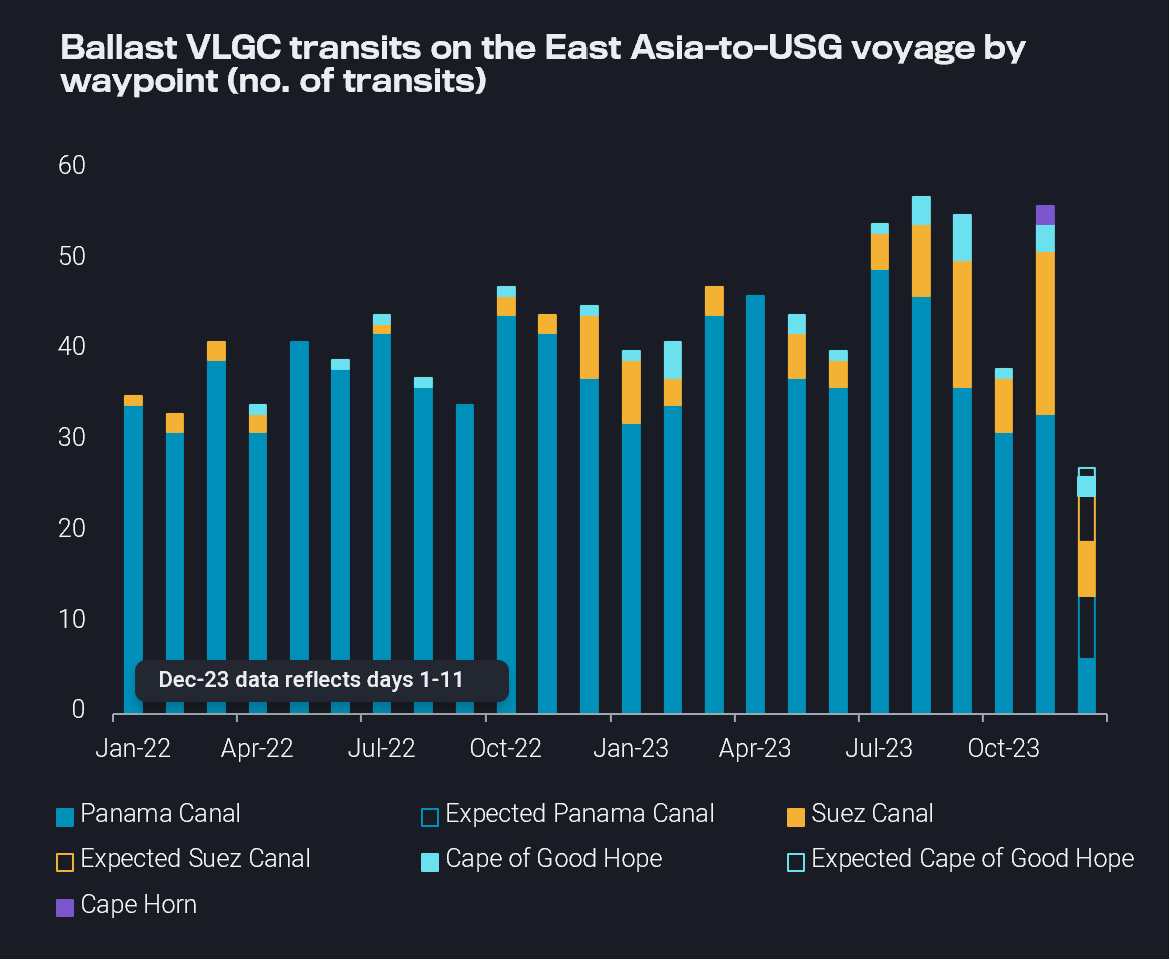

VLGC ballasters heading to the US Gulf are also avoiding the Panama Canal, and are increasingly utilising the Cape of Good Hope, the Suez Canal, and even Cape Horn. The effect of these longer VLGC voyages is increased tonne-miles and tighter vessel supply, which led to a surge in US Gulf-to-East Asia VLGC freight rates (BLPG3) that peaked in mid-November. However, higher freight costs – which eroded arbitrage economics – coupled with lukewarm import demand from East Asia due to warmer temperatures, weak petrochemical margins and ample domestic supplies have led to a softening of tanker rates in recent weeks.

VLGC transits on the East Asia-to-USG voyage by waypoint (no. of transits) (Retrieved via Freight API/SDK)