Russian roulette being played out in Ukraine, leaving the gas market guessing

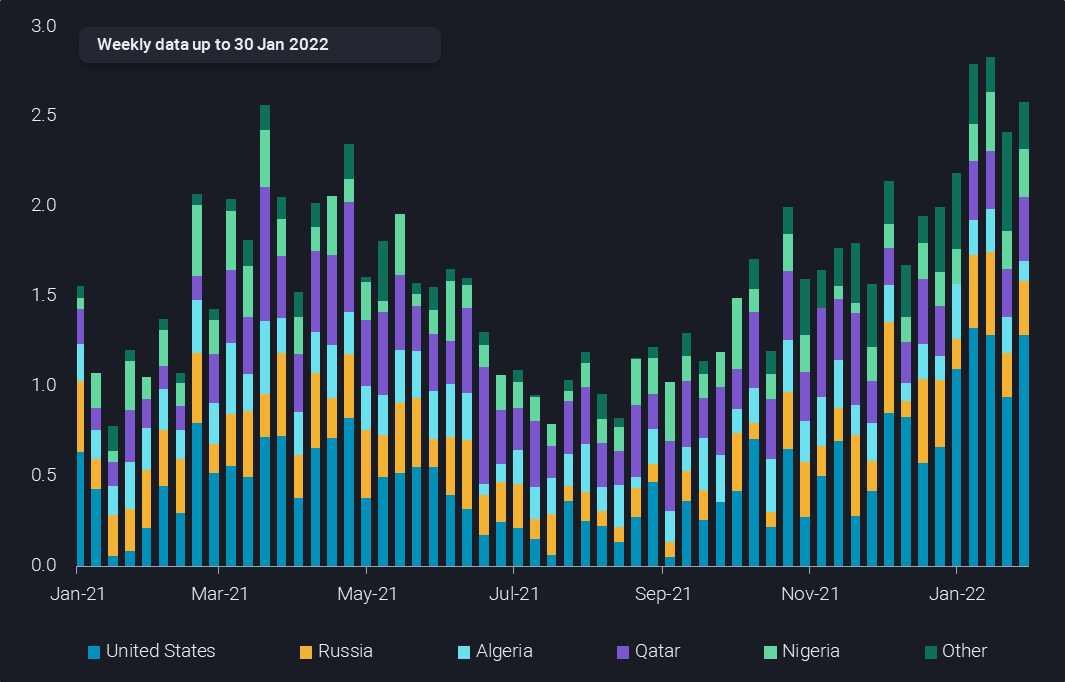

European LNG imports reach record highs in January, leaving less than 20% of free import terminal capacity – too little to cope with further losses of Russian gas.

Facing the prospect of continued or even deeper cuts to Russian gas supplies, Europe’s energy balance is in a dire position. Prolonging a notable trend, LNG imports into Europe hit an all time record of 2.8 million tonnes (mt) per week during the first half of January. Despite this, gas storage levels continue to drop. This has left Europe relying on US-led contingency planning for extra LNG supply, with talks underway with Qatar and even Australia. With global LNG exports already at capacity, how much more can feasibly be diverted to Europe?

While Europe is currently enjoying a wave of LNG vessels unloading their cargoes, leading to record import volumes, this has done little to reduce price levels.

- In January, Europe imported nearly 2.7mt on average per week

- This compares to roughly 1mt per week this time last year and 2mt per week in January 2020

The primary swing supplier has been the US, but volumes from outside the top-5 exporters are also rising strongly, including a reload cargo from as far afield as China.

