Global diesel pricing – bull or bear?

While a flood of East of Suez diesel imports has improved Europe’s positioning for the upcoming winter, Russia-Europe flows are rising again ahead of the 5 Feb EU import ban. Overall, the market may be better positioned for the challenge than many think.

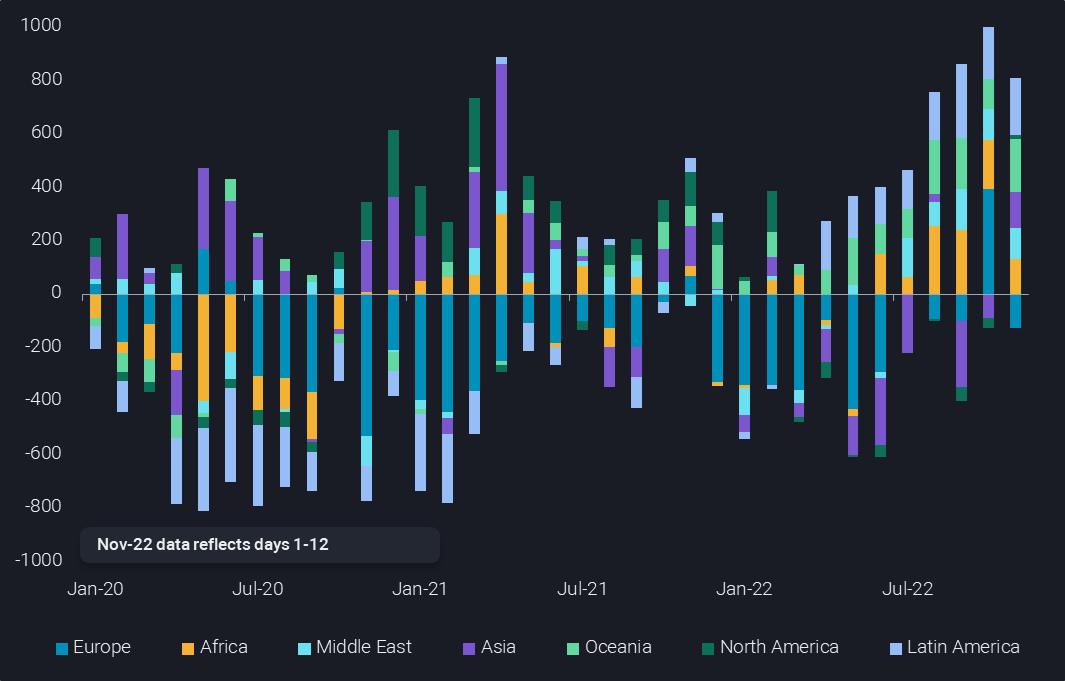

Through October EU & UK diesel imports from non-Europe/non-Russian sources surpassed a massive 1mbd, driven by supplies from the Middle East and Asia. More recently inflows are slowing down a bit, reflecting refinery maintenance in some origin markets. But the Chinese policy change asking for much higher clean product exports is now showing its impact and should help to boost East-of-Suez flows to Europe (largely indirectly). Two big new refineries in China are in the process of starting up operations, helping the export efforts.

Even beyond China, we are now entering a stage of new refining capacity coming online in significant volumes. Kuwait’s 600kbd Al-Zour plant is the most imminent addition, but 2023 may also see grassroots refineries in Oman, Nigeria and Mexico processing oil. We should however always keep in mind that the timelines for these ventures, especially with regards to on-spec diesel production, are fraught with uncertainty. This is illustrated by the track record of Saudi Arabia’s Jizan refinery, which is once again rumoured to reach full commercial operations soon.

On top of new production capacity, a lot of refining capacity is coming back from refinery maintenance and outages (e.g. French strikes). Potential catalyst changes may drive diesel yields even higher now than we had already seen over the course of the year. The incentives to do so have been unusually pronounced, both in extent and persistence. Taking all this together, the supply-side picture looks encouraging from a volume perspective.

The three main bull factors in the market

But of course, there are three massive bull factors at work, keeping diesel cracks still in the vicinity of the historically extraordinary $50/b level:

1) Extra demand from European winter needs,

2) The looming loss of Russian oil,

3) Apparently very low stock levels.

Much has been speculated about the potential extra demand for diesel from heat and power generation in the context of Europe’s natural gas and electricity crisis. But we are already in mid-November and gas storage is so full that LNG tanker queues are forming around Europe to unload cargoes. Price pressure has eased across the board, with a somewhat unwanted hand coming from the economic slowdown. Another semi-appreciated factor is global warming, derailing the European skiing season for now, but evidently helping with heating needs. The chances are high that the upcoming winter will at least not be unusually cold.

