Clean product margins strengthen despite the crude price rally

In this insight we explore the current support behind global clean product margins, focusing on global gasoline and diesel trade flow dynamics.

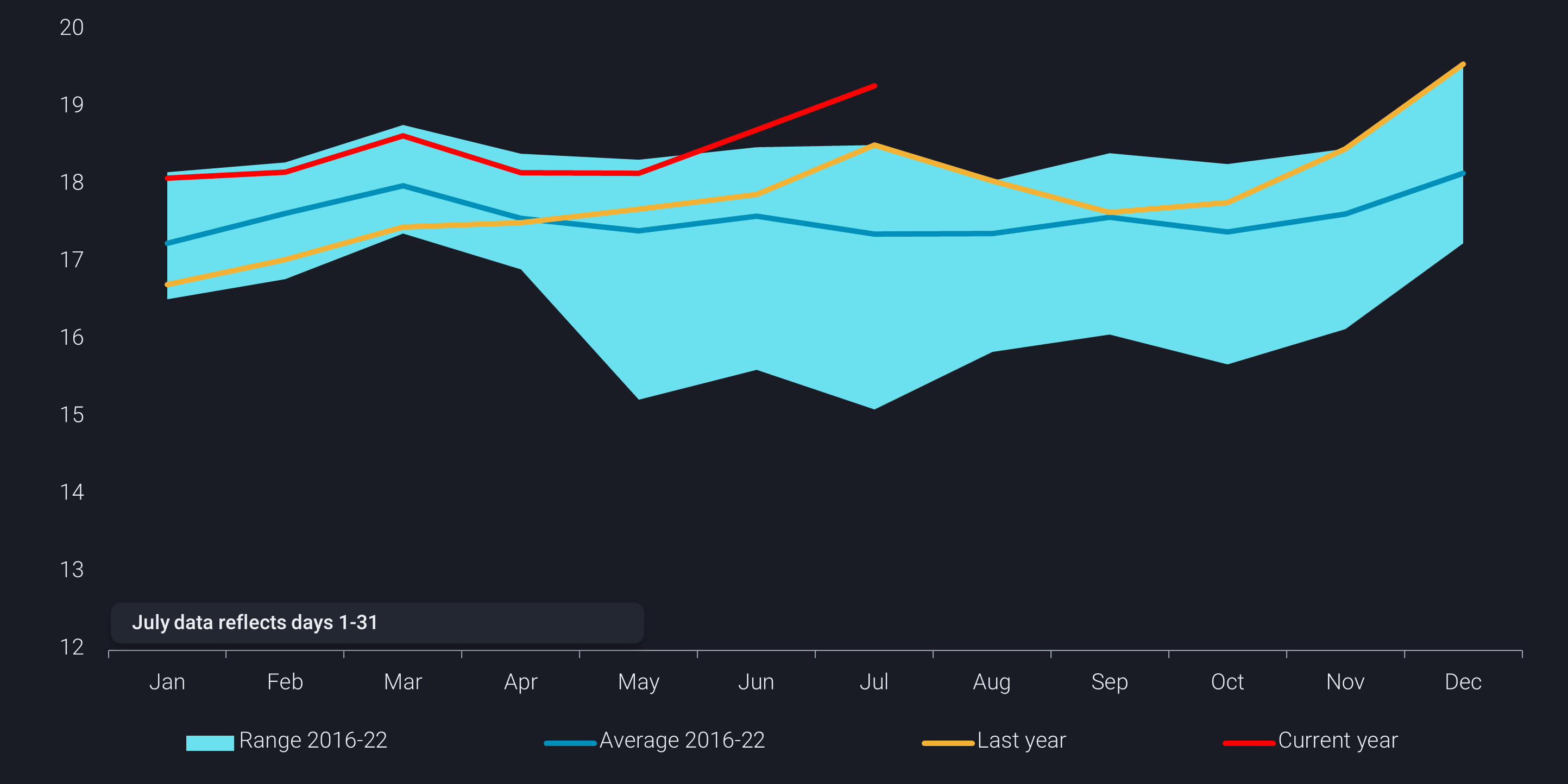

Clean product margins are reaching levels unseen since Q1 2023 in Asia, Europe, and North America while seaborne clean product export levels have surged above the seven year range (red line) indicating ample supply availability. At the same time, we see crude prices move up due to various big producers cutting seaborne supplies. What has changed recently to drive up the margins at a time of slow economic growth and high commodity prices?

