Atlantic Basin product cracks – is diesel still in the driver’s seat?

Atlantic Basin clean product cracks weaken under the pressure of growing refined product supply from the Middle East and Asia despite the strong regional pull from Latam, low stocks in USAC, and European uncertainty for alternative diesel supplies.

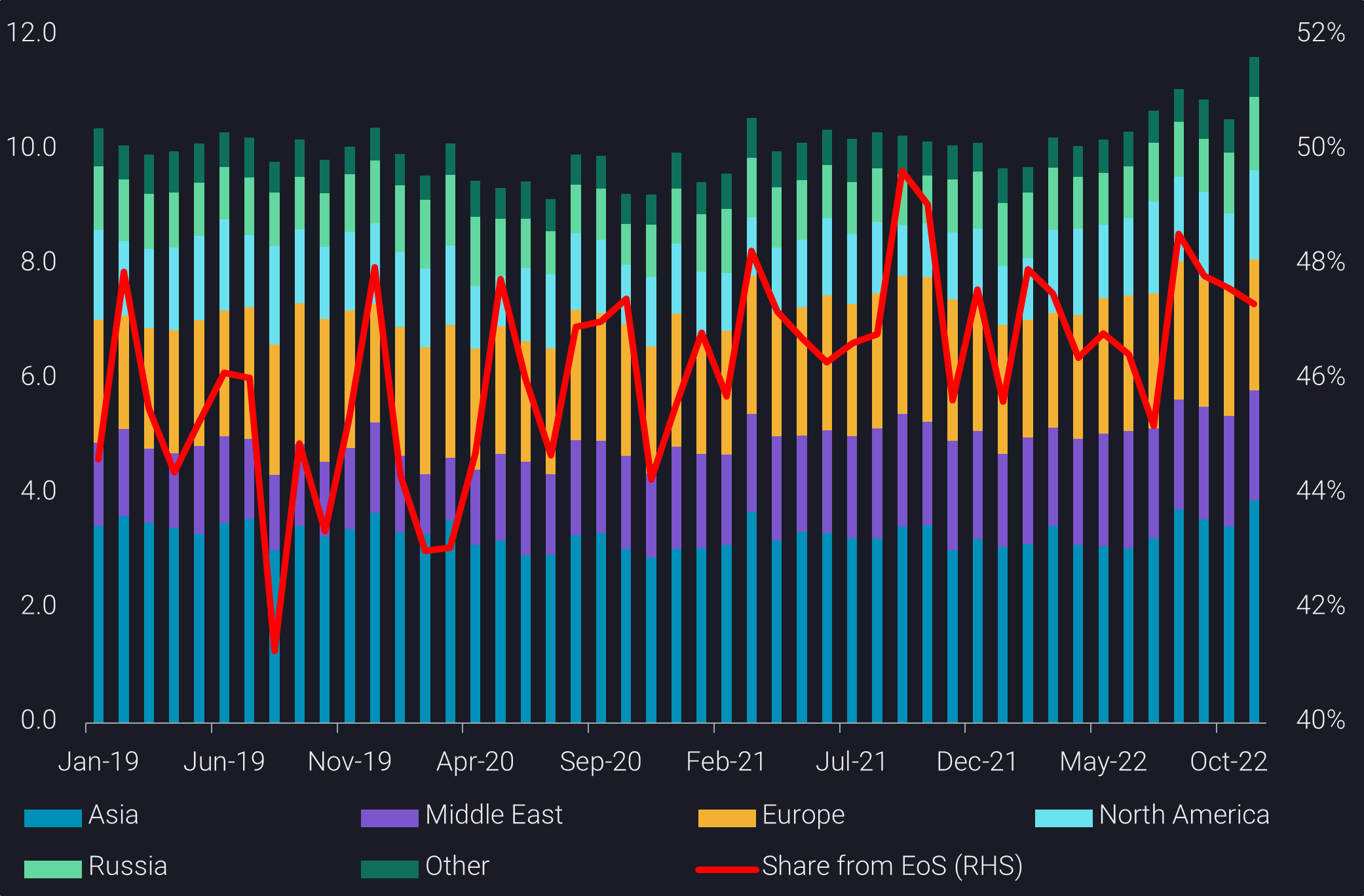

Global diesel cracks first weakened in the East of Suez markets in mid-September and then the Atlantic Basin since mid- October as refineries returned to normal operations (post maintenance/strikes) and new refining capacity ramps up in the Middle East and China. The latter is generating more available barrels on the water, pushing global diesel liftings up by 7% in November compared to the previous high observed in August 2022.

The risk of diesel supply tightness in Europe has declined as record imports during Oct/Nov averaged 1.73mbd, 26% higher than Oct/Nov 2021 with around 40% originating from Russia due to a big pre-sanction Primorsk diesel export programme. The large seaborne diesel influx coupled with a warm European winter and disappointing Chinese demand reveal a surplus unforeseen a few months ago – when Atlantic Basin cracks surged largely due to global diesel supply uncertainty. Nevertheless, even with the current weakness in diesel crack spreads, values continue to remain more than double what they were pre-invasion (Jan-Feb 2022) (Argus)

