Transatlantic flows are the shining light for MRs, but will it eclipse?

After hovering around 1-year lows for the 1st half of May, MR freight rates for transatlantic flows (TC2 and TC14) rallied during the 2nd half of the month and thus are currently up by around 25% and 20% on a m-o-m basis. This increase was a function of both recent development in freight demand and supply fundamentals.

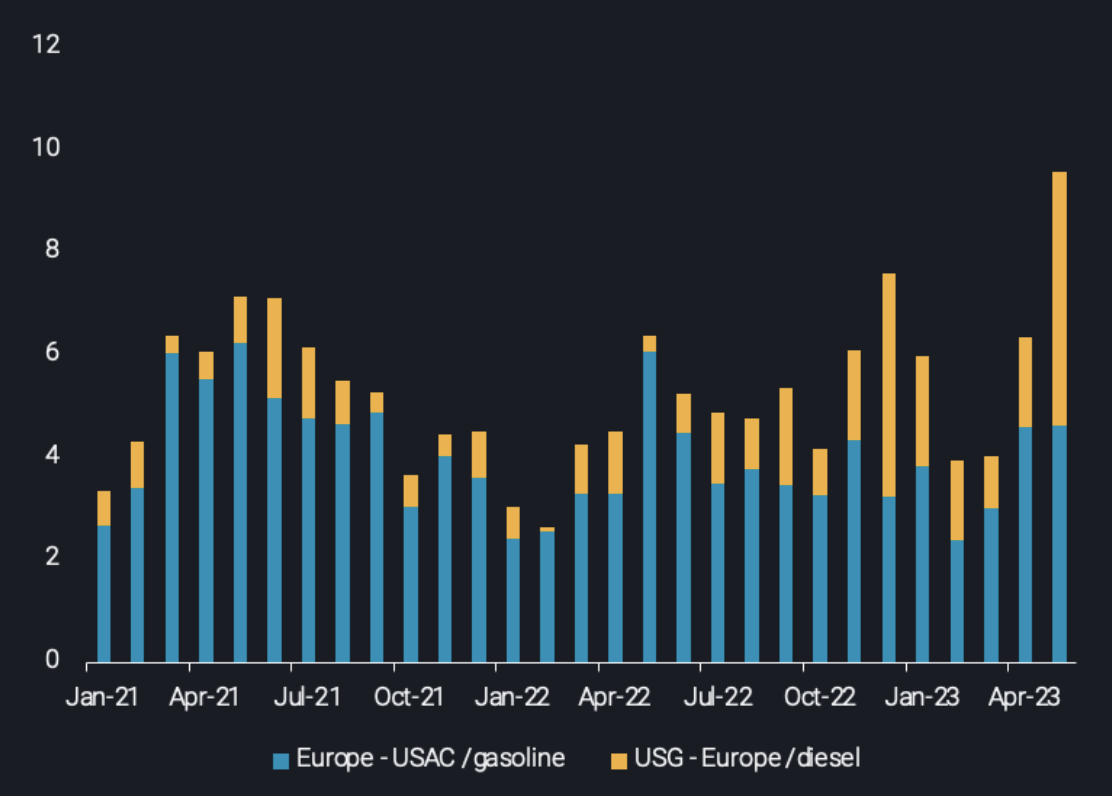

Gasoline tonne-miles for Europe-to-US trade remained robust in the onset of the summer driving season, recording a 12-month high in May, albeit lower than the tonne-miles recorded last May (13% down y-o-y).

The biggest differentiating factor on supporting MR utilisation in the Atlantic, was the surge of US Gulf diesel flows to Europe. This was triggered as the US commenced diverting supplies away from Latin America as Russian barrels were increasingly finding homes there and also partly because Europe is continuously diversifying its sources post-EU product ban on Russia. Also, concerns regarding the diesel stemming from India and questions revolving around the origins of crude processed there have made some European buyers shy away from the region (although Indian flows still remain high).

As a result of all these factors, combined transatlantic (Europe-to-PADD 1 & US Gulf-to-Europe) tonne-miles have reached an all-time high for the month of May.

