Prolonged Russian export ban triggers downside risks for Atlantic MR rates

As Russia reportedly attempts to implement control on its own volumes by cutting diesel and gasoline exports, up to 90 MRs could scramble for employment in the mainstream routes, although early indications on Russian diesel and gasoline exports post-ban announcement reveal that this number will be lower. The sanctions framework could provide additional optionality for certain operators while others might exploit opportunities arising in the East of Suez or in intra-Americas trades depending on chartering policies. At the same time, the lack of Russian volumes underpins product supply woes, while refinery maintenance season is underway in key regions and is likely to hamper MR tanker demand.

West of Suez MR freight rates have remained at healthy and relatively stable levels for owners following a volatile period post Russian invasion. The support on rates has been characterised by robust transatlantic CPP flows over the summer on the demand side. From a supply perspective, a reversal in MR migration with more tankers heading East and persistent Panama Canal congestion issues have alleviated MR tonnage. However, the fresh export ban on Russian diesel might provide another twist to the tale for MRs operating in the Western hemisphere.

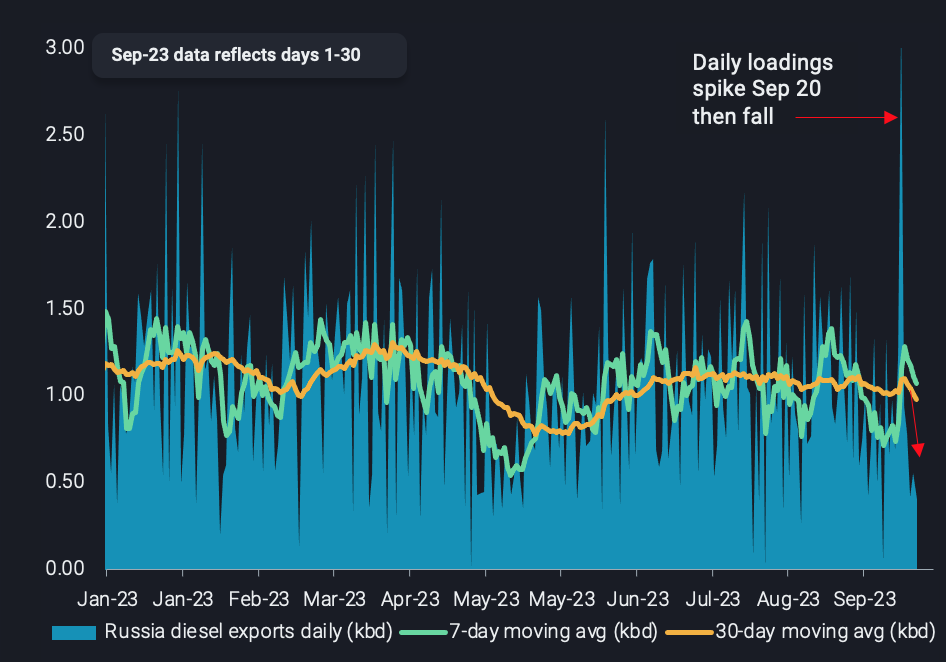

Daily Russian diesel exports (mbd)

MRs previously operating in Russia are already searching for fresh opportunities, as diesel exports have fallen about 40% last week vs year-to-date averages. Unsurprisingly, the number of MRs waiting offshore ports in the aforementioned regions is declining – although not close to zero – as they attempt to seek employment elsewhere. Similarly, MRs that have discharged Russian cargo recently show no concrete indications of their next loading port. In essence, these tankers are signalling waypoints (Gibraltar/Las Palmas, Rotterdam, West Africa) that could give them greater optionality in finding their next cargo.

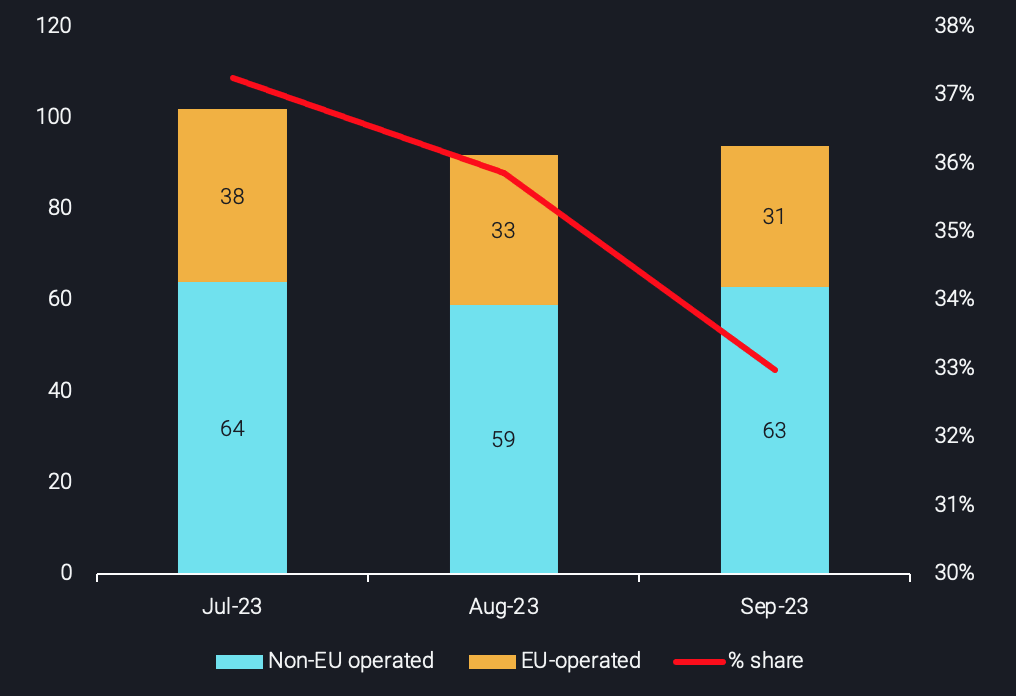

Subsequently these tankers will compete for cargoes on the mainstream trade (i.e. excluding Russian trades). One key aspect to note is that MRs operating out of the price cap will not be able to visit EU ports. If an assumption is taken that all EU-operated vessels have not been involved in any sanctioned-breaking activity then around a third of MRs carrying diesel on a monthly basis (more than 30 vessels) could be legally eligible to compete in routes involving Europe.

No. of unique MRs that loaded Russian diesel over the last 3 months split by operator nationality (no. of vessels, LHS) vs % share of EU operators (RHS)

Although the regulatory background will limit the competition for MR tankers operating in Europe, overall, the lack of Russian barrels will certainly lift the MR tonnage available for the global mainstream trade, presenting a downward risk to freight rates.

From a tanker demand scope, if the lack of 1mbd (currently is a lack of 400 kbd) of Russian diesel from the market materialises – for as long as it stands – also presents new realities. On the one hand, this development will trigger higher diesel flows out of the US Gulf to satisfy demand for places such as Latin America. Nevertheless, with the US currently catering for its own domestic demand as well, diesel flows to Europe seem rather unlikely. Hence, as winter progresses, Europe might further increase its needs for Middle Eastern or Indian diesel volumes, which are traditionally carried on LR tankers, limiting the freight upside for MRs.

Finally, an additional limiting factor for MR tanker demand could originate from traditional diesel exporters which were relying on Russian volumes. Turkey, for instance, is a country which ramped up Russian diesel imports for domestic use and in tandem increased its own diesel exports. The lack of Russian inflows could lead to a decline of exports, resulting in “double damage” for MR employment, especially in the Mediterranean.