Atlantic Basin gasoline margins propped up by reduced local supplies and low stocks

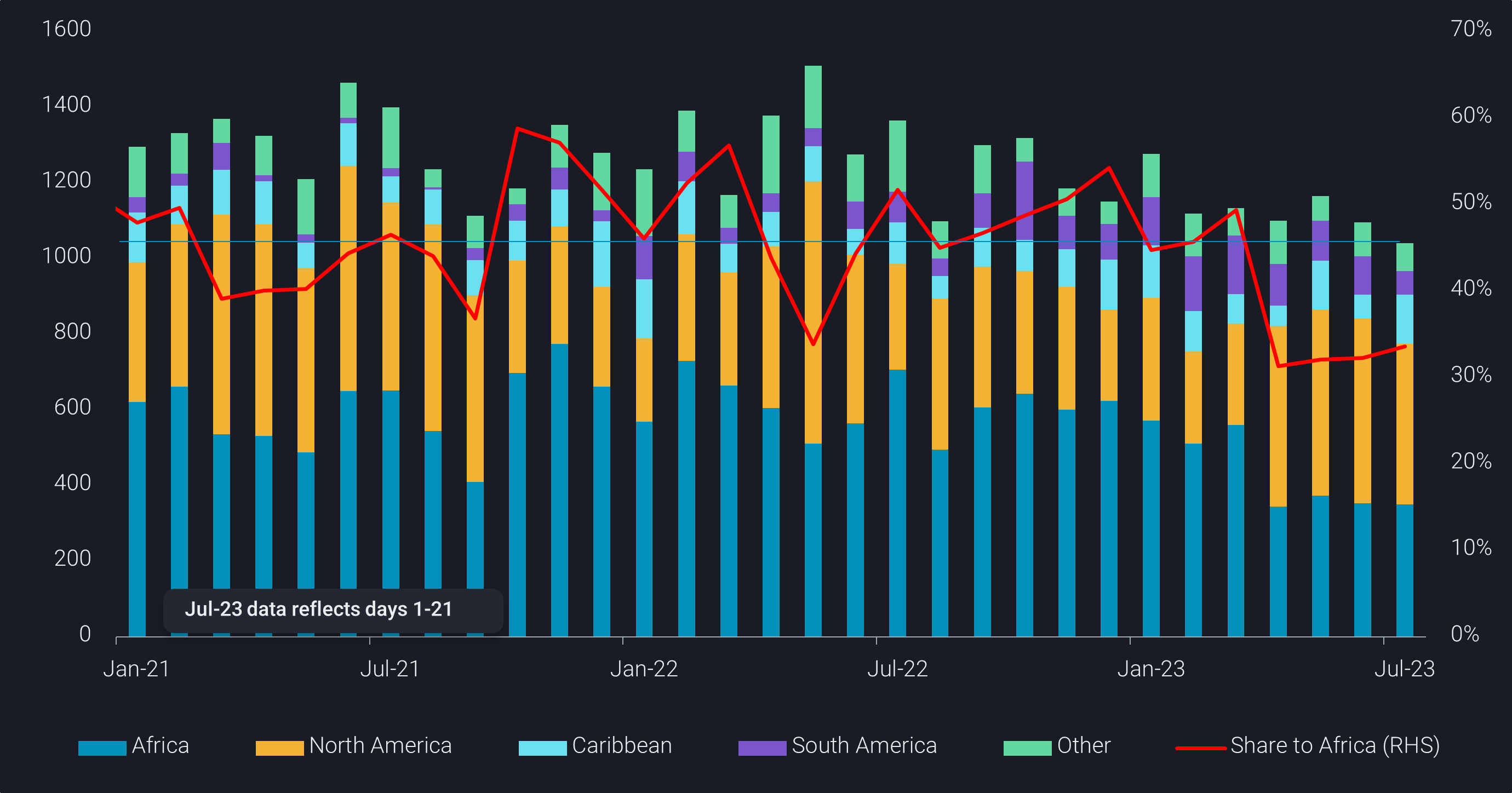

European gasoline exports, the dominant supplier to key markets including PADD 1, WAf, and LatAm, declined by 19% in Q2 2023 compared to Q2 2022 likely due to lack of blending components and ongoing refinery outages. Meanwhile, total PADD 1 seaborne imports grew by 25% and LatAm by 9% in Q2 2023 compared to Q2 2022. While declining Nigerian demand (-15% Q2 2023 vs Q2 2022) has freed up some of these European supplies to flow elsewhere in the Atlantic Basin, lower volumes from Europe have opened up opportunities for the East of Suez growing gasoline supply.

