Russian reshuffling and rising transatlantic demand to support MR tankers in Q2

MR freight rates have shown stability in March after seeing large swings earlier this year. In this insight, our freight team examines how reshuffling due to changes in Russian CPP trade and recent increases in MR demand in the Atlantic basin have contributed.

Clean MR freight rates have stabilised in March after starting 2023 with a large decline amid cooling CPP demand after a busy Q4 of 2022, as well as seeing high levels of market volatility with recessionary fears looming and reshuffling of trade ahead of the EU’s ban on Russian oil products in early February. In the MR segment, this has been brought on by a mix of demand strength and weakness in various regions, as well as a pick up in global MR tightness, with more tankers moving to the Russian trade.

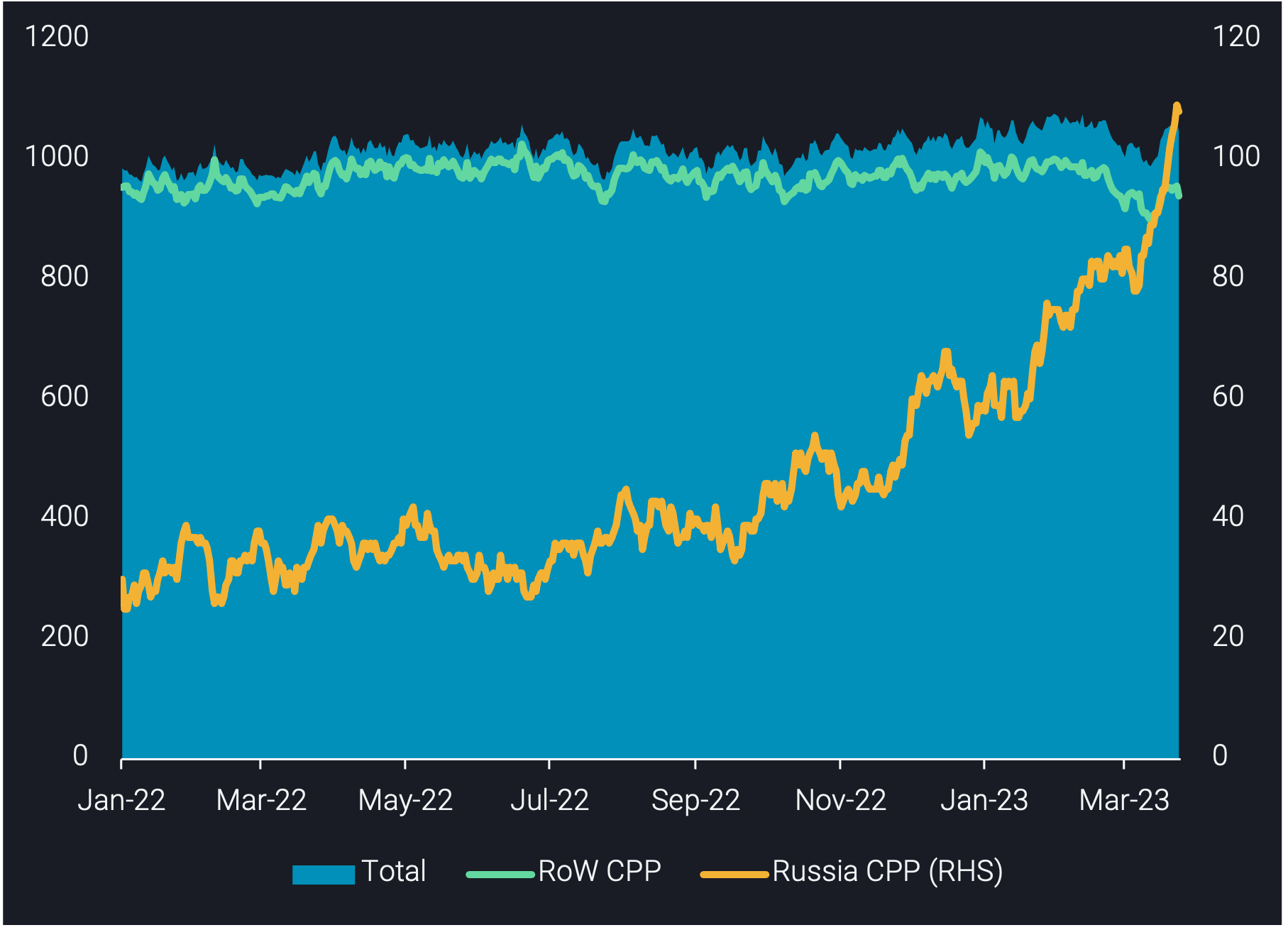

MR utilisation in the rest of the world vs in Russian CPP trade (RHS, no. of vessels)

Mixed fundamentals stabilise MR demand, for now

In the mainstream market (excl. Russian trade), MR tankers have seen increased utilisation out of Europe to the US Atlantic Coast as PADD 1 gasoline stocks have continued to decline, reaching the minimum of the 5-year range. This has supported MR freight rates out of Europe in general, despite less MR tanker demand out of Europe towards other regions. In the US Gulf, freight rates have struggled to gain momentum, with limited tanker demand due to refinery maintenance in February and March. With the maintenance season coming to a close, refinery utilisation has increased in PADD 3, which has seen increased CPP exports in March. A related increase in tonne-mile demand has been hampered by strong flows to short-haul destinations in Central America, keeping tanker availability in the region elevated and suppressing rates. Over in the Pacific basin, MR rates have also been suppressed by high levels of MR availability in the region and flat tanker demand.