Strong regional diesel demand provides continued support

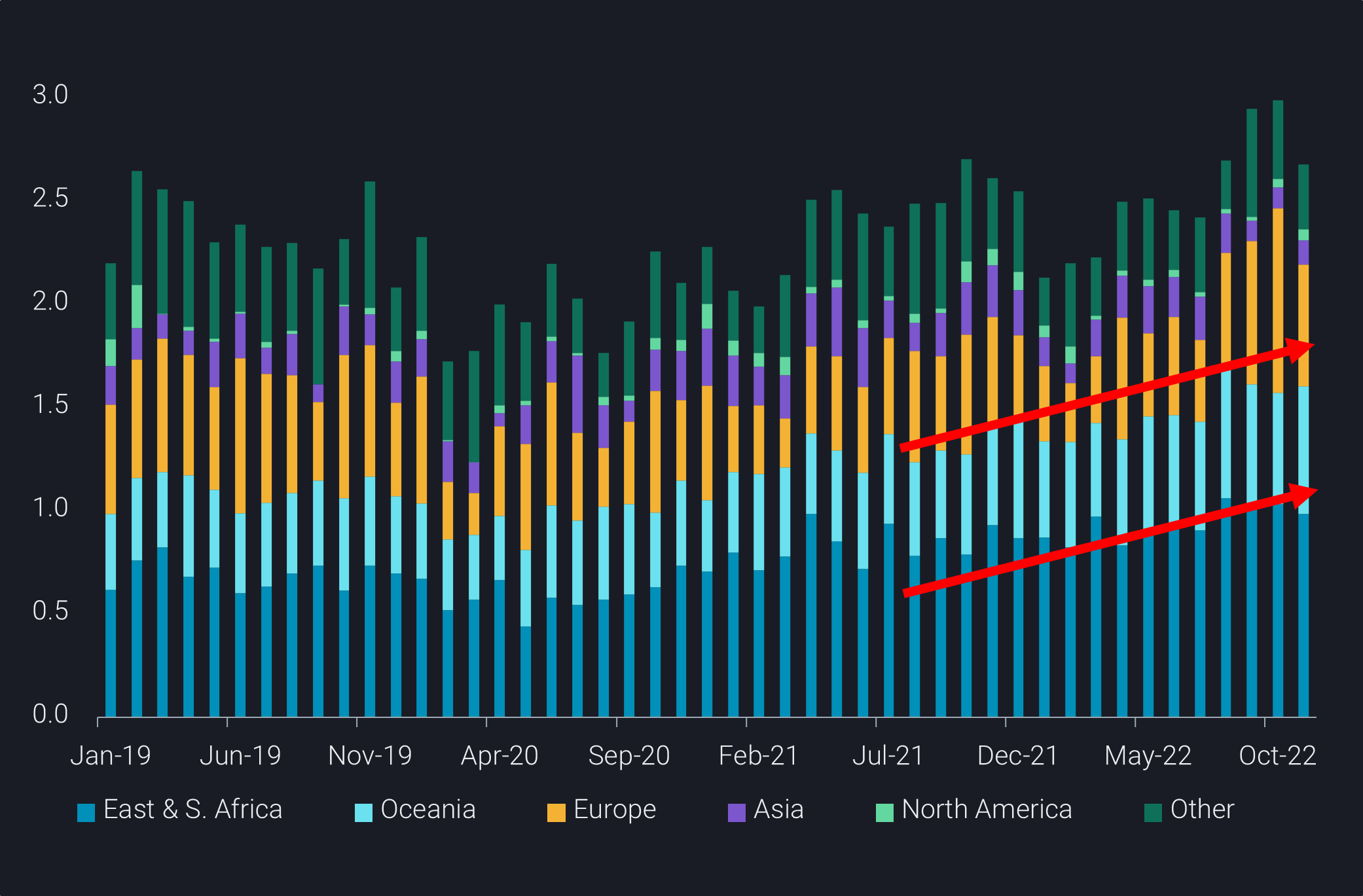

Although we continue to see a historically strong pull for diesel from Latam, Oceania, East and South Africa, and PADD 1 (relatively), the clean product supply situation is looking somewhat more well supplied from a regional perspective. Jet regrades, the jet vs diesel spread, in Northwest Europe and Asia have normalized, signaling global refineries to adjust yields to produce more jet and less diesel, at the margin.

But as Europe looks to wean itself from Russian diesel completely by February 2023, it will have strong competition from Oceania, East and South Africa, which will amplify any potential short-term supply shocks (refinery strikes, storms) and support diesel cracks until even more refinery capacity comes online in the later part of 2023.

