Demand indicators point to a divergence in transportation fuel imports into LatAm

In this insight we explore the divergence within LatAm clean markets from a transportation fuels perspective to understand the changing dynamics for flows of these products.

Vortexa data suggests that LatAm seaborne diesel import demand has grown fairly significantly ytd 2024 and diverged away dramatically from gasoline/blending component imports as seen in the chart below. During Jan – Aug 2024, diesel imports rose by 5% compared to the similar period in 2023, while gasoline imports into the region plunged by 11%.

This significant drop in gasoline imports has largely come from the biggest buyer, Mexico, which alone reduced imports by 7% y-o-y during Jan-Aug 2024. Higher than average refinery run rates during the first half of 2024 negated the need for seaborne imports into the country. Meanwhile, Brazil, the second largest importer of gasoline in LatAm, reduced its gasoline imports by half from Jan – Aug 2024 compared to year ago levels.

Looking closer at the diesel market, Brazil and Peru’s diesel imports surged, rising 11% and 17% respectively when comparing Jan-Aug 2024 y-o-y. A large portion of Brazil’s refineries were on turnaround during Q2 and Q3 of this year. Meanwhile a 10% drop for diesel imports to Mexico was observed for the same period.

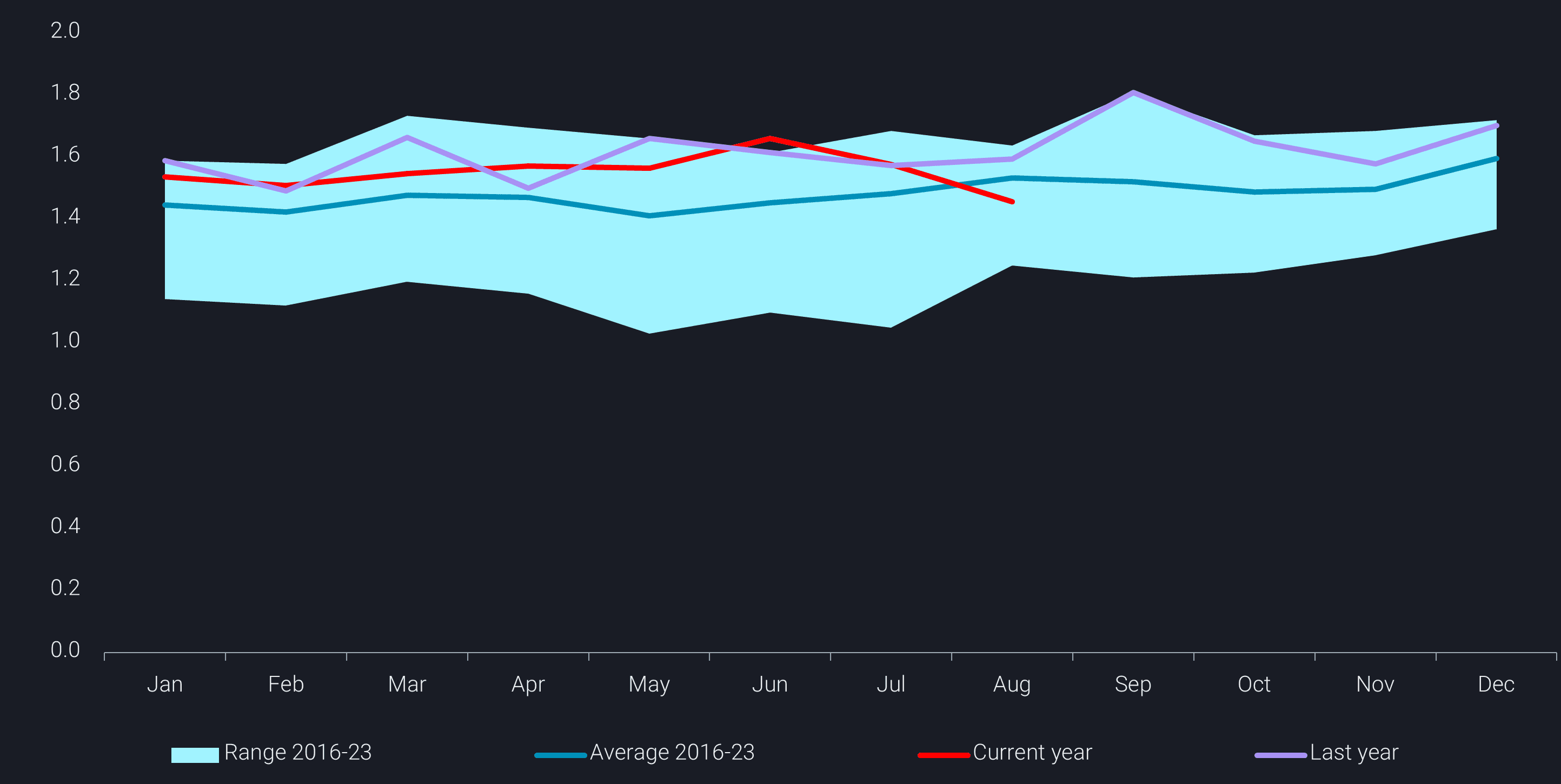

Taking a closer look at LatAm, we can see that transportation fuel imports into LatAm East Coast rose above the seasonal norm in June, largely related to a spate of unplanned refinery outages in Mexico causing a steep and sudden increase in seaborne import demand. However, imports are now seen moving into the region below the eight year seasonal average, underpinned by a steep drop (23%) from Argentina for both diesel and gasoline when comparing Jan – Aug 2024 with Jan – Aug 2023. Fuel prices in Argentina increased rapidly from November 2023 to April 2024 after the government imposed policies which reduced subsidies alongside a devaluation of the currency (Argus Media).

While Mexico’s East Coast witnessed a flurry of import activity later in the summer, the West Coast tells a different story. LatAm West Coast transportation fuel imports have fallen below last year’s levels largely underpinned by a 19% drop in seaborne imports to Mexico’s West Coast Jan-Aug 2024 compared to 2023. Chile’s transport fuels also decreased by 24%

And despite the relatively weak demand for transportation fuels in LaAm so far this year, the non-North American flows into Brazil, Peru and Chile have remained at the top of the seasonal range for most of the year. Russia moved into the top spot in 2024 to become the major supplier to the region, providing 51% of transportation fuel supplies and pushing Europe down to 12% and Asia to 10%.

Looking forward, the strength in clean product imports into LatAm are likely to slow down further in the longer term given the eventual start up of the Olmeca/Dos Bocas refinery (340kbd) on the East Coast of Mexico. However, in the short term, we could see healthy import demand continue due to refinery outages alongside the difficulties of ramping up gasoline production at new refineries.