Omicron obscures outlook for tanker markets

In this blog, Vortexa attempts to assess Omicron’s impact on crude and product tanker markets.

While autumn bid farewell to make room for winter, it made sure to make an impression at the end. The news of the Omicron variant breakout made the headlines and sparked – justifiably or not – fear around the globe, triggering a $12/b dip in oil prices. In this blog, Vortexa will attempt to assess Omicron’s impact on crude and product tanker markets.

Part I: Crude/dirty tanker markets

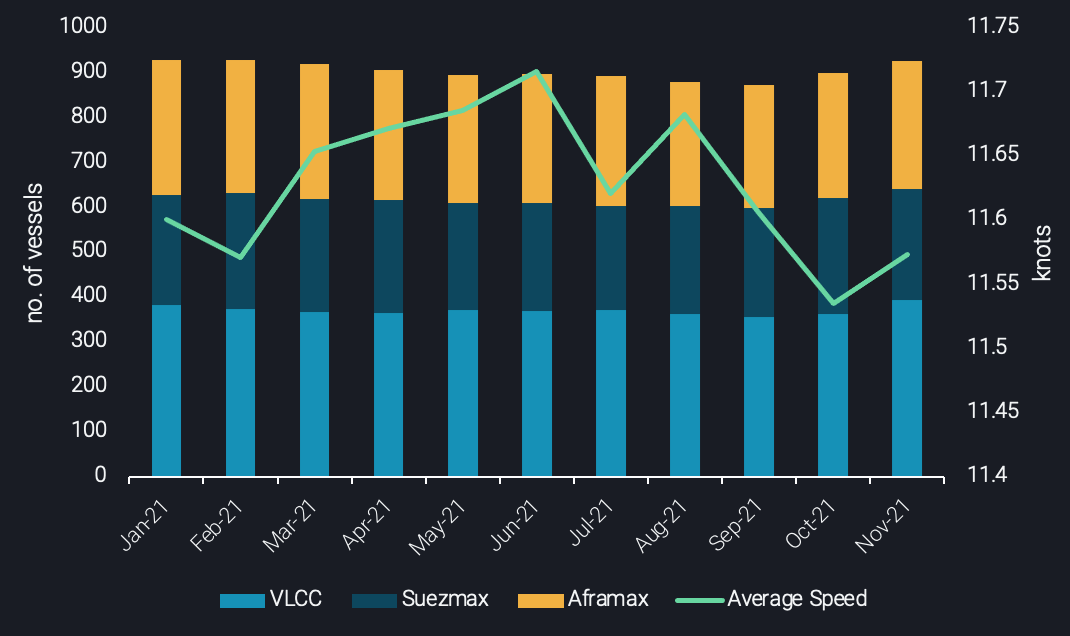

Utilisation of crude tankers vs. average speed

Looking at the chart above we can see improved crude tanker utilisation in Q4, led by rising OPEC+ and later also US exports. The bad news for owners is however that speed levels remained low as persistent oversupply has put a cap on rates across the board. The worse news is that rates remain low without taking the effect of Omicron into account, as we will aim to do below:

- Currently, refining margins are weak in energy-importing markets like Asia and Europe, while the new variant has put question marks over a prolonged rebound in oil demand. Thus refining operations and in extension crude procurement are set to slow, subsequently taking away cargoes from the crude tanker sector. In all likelihood, nomination for Saudi and other OPEC+ term crude will fall irrespective of the official production decision, as OSPs are now looking expensive.

- Zooming in on Asia, which recently showed its sweet crude appetite, margins currently look relatively lower on the year due to product oversupply in the region. This will likely translate into lower demand for sweet grades and in turn for long-haul voyages from the Atlantic basin, effectively reducing crude tanker tonne-miles, especially for larger vessel classes such as VLCCs.

- A potential silver lining for the crude tanker industry could be the fact that persistently lower crude pricing and a potential shift in market structure – we are not yet there – could incentivise buyers to replenish inventories following the recent drawdown. Such a development could provide support in trade demand, at a time where Omicron will possibly hamper final consumption.