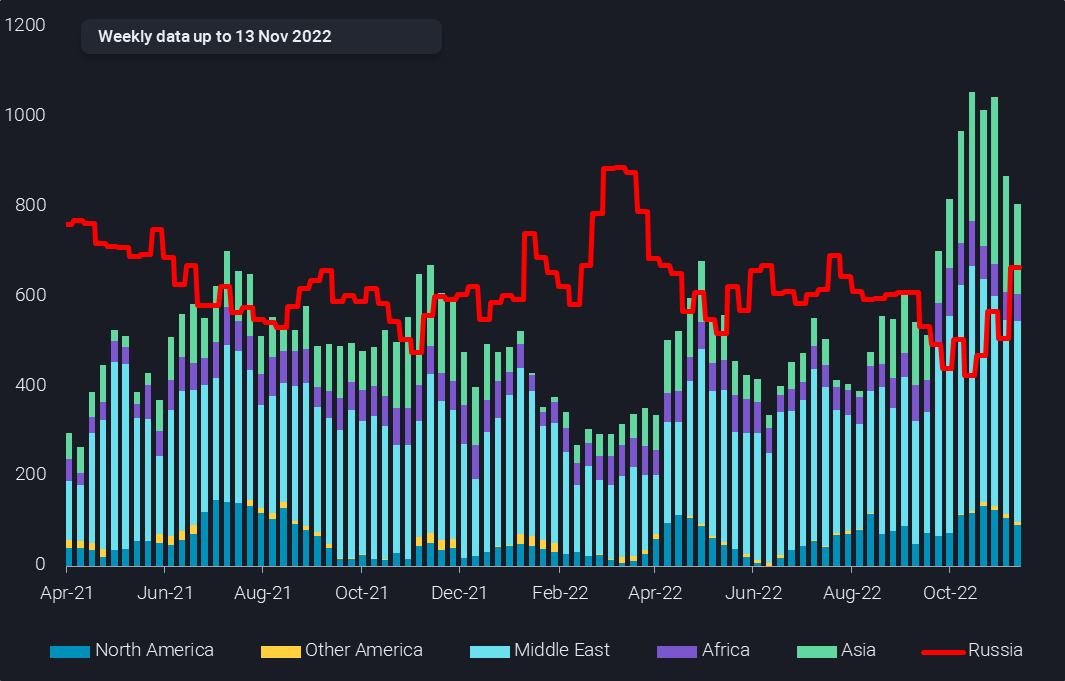

Even more difficult than to call the weather is to predict what will happen around EU sanctions on oil imports from Russia, as well as on services around third-party imports. Widely divergent forecasts are out on the extent of Russian crude supply that will be lost over the next couple of months. For diesel, it is even more challenging to make calls. Russia’s refining output and product exports hinge on the fate of all products, including very-difficult-to-place naphtha, and residues that now flow easily to Asia but may fall victim to dirty vessel shortages. However, we have two more months to find out what will happen with product exports as crude takes the lead in about 20 days.

The US is meanwhile working very hard – behind and front of scene – to ensure Russian oil continues to reach markets to avoid further price and inflationary pressures. After all it is at least a possibility that Russian clean products will find alternative outlets relatively easily, given much lower volumes involved and the lessons learned from crude, possibly including the implementation of the global price cap mechanism.

Another crucial price driver is low stocklevels, at least where they are easily visibly. That is specifically the US, with the US Northeast seen as the key undersupplied consumer market, and the ARA trading hub. However, we do believe that massive diesel imports around the world, especially into Southern Hemisphere markets, over the last four months signal more buying than running consumption.

In extension, that means tertiary stockbuilds at small-sized tanks held by the actual consumers of diesel, such as agriculture, commercial, industrial, and transportation businesses. Pretty much every business owner with a diesel exposure is following the news headlines, talking about the worst winter in Europe since the Second World War and likely related diesel squeezes. If that assumption is true, it would mean that import levels are set to cool in line with Northern Hemisphere temperatures. As a final comment, low trading hub stocklevels are simply a reflection of working markets, with record diesel cracks and strong backwardation incentivising traders to refiners to place as many cargoes as possible.

In conclusion, time is moving fast, and we will soon know how winter weather and sanctions on Russia play out. There is room for further temporary price spikes, but ultimately the chances are high that all the supply/demand adjustments, enclosing also the deepening recession, will put an end to the diesel crack and refinery margin rally some time in Q1 2023. In contrast to the crude oil market, there is no OPEC+ or US SPR buyback programme that will underpin product margins. Refinery run cuts could already be a reality or imminent for simple setups in the Asian market and more is likely to come in 2023.