Europe’s light distillate imports from alternative sources hit fresh highs in March

Will the loss of Russian naphtha and gasoline blending components make gasoline production in Europe difficult from a blending perspective or will Europe continue to be supplied by the four big alternative suppliers that we are currently seeing export higher volumes to Europe?

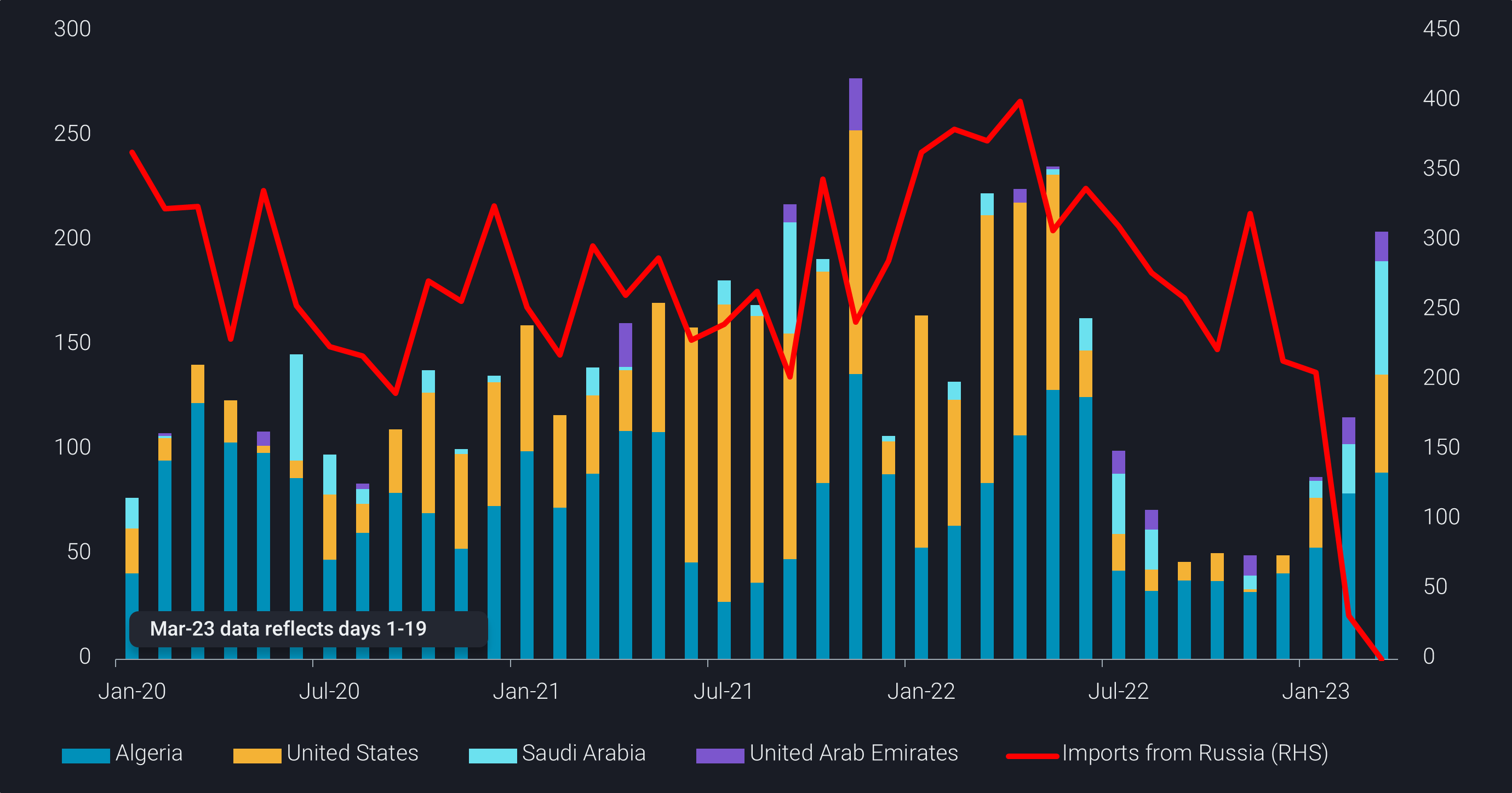

Algeria, US, Saudi Arabia, and the United Arab Emirates have increased light distillate flows to Europe in total by 76% so far in March m-o-m. Algeria alone has increased exports for three consecutive months since December suggesting that replacement needs for Russian supplies are attracting barrels from these alternative sources.

As we officially move into spring in the Northern Hemisphere, we turn our attention away from a well supplied diesel market and toward the less well supplied light distillate market and observe four big alternative suppliers to Europe, especially of naphtha coming into play.

Even with growing volumes of substitute barrels coming in, a shortfall of light distillates into Europe will likely continue. In 2022, European light distillate imports from these growing alternative sources averaged 120kbd while imports from Russia averaged 310kbd which means even with the increased flow, Europe will continue to be short on naphtha for gasoline blending, at least from an historical perspective.

We have also observed in March a 13% m-o-m increase in European gasoline headed toward West Africa, possibly due to the region’s demand for a lower spec gasoline.

Meanwhile, US Atlantic coast gasoline imports from Europe fell by 46% in March m-o-m. Given PADD 1 gasoline inventories have been drawing since mid February (EIA), new opportunities to send gasoline from Europe to PADD 1 will likely open as we advance closer to April when summer gasoline spec moves in demand.

Currently, we see more upside to the gasoline and naphtha market than the diesel market which is largely a function of the substantial shifts on the refining side as we see diesel supply swelling and with that the need to incentivize at least some refiners to shift yields back toward light distillate production. There is upside too on the demand side as we move into the driving season.

Nevertheless, Europe should be in a relatively good position to cope with the loss of Russian naphtha, given its considerable net length in light distillates. Euroilstock data is showing marginally higher light distillate inventories and production February y-o-y. Higher inventories coupled with strong refinery runs and relatively low planned spring turnaround season could give a boost to light distillate supplies while replacement barrels are coming in as well.