Part II: Clean tanker markets

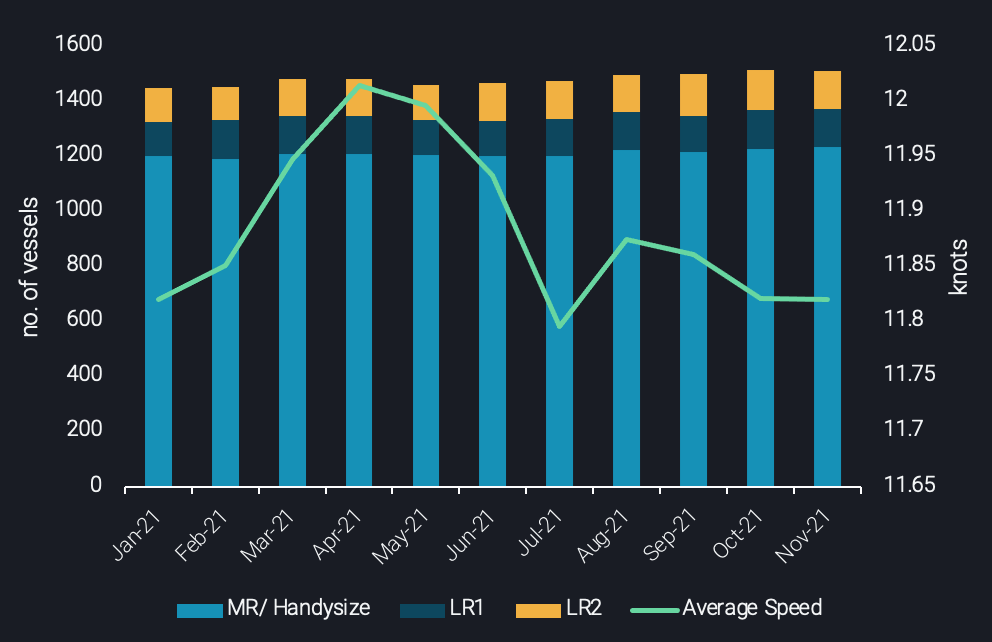

Utilisation of CPP tankers vs. average speed

A similar story is unfolding on the clean tanker market, with overall utilisation displaying an improvement as the year progresses. The difference however lies to the fact that a prospective impact of Omicron could not essentially result to the doom and gloom of the sector, depending on the vessel class and region of operation:

- MRs operating in the Atlantic basin could likely see both sides of the coin. On the one hand, diesel demand in Europe could remain resilient against the Omicron challenge. Heating and transportation services could even see an upside as more people stay at home, potentially counterbalancing lower mobility and supporting transatlantic diesel exports from the US, which also enjoys superior refinery margins.

- On the other hand, gasoline trade could see excess European cargoes finding homes in the US which for now seems less exposed to Omicron and all variants. But in Europe travel restrictions and social distancing are en vogue due to both Delta and Omicron. Refinery runs are set to decline, hampering tanker demand out of Europe.

- In a similar fashion, lower refinery runs could also limit LR tanker demand for eastbound European naphtha cargoes. Having said that, LRs will likely continue to be supported by sourcing cargoes out of the Middle East to satisfy strong Asian demand, however overall tonne-mile demand for LRs heading eastwards may decline.

- LRs heading westwards, predominantly carrying middle distillates, could also struggle to find employment for a combination of product supply and demand reasons. While demand repercussions of the new variant cannot be excluded for diesel, they are highly likely for jet fuel. Around 10% of LR tanker utilisation is currently attributed to jet fuel cargoes with the majority of them heading to European destinations. In Latin America, diesel demand is poised to decline seasonally as summer is approaching, bringing rain and lower agricultural and power demand. On the supply side, strong competition is coming from ample US and Russian barrels, which are carried by the smaller MR segments.

To conclude, the demand concerns related to Omicron and more regional supplies (US, Russia, less Atlantic Basin crude exports to Asia) are bad news for shipowners. Not only because it curbs oil trade and thus tanker demand, but lower oil prices could also play a role. Lower bunker prices coupled with a reduction in tanker demand (hence more suitors to take the cargoes available in the market), will provide charterers with greater negotiation powers when it comes to fix a vessel, potentially causing a drop in freight rates across the board. As a note of caution, though, Omicron and its actual repercussions on demand in the medium term are far from being understood at this point of time. We can only hope its impact is less than what we experienced with the Delta variant.

More from Vortexa Analysis

- Dec 1, 2021 Rising flows, wrong time?

- Dec 1, 2021 What a time(ing)!?

- Nov 25, 2021 Clean tankers battle it out in the Atlantic and the Middle East

- Nov 23, 2021 How helpful is the US-led SPR release

- Nov 23, 2021 Asia’s gasoline cracks make an unexpected U-turn

- Nov 18, 2021 Asia’s crude appetite sweetens in November

- Nov 16, 2021 Musings on OPEC+ spare capacity

- Nov 11, 2021 Tonne-miles need to pick up to sustain rally in dirty freight rates

- Nov 10, 2021 Does supply provide a cure for record LPG prices?

- Nov 10, 2021 Global diesel market braces for tight winter as inventories draw

- Nov 4, 2021 What’s behind Asia’s gasoline crack surge?