Tanker fleet profile for Russian oil after sanctions

The tanker fleet engaged in the Russian trade post-sanctions is predominantly Greek-operated and composed mostly of older Aframax and MR tankers.

Russian crude and product flows have undergone a huge reshuffling as previously traditional markets have all but shut out Russian exports. As new routes and flows open up and become more established, we can begin to explore the profiles of the tankers involved in these trades.

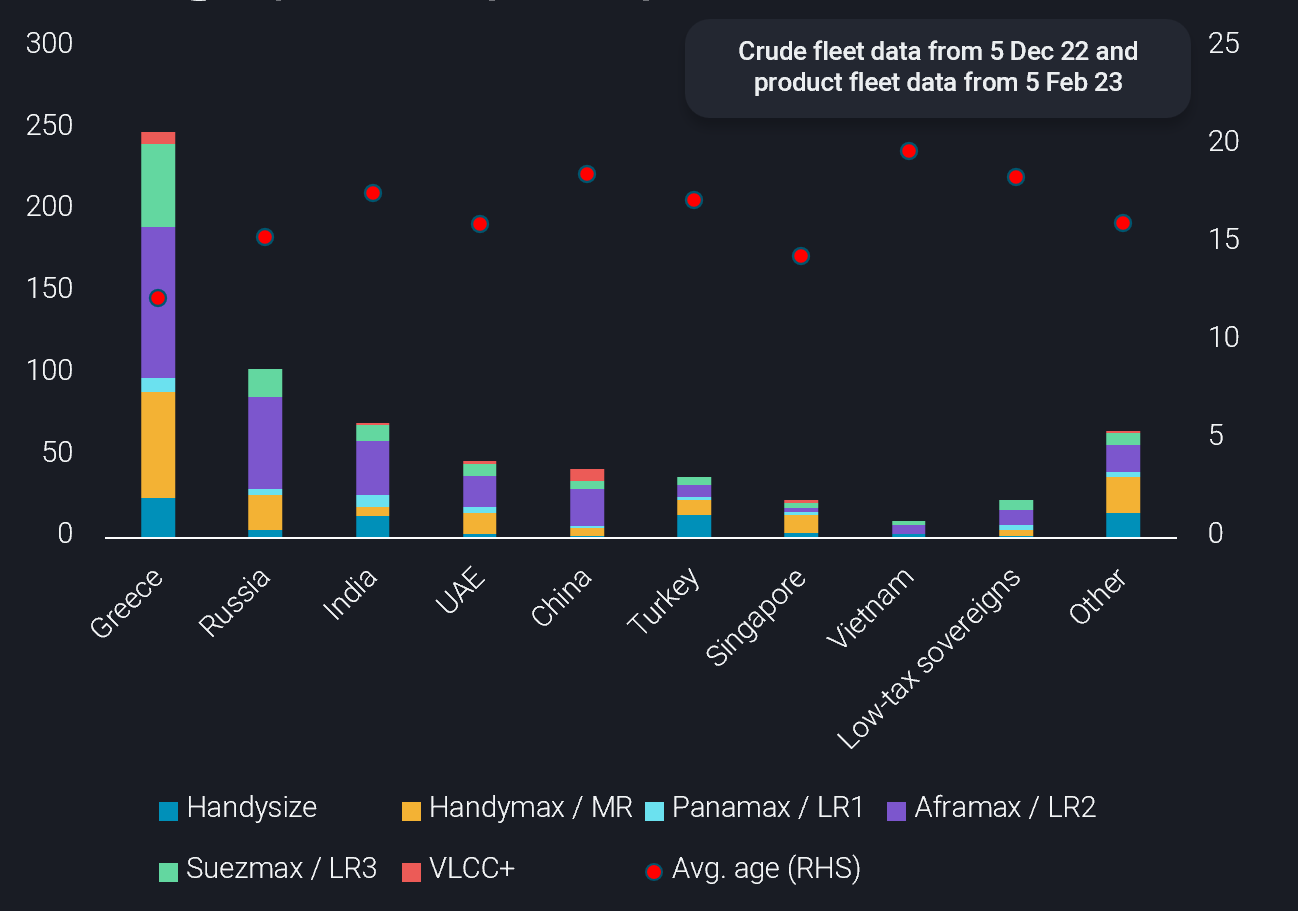

Greek tanker operators lead Russian oil trade

Russian trade after EU insurance ban by operator nationalities per vessel class (no. of vessels, LHS) vs. average vessel age by nationality (RHS, years)