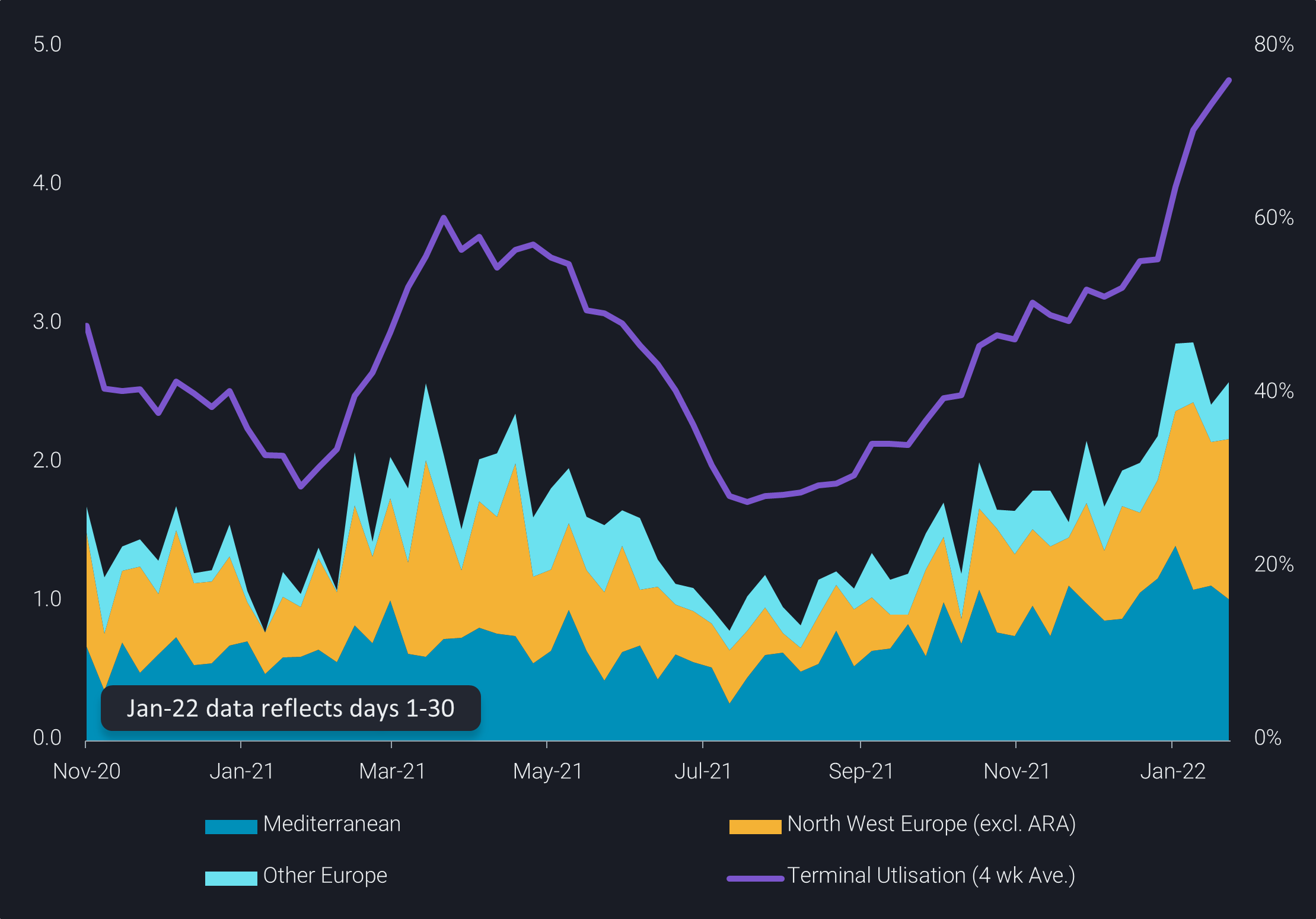

Should a conflict unfold in Ukraine and US-led sanctions follow as threatened, increasing LNG deliveries to Europe further is a key mitigation option. However, its effectiveness has an upper cap, as the continent will face a dual challenge, availability of global LNG supply and managing import terminal limits. Currently, import infrastructure is already approaching physical capacity limits (82% across all of Europe) and North West Europe terminals are running at higher levels, making them the key bottleneck for increased imports.

The chilling facts of the European gas outlook:

- 2022 has started with Russia gas exports to Europe falling to 55% of 1H 2021 levels according to Entsog’s data

- LNG imports are already at record levels in January (11.4mt) placing stress on import capacity. With 82% utilisation of regasification capacity through the first 2 weeks of January

- Gas storage is 28% or about 170TWh below the 5-year average (which is similar to year-ago levels) as of 30 January, according to AGSI+ data

Availability of extra supply has its challenges, as the LNG industry has been pushed to operational limits since the gas price surge that started last summer. Solutions are being explored to provide a security of supply backstop for Europe, led by the US government. Qatar has committed to a supply guarantee for Europe for their remaining uncommitted volumes, which may be able to offset a portion of Russian gas supply losses. Support has also been sought and apparently secured from as far afield as Australia.

What can one expect should the Ukraine-Russia crisis escalate with official Russian troops invading its Western neighbour? One could argue that a hard stop to all Russian gas exports to Europe, driven by either side, is an extreme bookend scenario (as it is for crude oil and refining products). A more likely outcome may see a halt to Ukrainian transits (which are already at historic lows of 15% of Russian pipeline supplies to Europe), other routes for Russian gas becoming less reliable (but remaining at similar levels to today) and the Russian Yamal LNG cargoes offloading in Asia. This outcome would add extra European demand for LNG in the order of 1.9 – 3.1mt per month, or about 30-50% of average European LNG imports in 2021.

Will Asian buyers remain bystanders?

