Despite softening demand global distillate strength looks promising

In this insight, we examine global distillate strength and its promising outlook, despite softening demand in the Mediterranean and amid low global inventories, as well as looming H2 refinery maintenance.

As global diesel margins approach a 17-month high (since February 2024) amid steepening backwardation, healthy global demand has been underpinned by a mix of regional factors which could start to soften as we approach Q4.

The Mediterranean has witnessed a summer dominated by power generation needs amid delayed ramp-up of LNG supplies in Egypt alongside new emission standards in the region driving up diesel arrivals above the nine-year seasonal average and exceeding the seasonal range.

Meanwhile in Asia, India’s diesel demand was boosted by the trucking sector due to an unusual lull in monsoon rains that normally drive down transportation fuel demand during June and July. South and East Africa have been pulling volumes of diesel reaching above the seasonal range since January. In South America West Coast, arrivals hit a multiyear high in June, while levels continue above the eight year seasonal range in July driven by a high demand for agriculture and mining amid unplanned refinery outages.

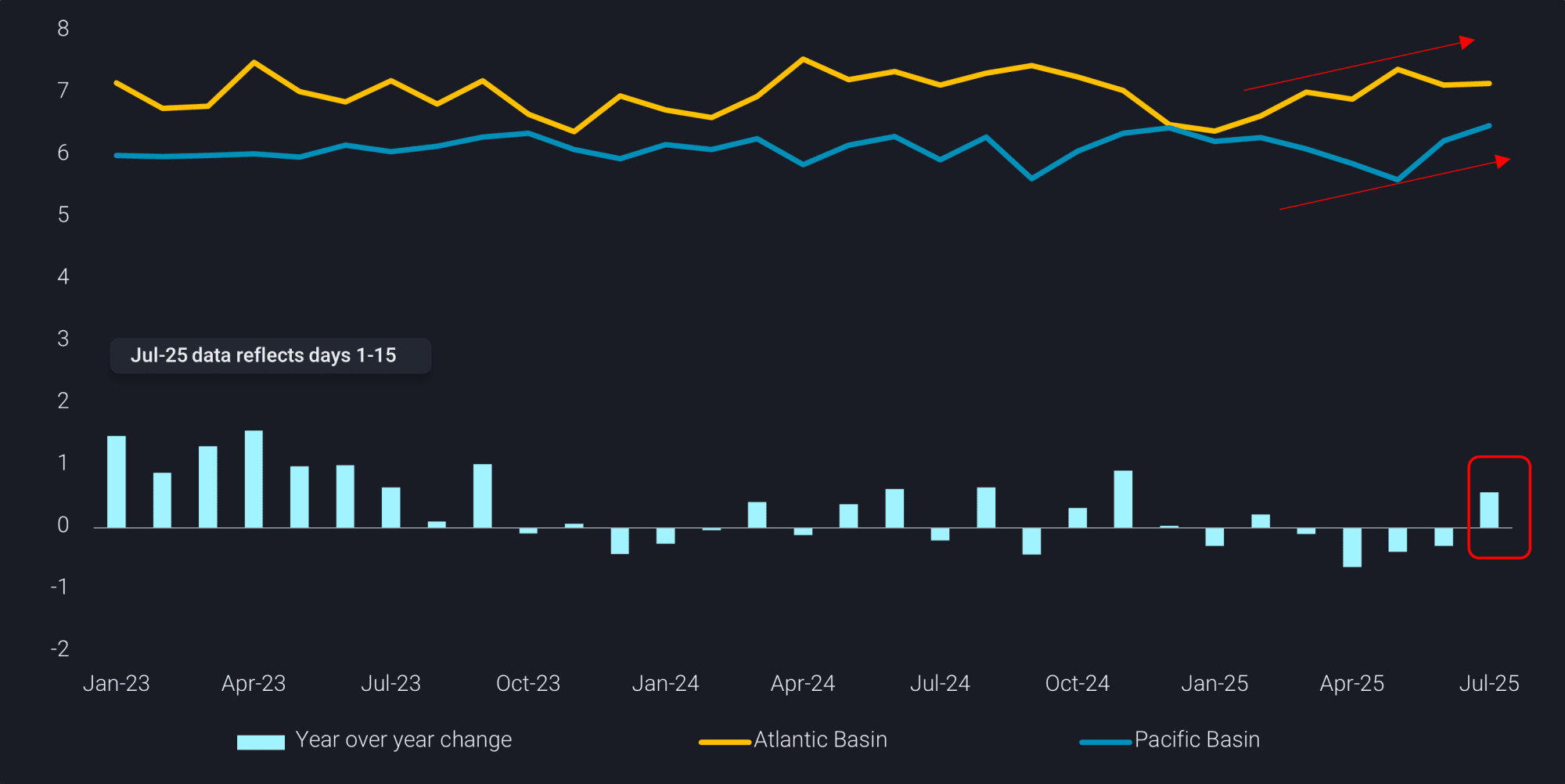

This mix of demand factors are resulting in the highest year-on-year increase in middle distillate arrivals since H2 2024 with this strength continuing unabated.

Middle distillate arrivals by destination basin (Atlantic gold, Pacific blue) and year on year change (bars, mbd)

From the supply side, distillate loadings from the top 100 refinery linked ports rose 8% in July y-o-y and 12% since May, reaching levels above the seasonal range prompting seaborne crude arrivals to these coastal refineries (+1 mbd y-o-y) for days July 1-22, the biggest change since April 2024.

Demand outlook

As we look ahead to Q4, the argument for power generation propping up the diesel margins starts to dissipate as Egypt connects the four new FSRUs between July and August, which are expected to largely mitigate the declining domestic gas fields and boost LNG supplies. This will be a key driver that will likely soften the need for the current high diesel imports into the Med.

However, despite the Med demand likely softening, on the upside the autumn/winter season beckons in the Northern Hemisphere amid low inventories on both sides of the Atlantic and Pacific Basins off the back of a summer of steep backwardation. Singapore middle distillate stocks fell to a 10-week low by July 18 (Argus). ARA diesel and gasoil inventories fell by 4pc to 1.85mn t in the week to 9 July, down by 15pc from the same week last year (Argus). And despite US distillate stocks’ recent weekly stock build (data ending July 18), inventories remain below the bottom of the five-year range (EIA).

Additionally, the refinery maintenance season which normally starts in September could push the current diesel margin strength into winter considering hurricane season lingers and the ongoing creep of light sweet into the overall refinery slate that could cap diesel yields until refineries return from seasonal outages.