How quickly can Europe pivot away from Russian gas

The EU has made the bold claim that a 100 bcm reduction of Russian gas can be achieved this year. LNG will need to play a leading role in this effort. The question remains whether Europe’s LNG infrastructure can keep up.

As the war in Ukraine continues into its 21st day, Europe is facing its own monumental challenge to secure the energy essential for its economy. The recent announcement by the European Commission articulates a clear intent to dramatically reduce their dependence on Russian gas ‘well’ before 2030. Their ambitious proposal centers around the acceleration of their 2030 green initiatives (that aim to reduce gas demand), while increasing non-Russian gas supplies and mandating gas storage of 90% by October. They make the bold claim that a 100 bcm (equivalent to 75mta of LNG) reduction can be achieved this year. However for this to eventuate, LNG must play a leading role and the question remains whether Europe’s LNG infrastructure can keep up.

LNG is central to near term ambitions of a 50bcm reduction (equivalent to 37mta of LNG) of Russian gas imports. Here are the salient points on Europe LNG infrastructure:

- 184 mta import capacity is operational within Europe (excluding Turkey) with highly seasonal utilisation patterns

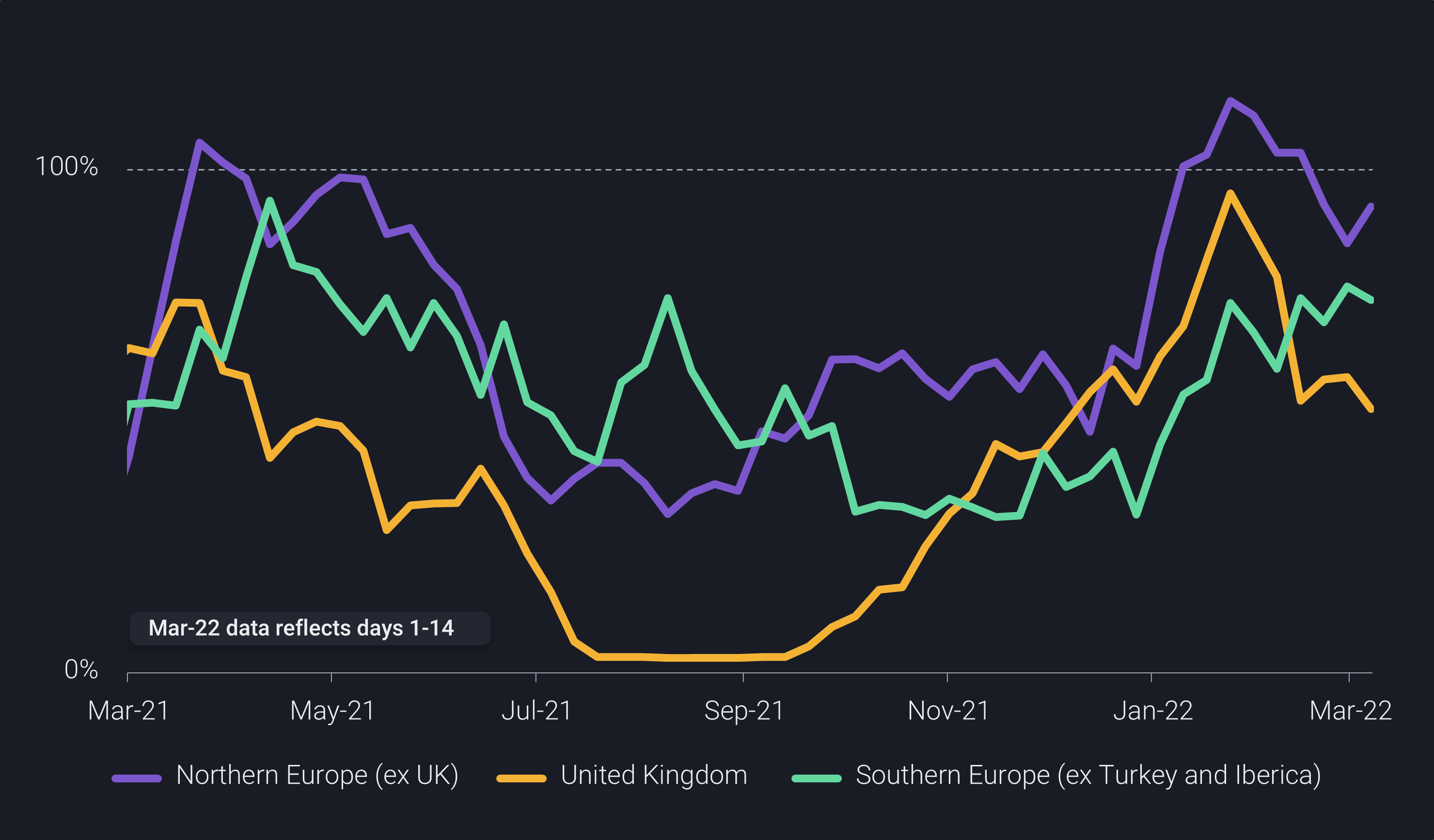

- During this January, European LNG terminals approached their physical capacity limits, reaching 82% across all of Europe according to Vortexa data

- Terminals supporting the largest gas markets in North West Europe hit their design limits to keep up with demand

- Much of the idle LNG import capacity is in Southern Europe and the United Kingdom, lacking interconnection to the central European gas markets that are highly dependent on Russia supplies

European LNG import terminal utilisation (4 week average)