Russian oil trade post-ban is dominated by Greek tanker operators, and the size of the Greek-operated fleet post-EU ban is nearly 2.5 times bigger than the next fleet, i.e. Russia’s. Russian-operated vessels make up the second highest share due to a large crude tanker fleet which existed pre-war.

It is important to emphasise that it is not illegal for EU operators to be part of the Russian trade post-insurance ban, provided the correct insurance documentation exists to show use of the price cap mechanism if a vessel uses EU/UK insurance and services. For example, after the shipping insurance bans, almost all the Greek-operated vessels still have coverage under the International Group of P&I clubs – which is the group of protection and indemnity clubs that provide insurance for almost all of the world’s shipping. This could give us an indication that the price cap mechanism is being used.

Greek operators’ involvement in both Russian crude and product trade is not a new phenomenon, but has fallen. In all of 2022 leading up to the 5 December ban, the average share of Russian Baltic and Black Sea crude exports carried by Greek operators was around 40% of total volumes. Following the ban and through Q1 2023, the Greek share fell to 33%.

This drop is partially because some of the Greek share has been displaced by new operators from countries such as India and the UAE. These new operator entities acquired fleets to serve new trade patterns such as the reshuffling of Russian crude flows to the East. Consequently, Indian-controlled vessels are the third largest in the Russian trade and UAE-controlled are the fourth largest.

Aframax tankers make up the highest share for each of the top five operator nationalities, as they are the biggest crude tanker class that can be fully-laden from Baltic ports.The increasing demand on the Aframax fleet can be seen in Aframax tonne-miles and laden utilisation from Russian ports, which have continued to trend upwards since April of last year.

