Tanker diversions rise with Red Sea tensions, but most oil & gas shippers still transit the Red Sea

As attacks in the Red Sea persist, only freight rates for key flows via the region have surged. Tanker diversions have picked up but not en-masse, as volumes continue to flow via the Red Sea.

As attacks in the Red Sea persist, freight rates for key flows via the region have surged but remain unaffected on a global scale. Tanker diversions have picked up in the span of the last two weeks, but these are not occurring en-masse as tankers and volumes continue to flow via the Red Sea. Instead, these diversions are at large constrained to US/EU/Israel-linked entities and also the companies that announced the decision to divert via the Cape of Good Hope.

Tensions in the Red Sea are mounting at the start of 2024 as attacks from the Houthi rebels continue to occur. Several companies in the shipping world – at least 18 given recent comments from the IMO – have decided to steer clear from the Red Sea, with containerships feeling the greatest impact with freight rates tripling over the last month to hit 12-month highs.

At the onset of the attacks on non-Israeli related vessels passing through the Bab el–Mandeb, Vortexa published a report studying the possible repercussions of the disruptions on the world of energy flows and freight. Fast-forward two weeks later, and we have a look at the extent of flows actually changing so far.

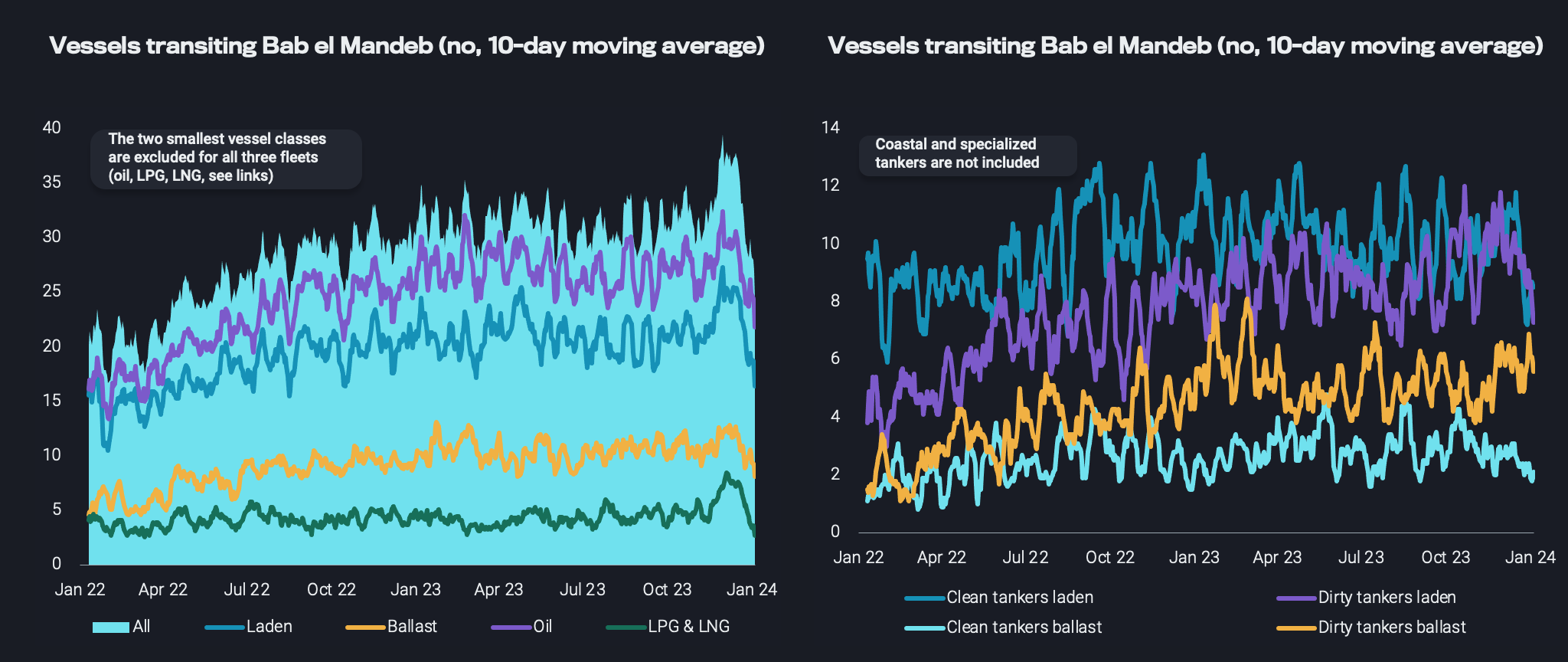

Starting with a look at the number of transits, we note that over the last 10 days transit numbers are about 15% lower than on average in 2023. The decline is more pronounced for LNG and LPG tankers, which had also seen particularly high transit figures in the months before Houthi attacks intensified based on Panama Canal limitations. But overall the majority of vessels are still passing through the Red Sea.