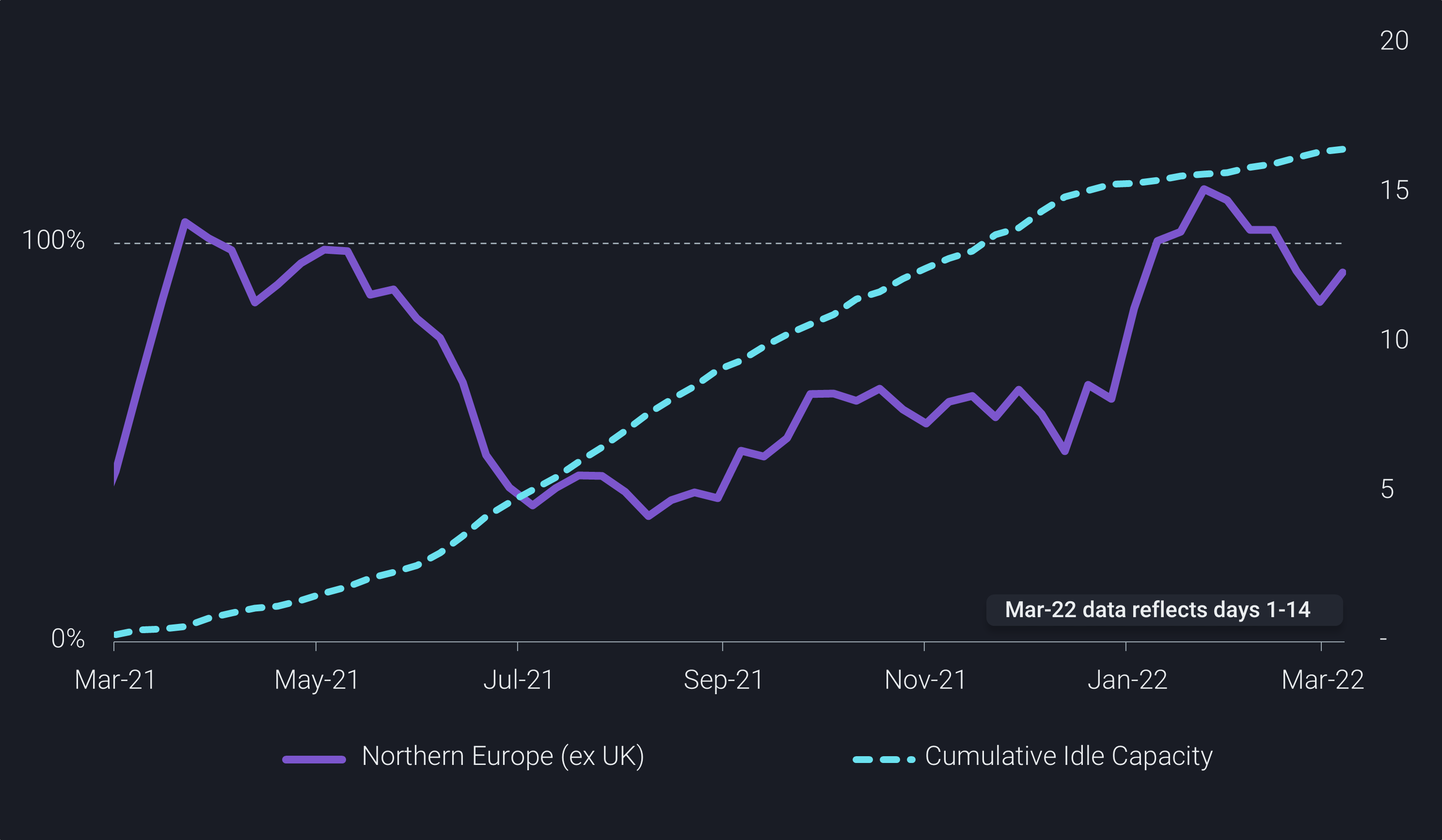

For the most exposed markets maximizing imports during the traditional off-peak months is not enough to substitute Russian supply, creating the most significant bottleneck for Germany and its neighbours

- Based on the idle capacity seen over the last 12 months, only 16 mta of incremental LNG supply could be added to the balances of the key markets in France, Belgium, Netherlands and Germany

- Already this constraint is introducing a disconnect between spot LNG transactions into North West Europe and TTF hub prices, with LNG trading at $3.3/mmbtu discount; according to Argus Media

Northern Europe: LNG import terminal utilisation (4 week average, %, LHS) and cumulative spare capacity over last 12 months (million tonnes, RHS)

Aggressive deployment of new LNG regasification capacity in Germany is being considered, leveraging Floating Storage Regas Units (FSRU) to help accelerate the project timelines.

- As seen in Egypt, where existing jetty and onshore gas network connection is available, FSRUs have been commissioned in as little as 5 months – compared to typically timeline of 1-3 years

- Two stalled German LNG import projects at Brunsbuttel and Wilhelmshaven have been mentioned as options, potentially adding 13 mta capacity to the region.

To meet the suggested pace of curtailing Russian gas imports several demand and supply side measure must be executed in unison. European politicians must enable prompt procurement of additional LNG and fast track LNG import infrastructure investments. In addition, the scope of the demand management measure ambitious and rapid implementation is unlikely to achieve the full demand reduction potential. Perhaps this herculean task can be achieved but it relies heavily on sustained politician will, strong coordination across the EU and clear initiatives for the market.