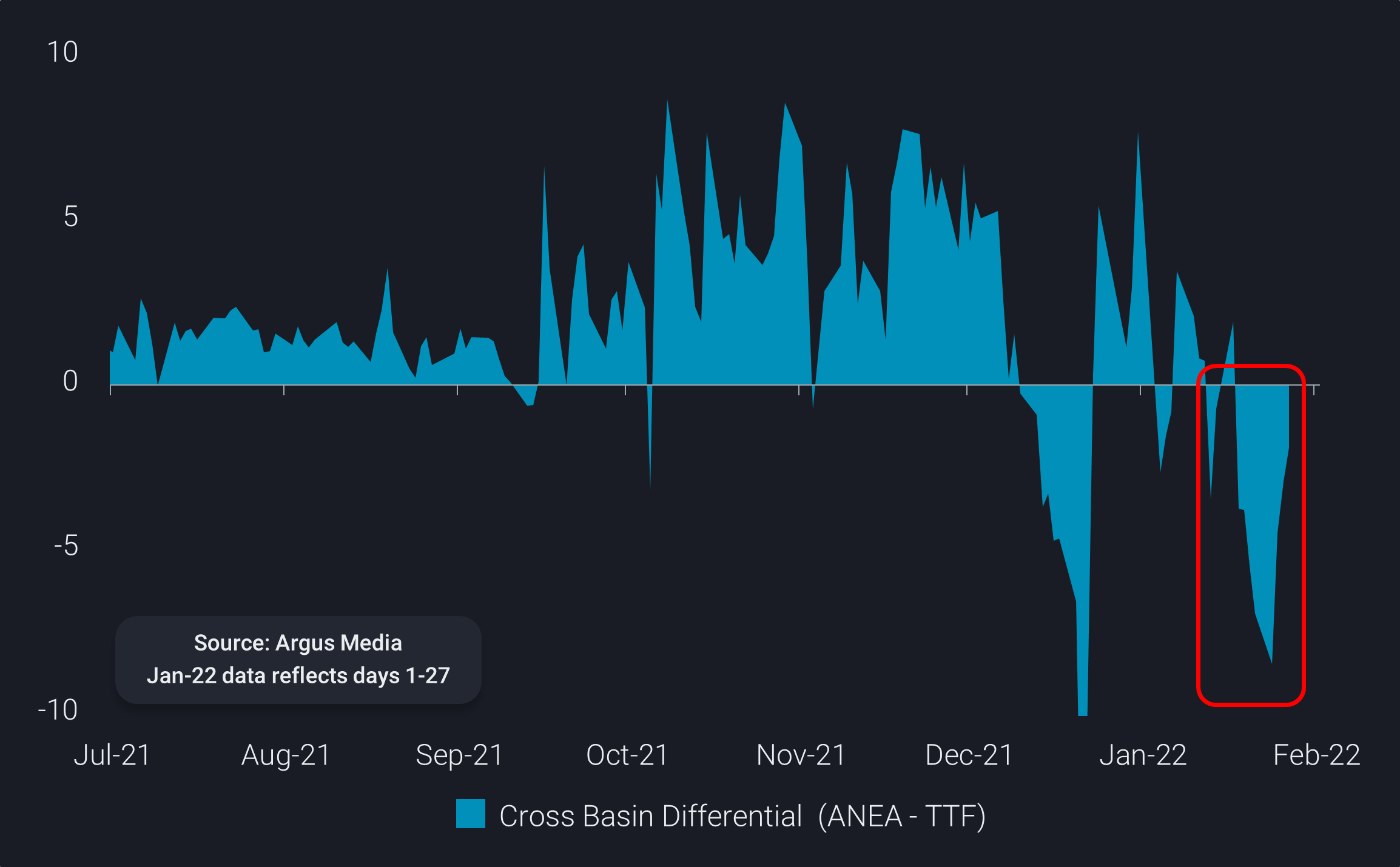

A superior LNG storage strategy has kept Asian buyers in an advantaged position throughout this winter, aided by milder weather in the Northern regions and targeted demand management. Chinese spot LNG demand is starting to wane – the result of Chinese New Year holiday cooling industrial demand, the over-performance of pipeline imports (from Russia), plus the start of new long term LNG agreements. In contrast, Japanese buyers have been observed in the market again to a certain extent, pushing the March cross basin differential back in Asia’s favour.

Cross Basin Price Differential ($/mmBtu, ANEA month 1 minus TTF month 1)

The disciplined focus on security of supply is helping to protect Northeast Asian buyers from the threat of new record LNG prices should Russia invade Ukraine. However, this foresight has not been adopted to the same extent by their European peers, who would be left scrambling for the most expensive cargoes.