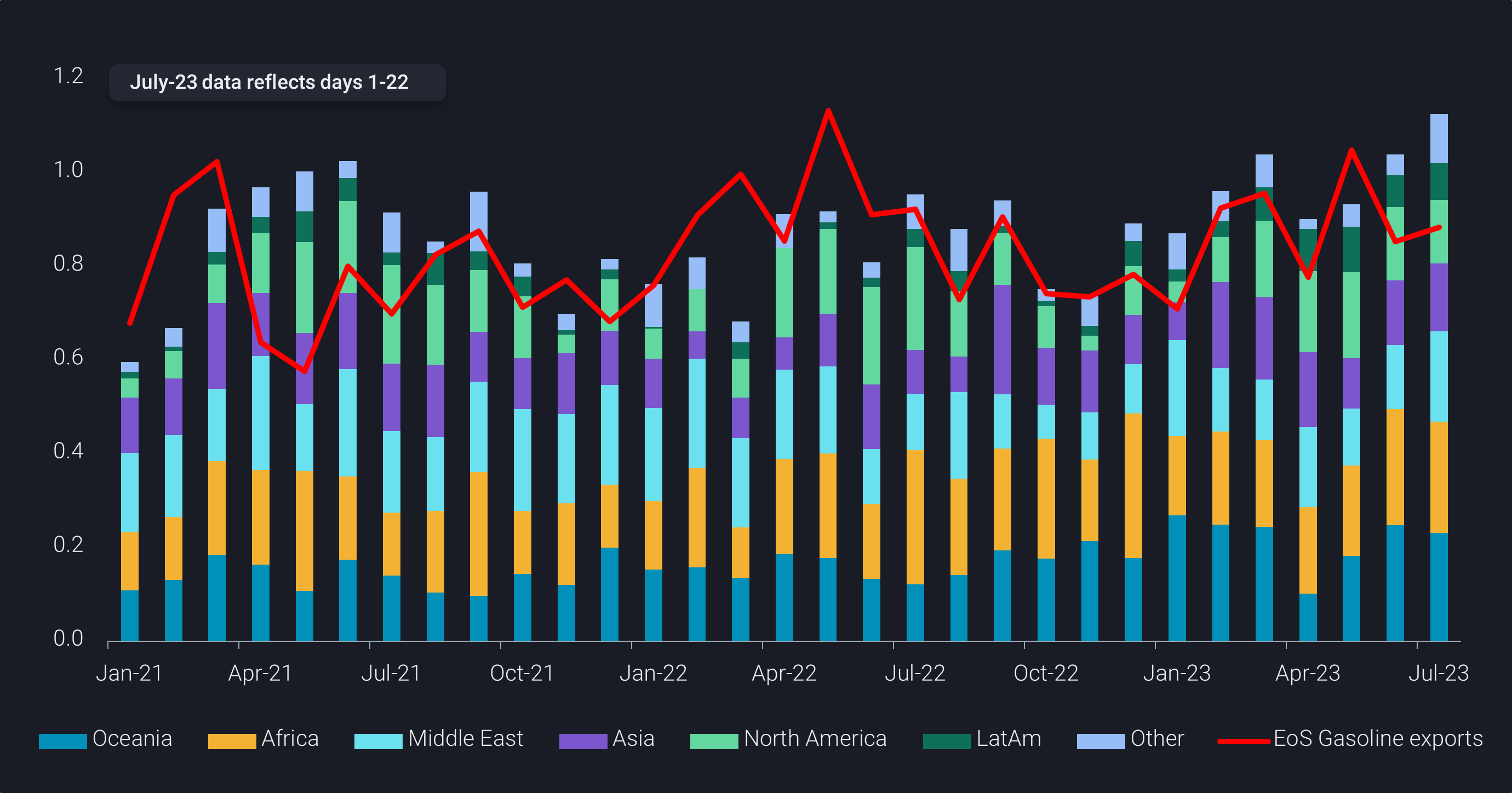

East of Suez is finding homes for barrels previously supplied by Europe

New refining capacity in East of Suez markets is expected to ramp up with over 400kbd of gasoline production by Q2 2023, pressuring local markets. Oceania, starved by a lack of refining capacity, increased gasoline imports by 12% in Q2 2023 compared to Q2 2022, while imports into East Africa doubled. And although Asian demand has been relatively resilient in light of the recent economic downturn, we see barrels moving longer distances into Atlantic Basin markets supplying the major demand centers. PADD 1 imports from India increased by 25% while LatAm gasoline imports from Asia increased by sevenfold in Q2 2023 compared to Q2 2022. The crux of it is that East of Suez is finding homes for barrels previously filled by Europe while servicing growing demand from Oceania, East Africa and a somewhat resilient local demand.

