Asia’s naphtha demand faces growing headwinds

Asia’s naphtha cracks are facing growing headwinds from slowing gasoline blending and petrochemical feedstock demand. Soft tanker rates and China’s new cracker start-ups may offer some tailwinds.

Asia’s naphtha cracks have been steadily rising since April, bucking the trend of softening transportation fuel cracks. A seasonal switch in cracker feedstock from LPG to naphtha and strong aromatics margins (until September) have bolstered market fundamentals. However, growing headwinds are weighing on naphtha cracks. Regional aromatics margins have begun to retreat in recent weeks, while reforming margins have faded since the end of the Western hemisphere peak summer travel season. Northeast Asia’s ethylene cracker margins are also under pressure, with potential run cutbacks looming.

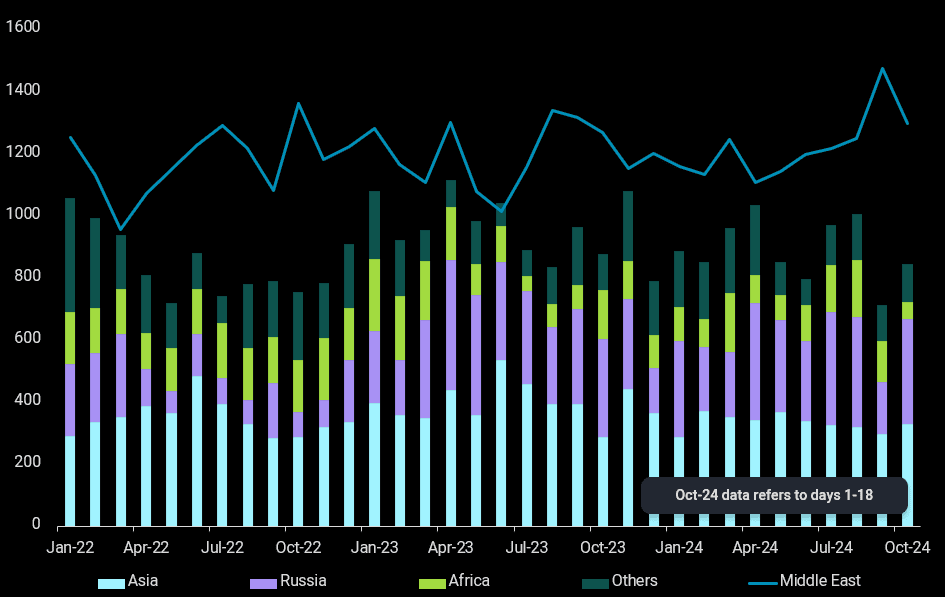

Naphtha imports into Asia in the first half of October have declined for a second consecutive month to 2.1mbd, with Japan and Singapore leading the m-o-m drop. Russian naphtha arrivals have rebounded to over 330kbd this month, with imports into Singapore hitting a 9-month high of 96kbd. However, Russian supplies to Asia will likely slow over Nov/Dec as the country’s naphtha exports are on track to reach a seasonal low this month, with about 900kbd of refining capacity taken offline for maintenance. No naphtha cargoes have been loaded from major Russian ports like Vysotsk and Nakhodka so far in October. The declines from Russia are offset by rising supplies from the Med, with volumes loaded to Asia in 1H Oct climbing to a 9-month high of 200kbd.

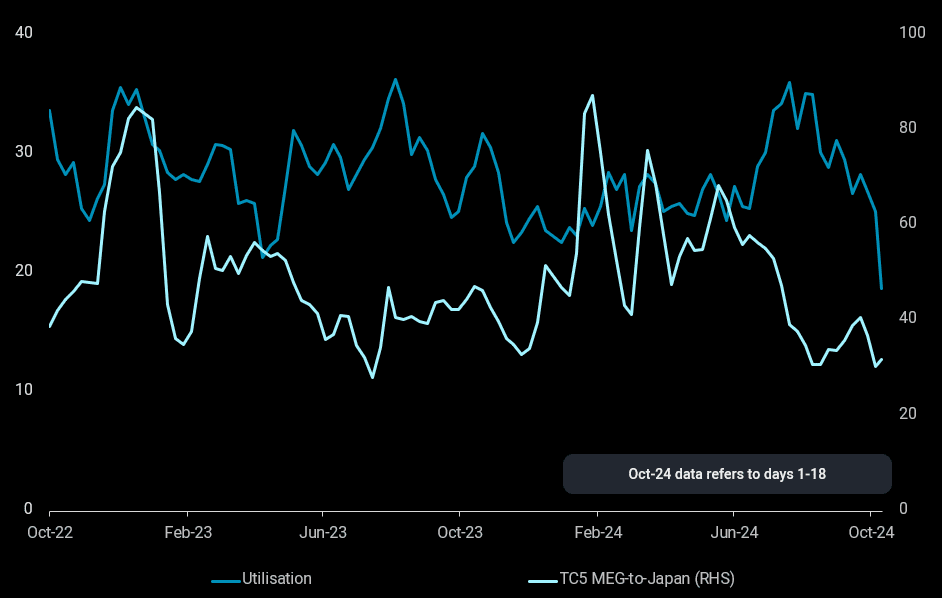

Soft LR tanker freight rates have also provided relief for Asia’s naphtha buyers amidst rising naphtha prices. TC5 MEG-to-Japan LR rates are currently near the bottom of their historical range, about one-third of January’s levels. Declining LR utilisation on MEG-to-Asia trade route as well as ample global LR supply tonnage that has faced stiff competition from supertanker clean-ups are expected to keep LR rates subdued, unless there is a significant demand recovery by year-end.

Six new naphtha-based ethylene crackers are scheduled to come online in China between Q4 2024 and 2025 (Argus), with one of Yulong refinery’s crackers expected to start up next month. As Yulong’s crackers are taking their feedstock from the refinery, the start-up will not boost the country’s naphtha imports. The start-up timeline of the remaining crackers is less certain, challenged by weak margins. However, several of the independent crackers may provide upsides on China’s naphtha imports when they come online next year.