How has Russian CPP changed the MR market?

In the Russian CPP trade, a much clearer trend is shown in tanker demand, specifically in the MR segment. MR utilisation for Russian CPP has risen steadily since the last quarter of 2022, and over 80% this year alone. These cargoes are mostly diesel headed to destinations further afield as compared to Europe, including West Africa, South America and Southeast Asia.

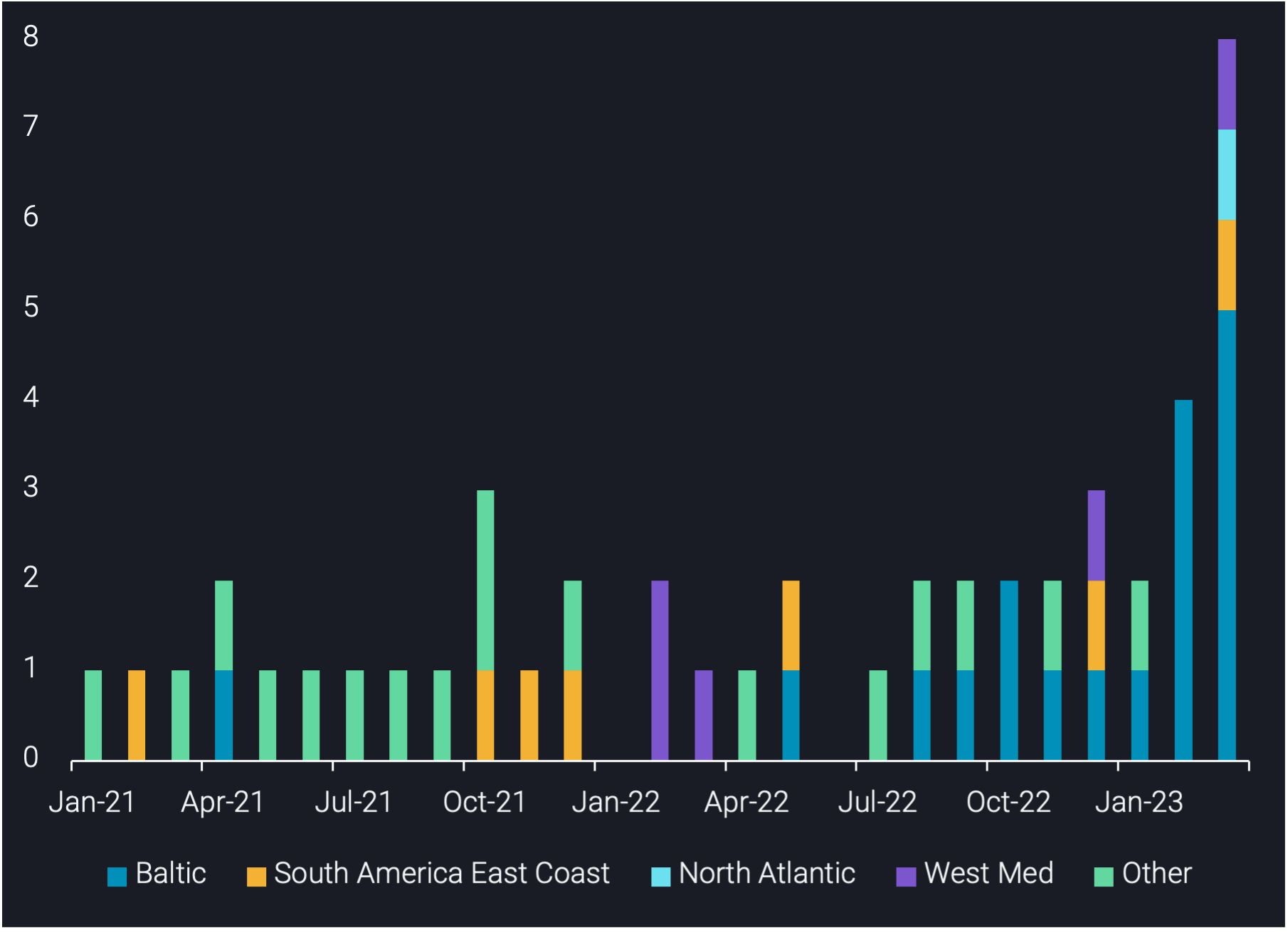

Ballast voyages post discharging Russian CPP in Brazil per destination (no. of voyages)

Not only are voyages much longer, but vessel behaviour has also changed, keeping vessels from operating in other CPP markets. For example, vessels discharging in Brazil have increasingly been heading back towards the Baltic, as shown by data from our Freight API/SDK. This voyage is inefficient from a shipowner’s perspective, given the substantial ballast leg, which indicates that – while there is no formal freight assessment for this route – the financial incentive for owners is likely to be significant. A similar pattern has emerged for Russian CPP headed to West Africa, where tankers have exhibited the same behaviour.

With fleet growth in the tanker market staying limited for at least the next two years on the back of a low orderbook, Russian CPP trade has increased vessel requirements in the MR segment and hence exacerbated tightness in the global MR market. On the demand side, MRs could find further support in the summer driving season and the return of PADD 3 exports. These drivers could see the MR market break away from the current stability in rates towards the upside.