Shipping is navigating through uncharted and uncertain territories

Having one eye set to analytical insights and the other on industry events, Vortexa provides a brief outlook on the shipping industry’s future.

Having one eye set to analytical insights and the other on industry events, Vortexa provides a brief outlook on the shipping industry’s future. It seems that the tanker sector will need to surf high and wild waves, both in the short and the long term.

Decarbonisation drive lacks clear guidance

After almost two years of virtual panels and conferences, London International Shipping Week 2021 (LISW21) gathered stakeholders in person from all around the sector: charterers, shipowners, brokers, classification societies, IMO delegates and lawyers to name a few. Even though the current demise of tankers was mentioned along with the upbeat environment in the dry bulk and containership segments, there was a single topic that took the spotlight: the path towards decarbonisation.

Below is a summary of the main takeaways:

- A catch-22 situation has been created where a shipowner will not commit to building a vessel if the infrastructure is not in place. Meanwhile, the fuel/energy provider will not develop said infrastructure if the respective fuel-burning technology is not fitted on ships. Doubts on the viability of green technologies, all currently at a nascent stage, are keeping investments thin across potential suitors, while the number of different stakeholders involved in the shipping decarbonisation process adds to the complexity and decelerates any significant movement.

- Thus, the need for cross-collaboration was touted to develop the appropriate technologies to ride this wave of decarbonisation. This seems quite reasonable as the effort encompasses the whole supply chain: from the producer to the end-user. Data-sharing activities and an uptake of pilot projects between industry stakeholders is required to research and expedite the development of technological advancements and their feasibility. However, the opaque environment of the shipping industry and the reluctance in data-sharing especially when it comes to fuel consumption and carbon emissions could prove to be a hurdle in this endeavour.

- Shipping is a capital-intensive activity with the economic life of a ship lasting around 25 -30 years. Investing heavily in a technology that has not been commercially deployed and burning a fuel for which the bunkering infrastructure is not in place, is a big ask.

- The industry has a real challenge to implement measures beyond the larger players. Around 70,000 smaller ship owners exist in the market, with many lacking the resources to implement digital/technical infrastructure for tracking emissions and monitoring real-time vessel performance. Creditors/financiers can be also more reluctant to provide the capital required for a significant investment, which ultimately could lead to an industry consolidation with fewer participants and possibly fewer ships as a portion of the technological obsolete vessels will head to the scrapyards. Even for bigger owners, banks and other financing sources could be reluctant in investing in a ship without a guarantee of return. This guarantee could come in the form of a time-charter attached to the newly-built ship. Such a development could have significant repercussions on the market structure of tramp shipping (dry bulk and tankers), where long-term contracts could prevail over spot charters.

In summary, the issues that the industry is facing towards the decarbonisation drive were well-addressed throughout LISW21 and a consensus was reached that the industry needs to act immediately. Despite acknowledging the problems, there was a struggle to provide an appropriate and coherent guidance to solve the matter at hand, and it seems that the shipping industry (tankers, dry bulk carriers, containers) will be sailing through uncharted territories for the years to come.

Hopes for tanker market recovery remain dim

It is not only the long-term future that is looking uncertain, however, especially when focusing on the tanker industry. Crude freight rates remain currently depressed and there are a variety of factors that speak against a marked recovery, at least in the remainder of the year.

- Global crude loadings remain at low levels or are even declining. The only significant exceptions are UAE and Saudi Arabia exports, which have ticked up higher during the summer. After excluding these two crucial OPEC members, we see OPEC+ exports around 7mn b/d below early 2018 levels, with West Africa spearheading this decline.

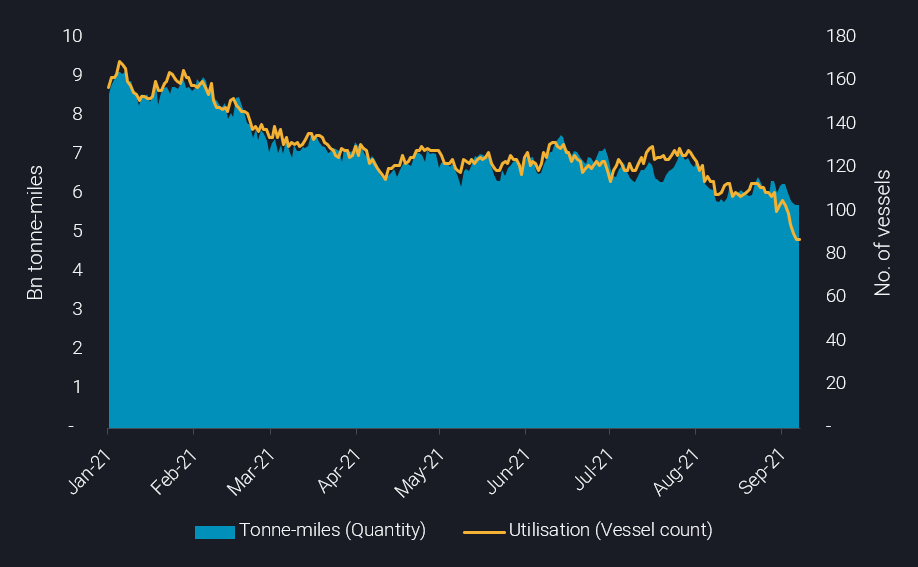

- Similarly, oil demand is failing to recover decisively on a combination of protracted Covid repercussions, inflationary pressures and first effects from decarbonisation efforts. China in particular has changed its guidance for the oil industry drastically, cutting crude imports to an extent, where together with less long-haul imports from the Atlantic Basin VLCC utilisation to China was halved throughout the year.