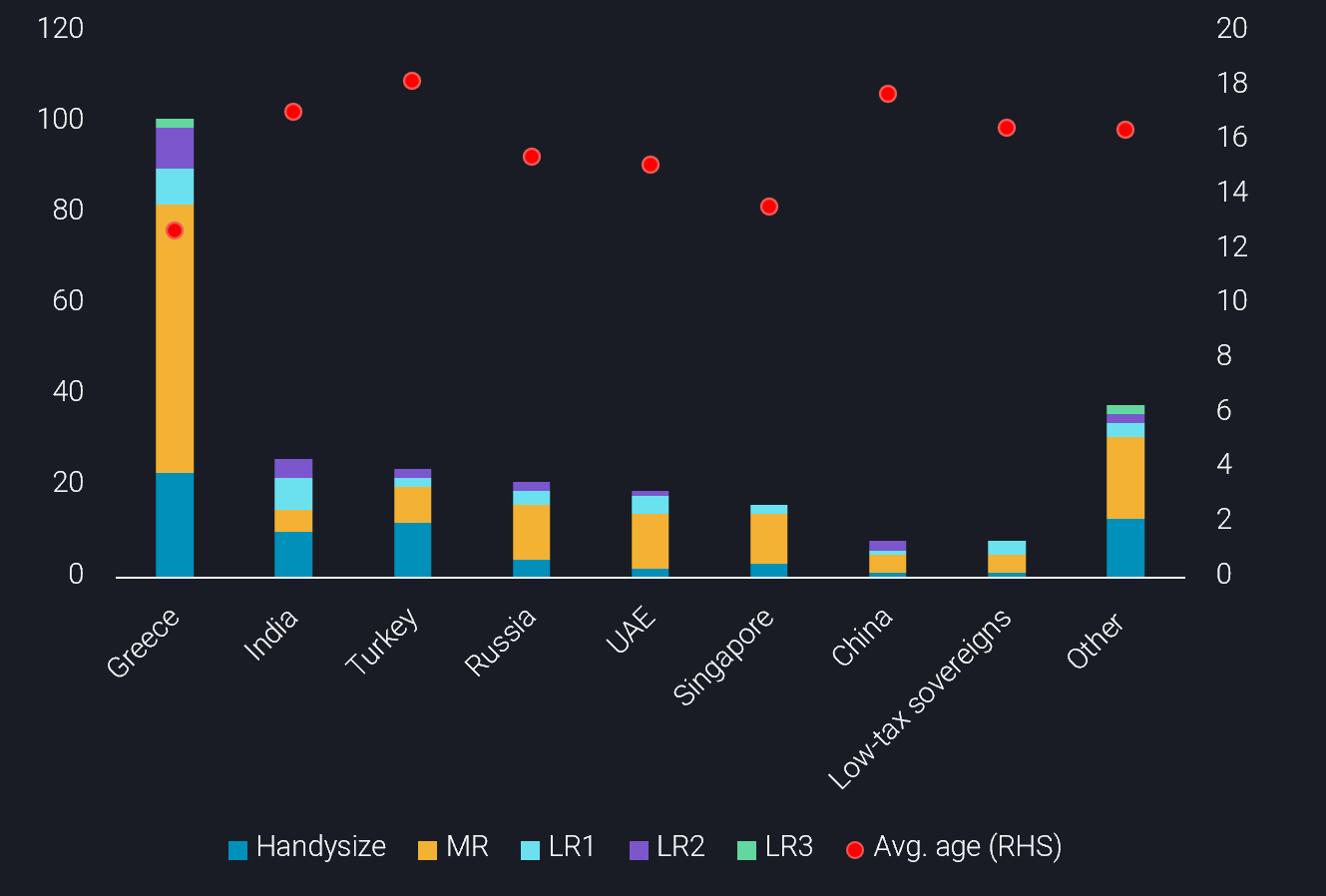

Greek operators even more crucial for Russian CPP

Russian CPP trade after 5 Feb by operator nationalities per vessel class (no. of vessels, LHS) vs. average vessel age by nationality (RHS, years)

Analysing solely the clean tanker fleet reveals a few differences from the wider tanker fleet profile. Since the 5 Feb products EU/G7 ban, Greek operators have the largest share of the fleet engaging in the Russian CPP trade, but by a much wider margin than when analysing the total tanker fleet. The Greek-operated fleet moving Russian CPP is about 4 times larger than the next-largest fleet. The main difference here from crude is the lack of clean product tankers controlled by Russian operators.

Almost 60% of this Greek fleet are MR tankers, traditionally used for short-haul destinations such as the Mediterranean, which is where most voyages end. Unusually, some of these MRs are travelling as far as South America, illustrating the significant reshuffling occurring, especially for a vessel segment which usually does shorter-range journeys.

As in the crude side, Indian operators have already built up a substantial product fleet. The CPP fleet controlled by Indian operator-entities, has the largest ratio of LR tankers to total fleet, which could indicate a propensity to carry products to destinations further afield. We have already seen a few voyages by these operators from Russia to destinations in Southeast Asia, West Africa, and South America.

Another major difference compared to the overall post-ban trade is the higher involvement of Turkish clean tanker operators, which is mainly driven by the diesel trade. Russian diesel exports have increased over 32% m-o-m in March, with most of the volume heading to the Mediterranean and imports to Turkey by around 113kbd, an almost 46% increase. Interestingly, the Turkish fleet has the oldest average age at around 18 years old.

Looking ahead

Based on Vortexa data, the post-sanction tanker fleet carrying Russian oil demonstrates a predominance of Greek operators, the usage of smaller vessel classes such as MR and Aframax, as well as the employment of older tankers.

Recent purchases of vintage product tankers could indicate some of the India and UAE-based operator companies formed after the Russian war are continuing to build their fleets, according to market sources. Meanwhile the fleet for Russian crude trade looks to have solidified, as we have not seen many new players entering in recent weeks. Sale and purchases of old crude tankers have fallen in recent months, signalling that operating companies formed post-invasion have slowed in building their fleets.