So if one goes up, so does the other? ?

One could easily argue no single commodity has ever had a greater influence on all aspects of one’s life than oil. Every change in the price of oil is greatly analysed, with one question in all minds being where does it go from here? Fluctuations in the price of oil lead to an infinite possibility in terms of ramifications, from the cost of energy to heat one’s home, to the cost of transportation to drive to work, to the cost of the chair one is sitting in reading this, and so much more. Behind every barrel of oil there’s most likely a tanker that carried this oil from its point of extraction to the refinery which would have processed it. So, it should be safe to say that, based on all of the above, if the price of oil goes up, so do tanker rates? As the price of oil goes up because more people want it (i.e. higher demand) so that means more people need ships to carry that oil (i.e. higher derived demand). Let’s assume supply remains constant for a minute and we have higher demand thus higher prices. It is, however, slightly more complex in reality.

Oil prices and tanker rates 101 ?

Before we dive into the effects of oil price fluctuations on tanker rates, it is important to understand there is an extra layer of complexity in our case. A fluctuation in the price of oil will have not one but two consequences for tankers. Firstly, it will impact the price of the cargo on-board, fairly straightforward but unique to tanker markets (as opposed to the dry bulk market for example). But it will also impact the cost of bunker fuel used to power the ship, which is a common trait across shipping markets, when the price of oil fluctuates.

What moves oil prices?

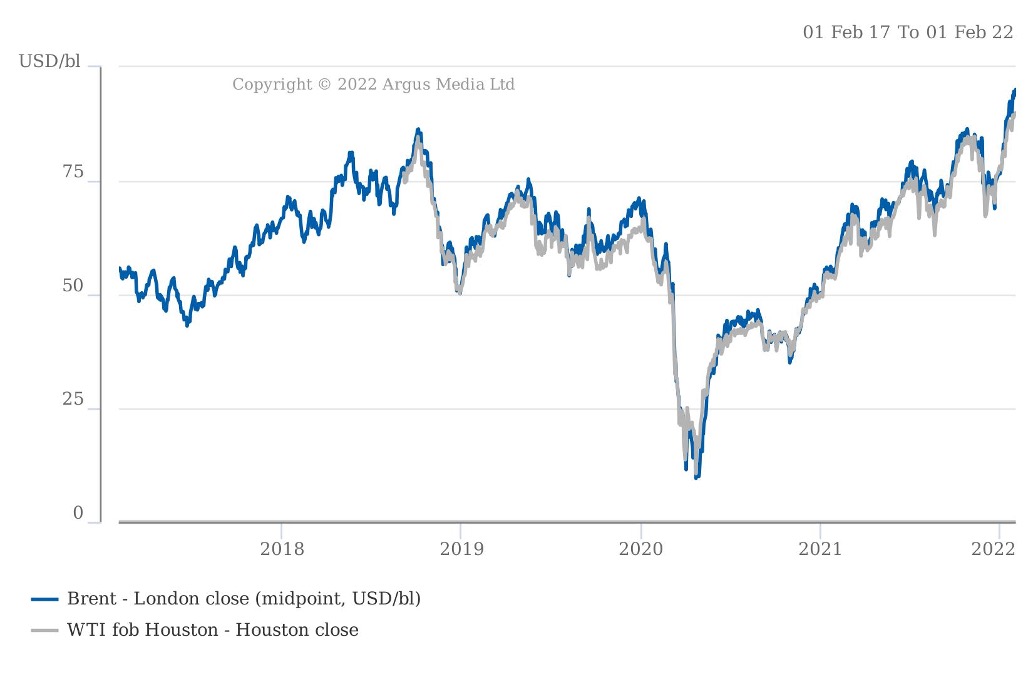

Oil prices in general, are a function of supply and demand. In the case of crude oil, supply pertains to barrels extracted from the ground, in large producing countries such as Saudi Arabia, or Russia. Both are members of the OPEC+ alliance, a group or 23 countries with a stated mission “coordinate and unify the petroleum policies of its member countries and ensure the stabilization of oil markets, in order to secure an efficient, economic and regular supply of petroleum to consumers, a steady income to producers, and a fair return on capital for those investing in the petroleum industry.” Slightly long winded, I’ll give you that, but the idea is one of coordinated increase or decrease in supply in line with market conditions at the time. Demand on the other hand, in the case of crude oil again, comes from refineries, which utilise crude oil as a feedstock, or raw material, to refine petroleum products more familiar to us such as jet fuel, gasoline or diesel. In that sense, crude oil is itself a derived demand!

Thus, the price of crude oil is dependent on the balance between supply and demand at any given time. On top of that, countries will have their own oil inventories, known as strategic reserves, whilst companies may have also built up stocks in case of significant disruption to their supply. The price of aforementioned refined products will also have an impact on the demand for crude oil and in turn lead most likely to a market impact on decisions or trades around the supply of oil.