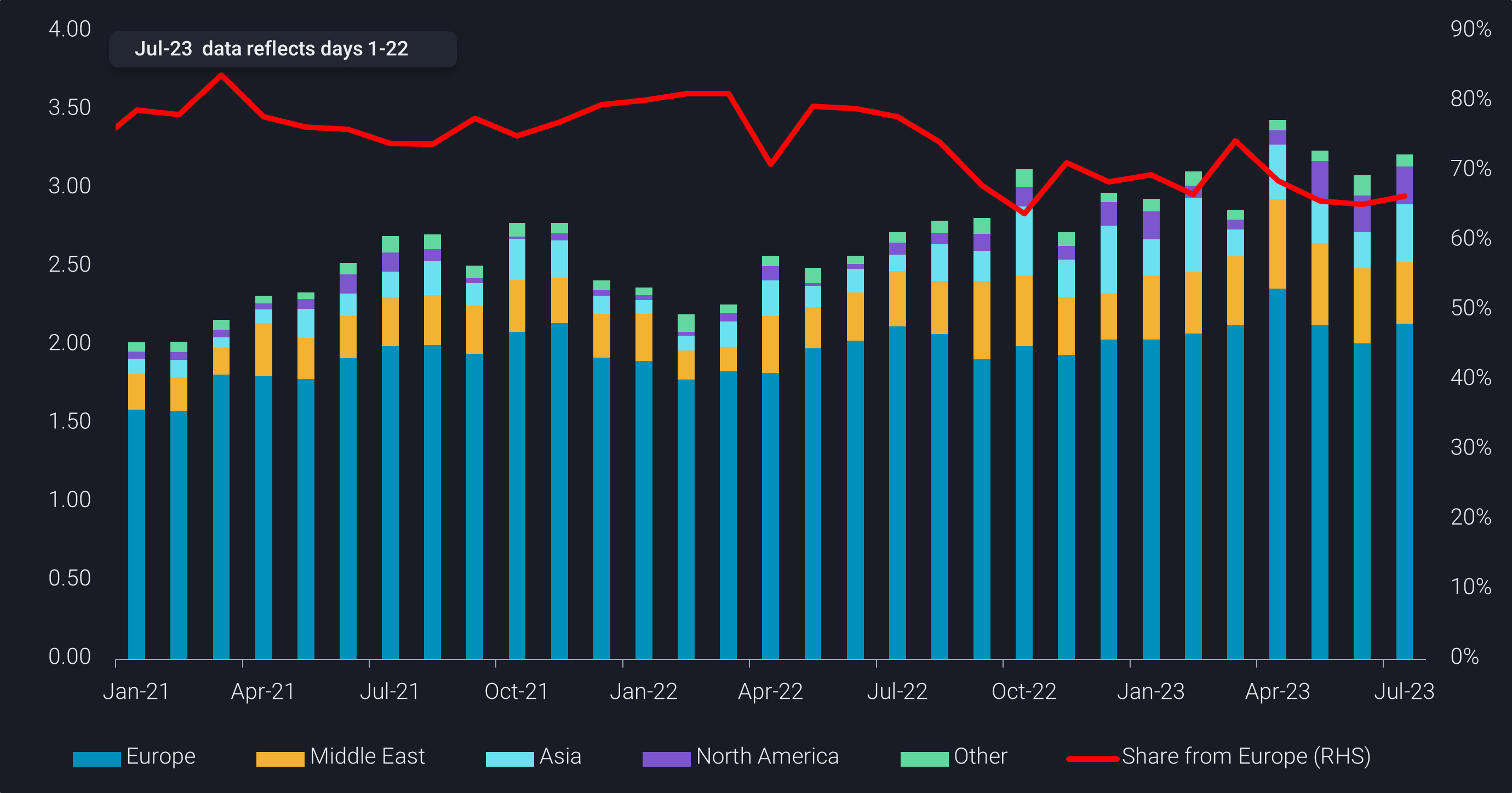

Lack of European domestic supplies due to outages underpins elevated diesel margins

European diesel cracks have returned upward to March levels hovering around $30/barrel (Argus), largely due to stockdraws from the builds seen in late 2022 coupled with ongoing refinery outages which are suppressing intra-European flows. Despite the growing supply potential from East of Suez markets, a prolonged closed arb to Europe from Asia has led Europe to look toward the US Gulf Coast for resupply as well as elevated volumes from the Middle East.

Although Europe is also well past refinery turnaround season, it remains haunted by a series of unplanned outages first with Shell Pernis (400kbd), Shell Wesseling (334kbd), TotalEnergies Donges (200kbd), Repsol’s Bilbao (220kbd) and PCK Oil Schwedt (223kbd) while the Med suffers from a heat wave which has rumored to have caused refinery run cuts and outages in the Sarroch refinery in Sardinia (300kbd) (Argus). Unplanned outages have also kept supplies relatively thin from Asia (Malaysia, Vietnam, South Korea) coupled with low runs in China and narrow export margins.

Meanwhile in other markets, LatAm diesel import demand is down by 10% in Q2 2023 compared to Q2 2022 while Oceania is posting 20% gains in the same time period, offering logistically closer support to the growing diesel production from the Middle East.

As we move closer toward autumn, seasonally we could see weakened demand for gasoline and increase buying for diesel despite the strength in the service sector (gasoline demand) that has provided respite from the industrial recession (diesel demand). While there is continued support for refined product margins in the way of refinery outages that may last until the autumnal refinery maintenance season, the question is how long these interruptions will continue to support gasoline cracks when seasonal demand curtails. Diesel may have some upside if prices in Europe need to draw in volumes from Asia later in the year. At the same time, China is expected to announce a fresh batch of clean product quotas in early August which may limit any upside potential in Asian refined product cracks, especially considering the current run cut environment. There is always continued high Russian diesel exports to consider (14% of the seaborne export market compared to Asia 29%) but limited nearby destinations will mean a curtailed impact on European margins, while pressuring East of Suez markets.