- Finally, shadow voyages from Iran and Venezuela which induce a low risk-high reward situation to old VLCC tonnage, has dampened demolition activity. Even though scrap prices have reached 10-year highs, only five VLCCs have headed towards the scrapyard so far in 2021 and nine from 2019 onwards. This number is dwarfed when looking at the 32 that were scrapped in 2018 and it provides no alleviation to an oversupplied market. As long as these illicit trading opportunities are lurking, it is highly likely that owners will refrain from scrapping.

VLCC tonne-miles and utilisation (RHS) towards China

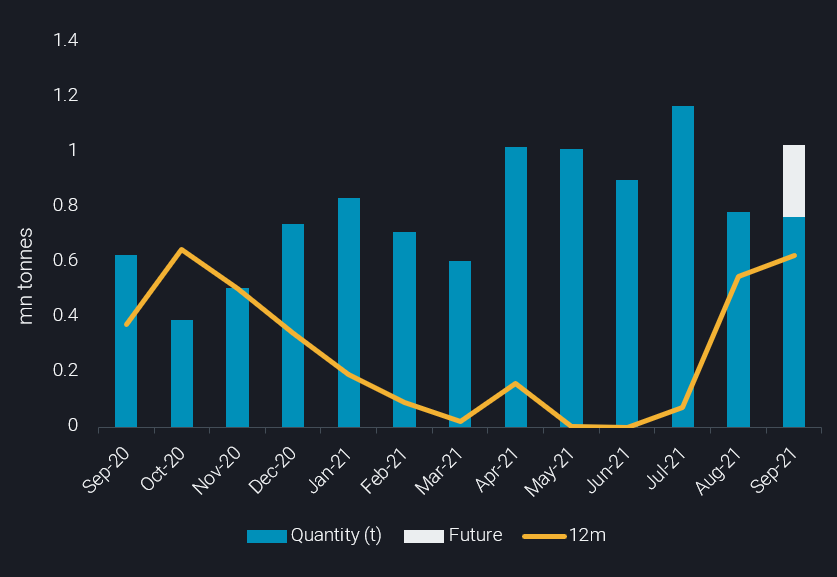

On the clean market, a slight improvement was in the Pacific observed towards the end of the summer. Rising diesel exports from Asia amid lower domestic consumption was met with rising import demand from Europe and the Americas. This development in turn, boosted East to West of Suez tanker movements, which essentially brought tonne-miles ex-East of Suez at an annual high. Yet, this support in rates will likely be short-spelled :

- Diesel consumption in Latin America is expected to decline as the agricultural season is coming to an end. Additionally, the refineries that are coming back online in Europe from maintenance schedules will satisfy regional demand, thus reducing East to West of Suez movements and effectively slashing tonne-mile demand.

- The demise of the crude tanker markets reinforces the trend seen in the past few years for newbuild VLCCs to increasingly carry clean cargoes on maiden voyages. This in turn cannibalises the MR and LR2 tanker segments, which otherwise would have carried these clean cargoes. At the same time, an increasing number of Aframax/LR2s are “cleaning” up to compete on the CPP market owing to economic prospects. This development exerts pressure on the clean tanker supply side, capping any prospective recovery on rates.

For a more thorough and insightful analysis on the current and future state of the tanker market, tune in to our freight webinar by clicking here.

More from Vortexa Analysis

- Sep 20, 2021 Flow highlights: Tight supply continues to support prices across the board

- Sep 16, 2021 LatAm road fuel imports set for decline after hitting record

- Sep 15, 2021 Can Asian gasoline sustain their strength in Q4 2021?

- Sep 15, 2021 Reality check: is China ready for U-turn after weakness in last months?

- Sep 9, 2021 The Atlantic Basin pulls diesel into the spotlight

- Sep 8, 2021 Collapse in West African supplies hits dirty freight segment hard

- Sep 7, 2021 Physical flow highlights: Supply-side restrictions boost prices across the board in spite of poor demand

- Sep 2, 2021 VLCC Clean Maiden Voyages: a trend coming to an end?

- Aug 31, 2021 Physical reality check: How strongly are Asian oil flows affected by COVID-19 waves?

- Aug 26, 2021 Summer of 2021 brings LNG players heatwaves, empty dams and a longing for Nord Stream 2