Bab el Mandeb transit for large oil & gas carriers (no of vessels, 10-day moving average)

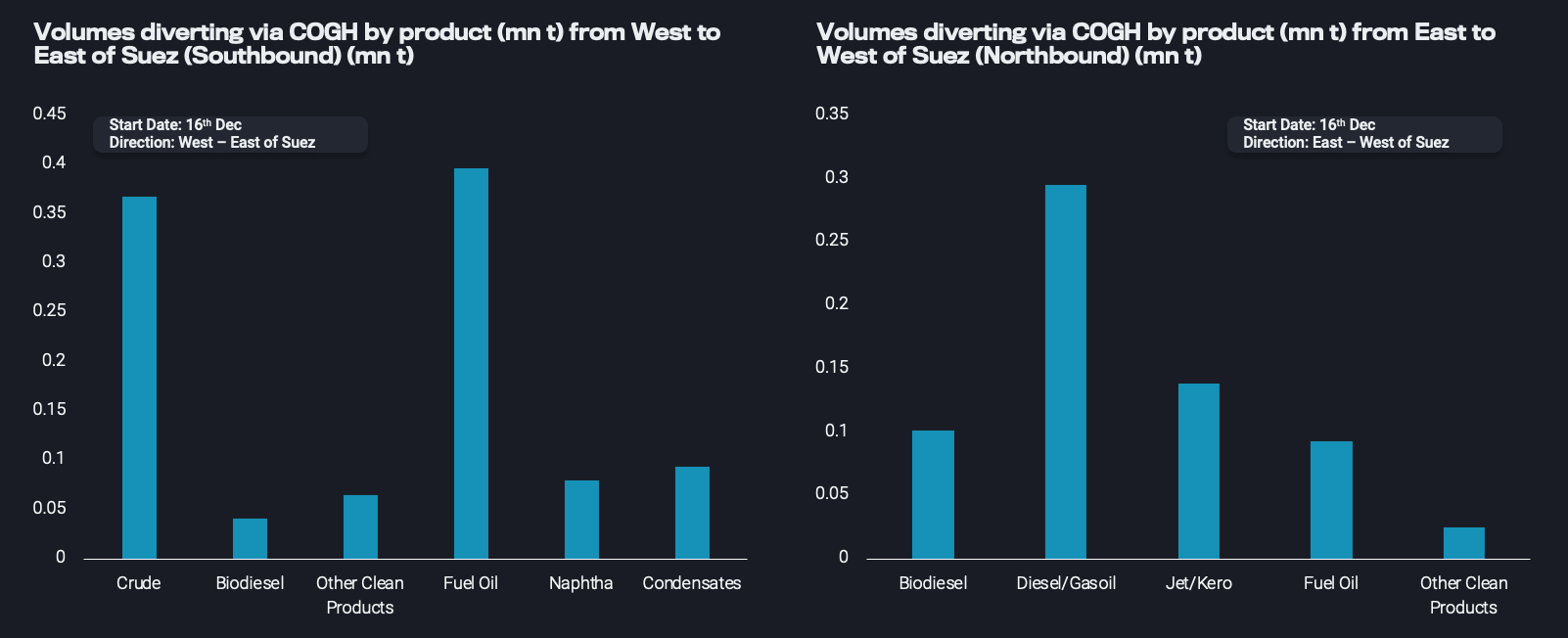

Since H2 December 2023, 19 vessels have diverted or transited via the Cape of Good Hope going Southbound (West to East), instead of heading via the Suez Canal carrying a combined 290kt of CPP and 860kt of Crude/DPP. Similarly, 13 vessels have diverted via the Cape of Good Hope going Northbound (East to West) instead of heading via the Bab-el Mandeb strait carrying around 560kt of CPP and 90kt of Crude/DPP.

Volumes diverting via COGH vs their respective volumes carried by product for Southbound and Northbound transits (mn tonnes)

Tanker freight rates for routes involving transit via the Red Sea have surged on a m-o-m basis. The increase on CPP freight routes (TC8 and TC20, 60% m-o-m) versus their crude tanker counterparts (TD23, 25% m-o-m) underpins the importance of the disruptions to the middle distillates flows from East of Suez to Europe and the difficulty to replace these.

Although freight rates for the impacted routes have picked up, this has not been reflected in the overall tanker market, implying that there is not en masse re-routing taking place at the moment. Additional War Risk Premiums in the Red Sea have been partially contributing to the freight rate hikes for the relevant routes, but this surcharge is significantly lower than the costs linked to re-routing via the Cape of Good Hope. Because of the current pricing dynamics, the tankers that are diverting are predominantly the ones chartered from companies announcing diversions as well as the ones operated from US and Israel-linked entities.

Reportedly some traders are attempting to avoid transiting via the Cape of Good Hope due to increased costs, yet other Western-based operators are also reluctant to transit the Red Sea. For now in these cases, every fixture is treated differently, based on mutual agreements between the operator and the charterer.