LatAm clean products demand continues to outpace 2019

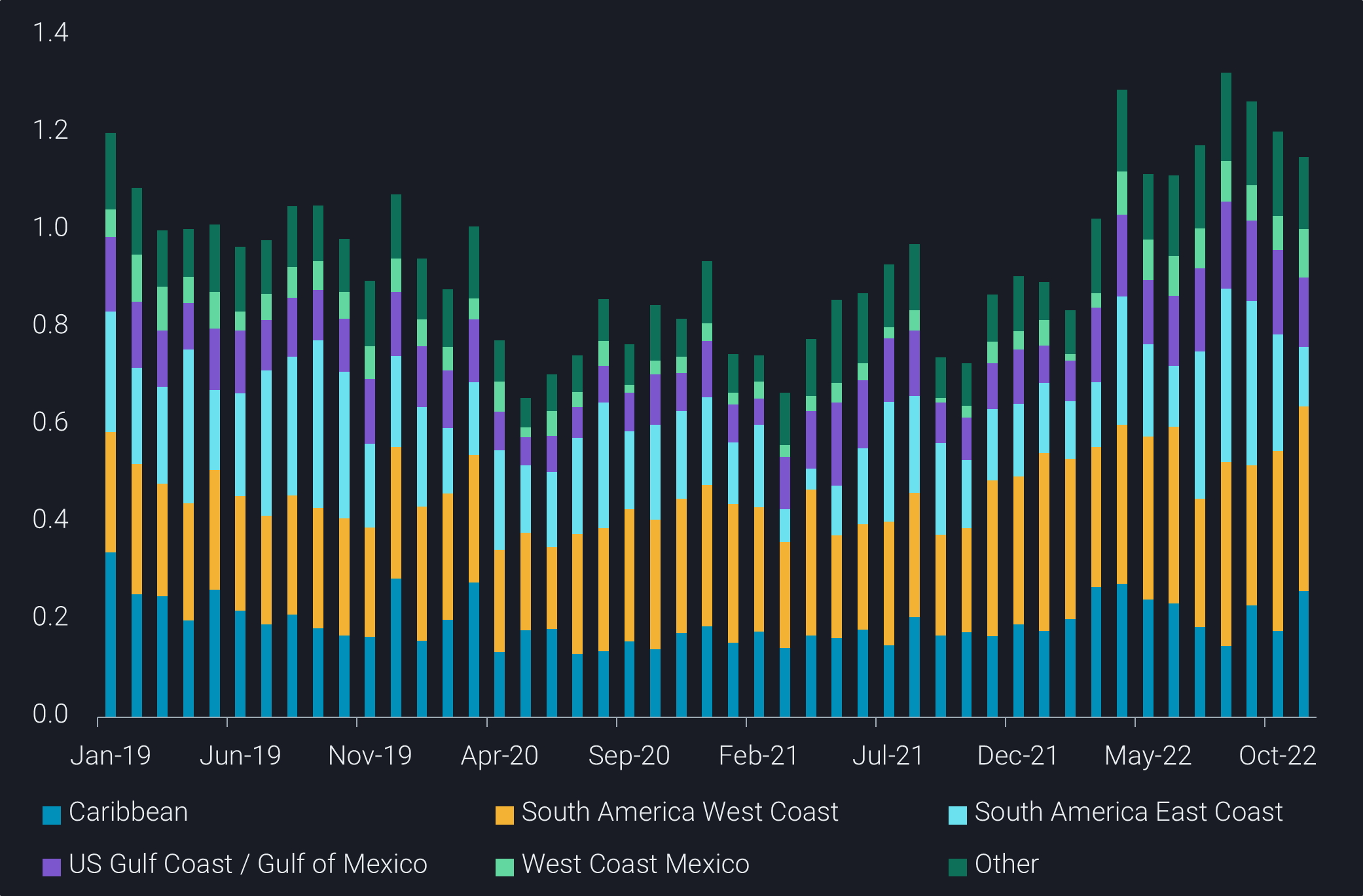

Meanwhile, LatAm product imports have outpaced pandemic levels with some recent signs of slowing (Brazil) after reaching dataset highs in Sept/Oct 2022. The recent peak in imports tied with agricultural demand for the 22/23 harvest season due to strong crop yields, increase in planted areas and strong rains. Chilean diesel imports surged in August to meet power generation needs amid a very long drought which continues to drive seaborne barrels at relatively strong levels, while Mexico’s diesel continues to serve as a pillar of strength in the market, with seaborne imports having increased 19% Jan-Nov 22 versus Jan-Nov 19 as commercial activity surged following a recovering economy.

Gasoline and naphtha cracks have little room for recovery

As for the Atlantic Basin light distillates market, gasoline and naphtha cracks are stabilizing after disappointing 2022 US gasoline demand due to historically high retail prices/poor US economic conditions and slight strengthening in naphtha due to short lived demand in South Korea. Although there could be some bright spots for US gasoline in Q2 due to seasonality, lack of stocks (PADD 1) will likely be covered by ample supplies in Europe.

As for naphtha, although we have seen a small recent uplift in cracks, the recovery depends largely on the revival of the Asia market, led by China. With two integrated refineries in the country coming online Nov/Dec 2022, it will likely continue to pressure naphtha margins.

A few supporting factors for diesel cracks in Q12023

Despite growing fears of a deepening recession in the Atlantic Basin, there are a few Q1 2023 demand drivers that could offer support to the global diesel market albeit not likely to the levels seen in 2022. The biggest, and least predictable factor is a late and sharp drop in winter temperatures in Europe and the USAC. Other factors include; China bolstering vaccination programs to emerge from the strict lockdown policies reviving local demand, and the difficulty in the replacement of Russian clean products after the ban on tanker insurance and other services for clean product exports moves closer (5 Feb 2023).