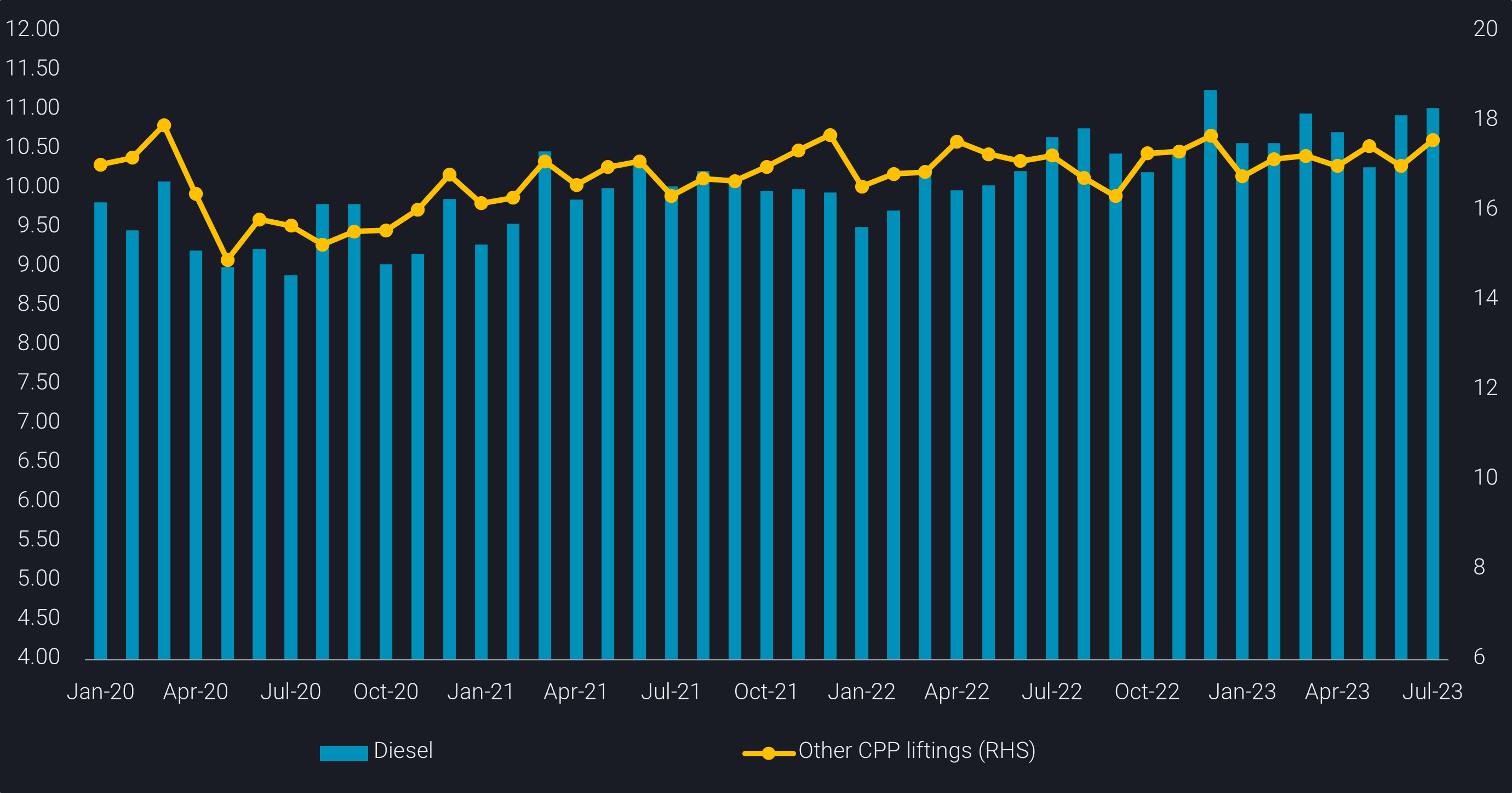

Global diesel vs other cpp liftings (mbd)