Transatlantic tonne-miles for MRs, for selected routes (bn tonne-miles)

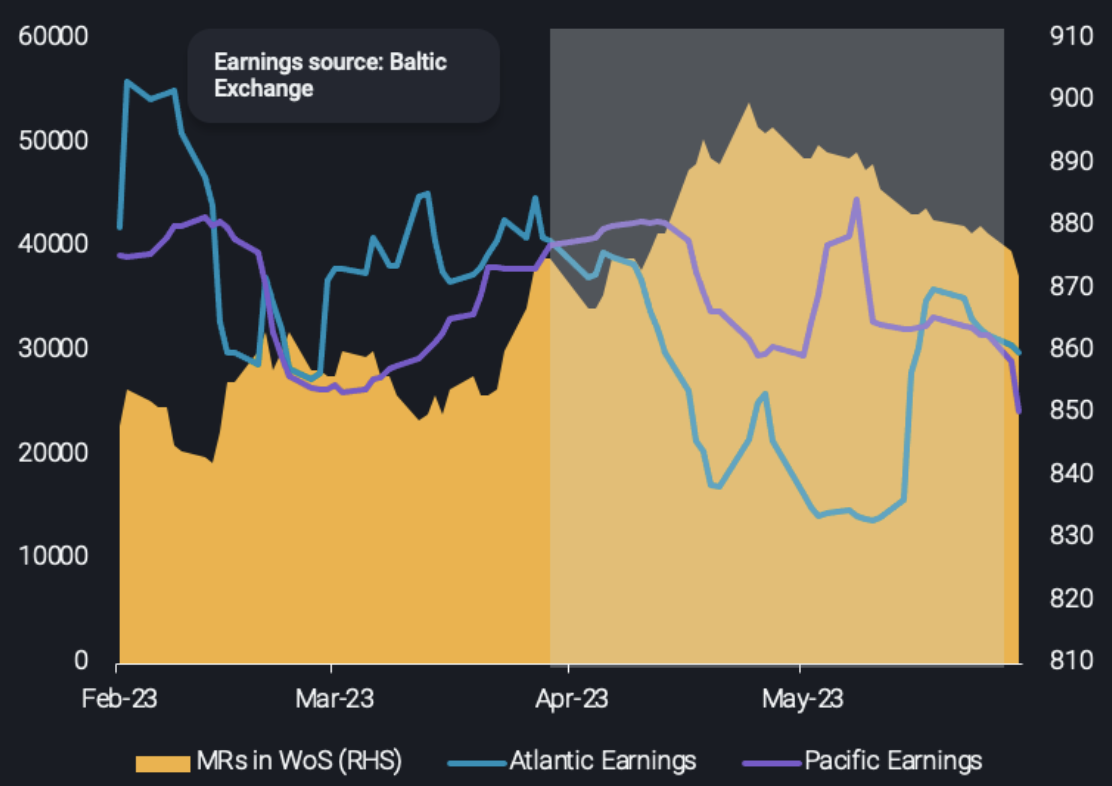

The supply-side developments have also been encouraging for owners operating in the Atlantic. Since the first week of April, MR earnings in the Pacific surpassed those in the Atlantic according to the Baltic Exchange assessments. Hence, the MR migration from East-to-West came to a halt as owners opted to remain in the Eastern hemisphere. Subsequently, this relief in MR tonnage supply in the West of Suez coincided with higher transatlantic flows and triggered the freight rate movement upwards.

Atlantic vs. Pacific Earnings ($/day, LHS) vs. MR migration in the West of Suez (no. of vessels, RHS)

Nevertheless, a note of caution should be given going forward. Whilst MR rates are double the average 2021 levels, since the post invasion period (average April 2022 – June 2023) they are actually down by 15% despite these encouraging fundamentals. This trajectory of MR rates could prove to be evidence of an economy in recession or at least softening seasonal trading patterns:

-

- PADD 1 gasoline stocks are still on the lower bound of the 5-year average, yet gasoline tonne-miles for May did not surpass seasonal levels (May 2021 or May 2022). At the same time, the US summer driving season is drawing to a close after the July 04 holiday

- Similarly core European diesel imports have declined m-o-m despite higher supply availability for neighbouring regions like Turkey, indicating saturation in the region’s demand, which still attempts to absorb the excess product supply.

- Soft refining margins in the East along with planned and unplanned maintenance schedules in Asia could drive the resumption of the MR tanker East-to-West migration with tonnage supply adding once again downward pressure on MR rates.