Could USGC diesel continue to attract European buyers?

US exports of diesel to core-Europe are set to reach multi-year highs in January. In this insight we explore the factors behind these recent highs and whether they could continue.

Counterseasonal surges of diesel from the US to core-Europe* have occurred in the past largely due to unplanned refinery outages in Europe and a lack of replacement barrels from other sources. Normally, they have been short bursts of temporary and prompt cover lasting for only one or two months. The last multi-month increase was observed over April – August 2017, when US diesel exports to core-Europe were up by 75% from April peaking at 410kbd in August 2017.

The current upward trend started in November 2023, despite PADD 1 stocks falling to the bottom of the five-year range (EIA).This near tripling of US diesel exports to core Europe from October 2023 – January 2024 places the US as the second highest marginal supplier to Europe behind the Middle East for January (340kbd ex-US vs 370kbd ex-Middle East respectively for days Jan 1-19).

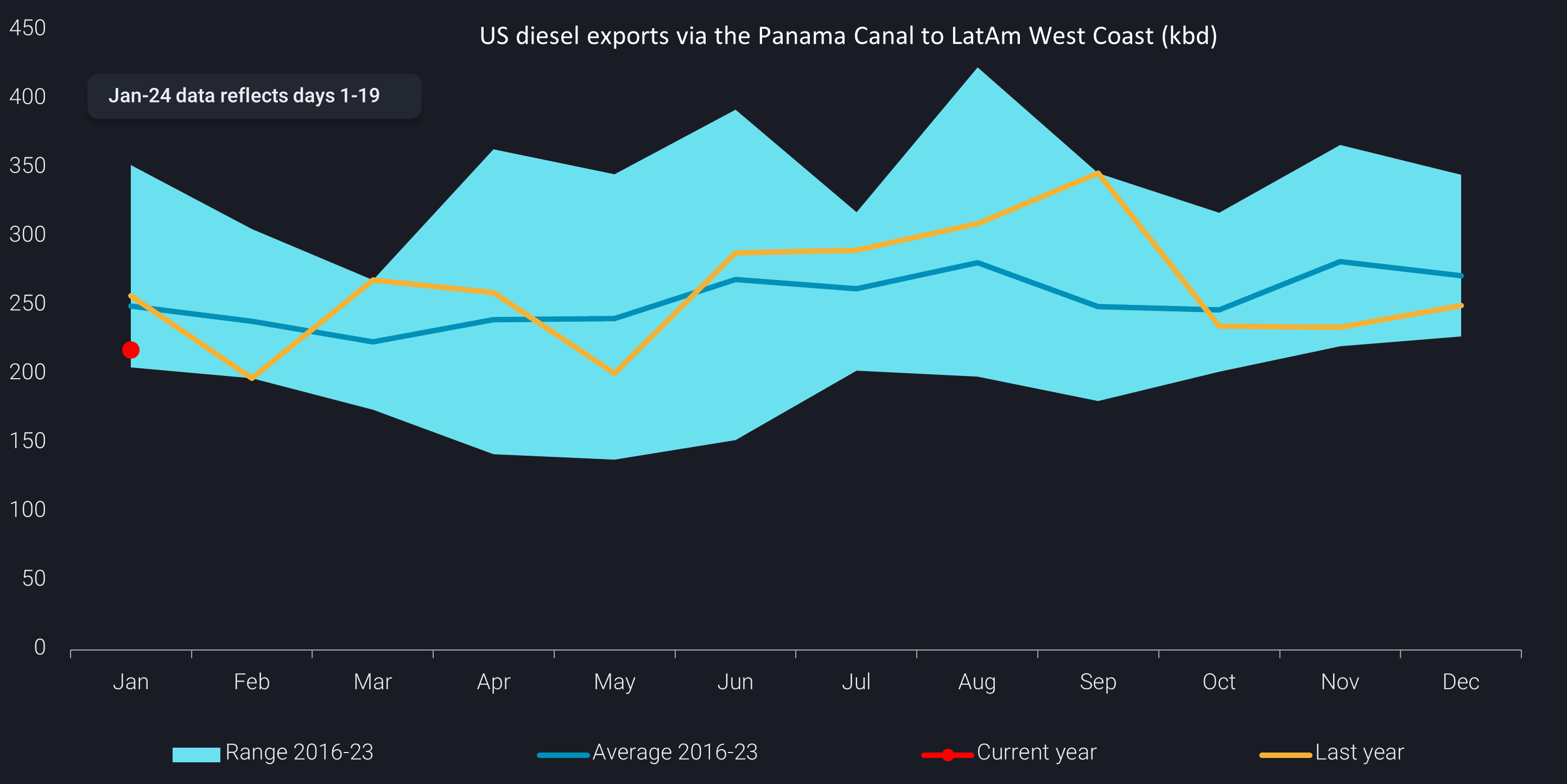

Panama Canal constraints free up USGC diesel toward Europe

In addition to the PADD 3 refiner’s ability to make strict winter specification diesel e.g. for the German market, another driving factor pushing higher US diesel exports to Europe has been the ongoing Panama Canal drought, dropping water levels and restricting vessel transits. This trend has meant fewer vessels from the USGC could reach LatAm West Coast, plunging imports down below the eight year average, towards the bottom of the seasonal range and 15% lower than full month Jan-2023. In addition, the spread between prompt European diesel and USGC prices peaked at 120$/tonne early December (Argus), helping to increase loadings pointed from the US to UK Cont.

European diesel imports from Middle East and Asia fall

An important factor that precipitated the decline in demand for diesel barrels from the East of Suez are questions around the region’s ability to make German winter spec. Other than Reliance Jamnagar on West Coast India and minor volumes from Adnoc’s Ruwais refinery (668kbd), it is largely thought that most of the region’s other refineries are unable to make significant volumes of this specific diesel for the European markets, therefore propping up precious supplies from the USGC refineries.

As we move past peak winter demand in the Northern Hemisphere amid softening pricing incentives to move barrels toward Europe, we focus on another deterrent; diesel barrels moving through the Red Sea. According to 2023 Vortexa data, 43% of all core-European diesel imports transited via the Red Sea (close to 100% of all East of Suez inflows). This increase was largely due to the EU ban on Russian oil into Europe alongside the new refinery start ups in the Middle East. However, longer tonne miles and war risk premiums will both serve as arb constraints for prompt delivery into Europe which could continue to make US barrels attractive.

In the first half of February less than 100kbd of Wider Arabian Sea diesel may arrive in Europe due to the temporary impact of the close to complete rerouting via the Cape of Good Hope. But huge volumes are then set to arrive in the second half of February, which at some point will weigh on overall arb economics, contributing to keep more Wider Arabian diesel yet to load in the East of Suez market.

*Core Europe includes: Norway, Switzerland, UK, Austria, Belgium, Bulgaria, Croatia, Cyprus, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden