Volatile global flows and hydrogen economics leave Europe short in naphtha

Naphtha flows have seen strong volatility, especially for US sources barrels. Surging European imports and falling loadings are linked to hydrogen economics. The current lack of inflows is boosting cracks.

Naphtha flow developments over the last couple of months are a great example of how adaptive the industry is, and how various factors play together to create quite some volatility in global movements, both in terms of levels and directions. Vortexa data helps to find and visualise the shifting dynamics early on.

Naphtha owns a sizable and completely unique niche in the oil industry. Its uses are pretty divergent, as feedstock for the petrochemical industry, and as blending component/intermediate product for the gasoline pool. In the interest of both target markets, naphtha may or may not run through catalytic reforming units, being largely converted into reformate, either a high-octane gasoline component, or the feedstock for BTX/ethylbenzene chains in the petchem path.

An additional complexity and opportunity stems from the fact that catalytic reformers are the only units in a refinery that produce rather than consume hydrogen. The latter may be a key energy carrier in the energy transition in the long term, but in the short term it is required to desulphurise transportation fuels in refineries. The major alternative supply source for hydrogen is steam reforming of natural gas (not a refining process). With LNG/natgas prices surging, hydrogen has become a massive drag on operating costs, weighing massively on the economics of exposed refineries in Europe and Asia. Extra-costs can range up to $5/bbl (IEA), but are usually not reflected in most refinery margin calculations.

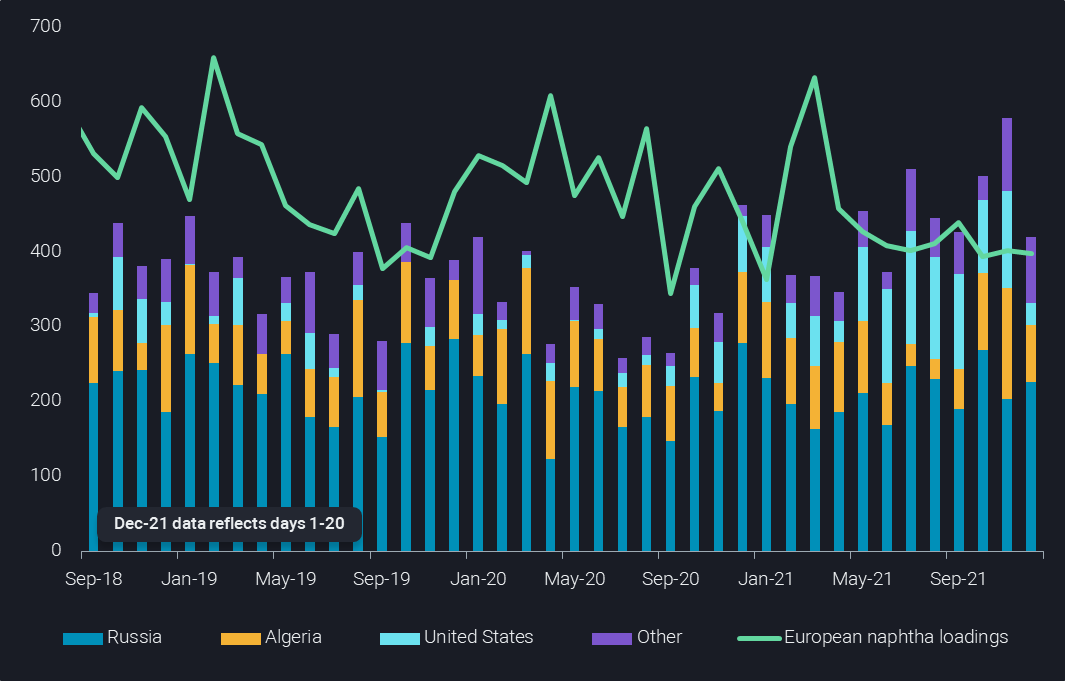

European naphtha imports by origin (bars) and regional naphtha loadings (kbd)

Why that somewhat theoretical digression? Because it may well impact naphtha flows and pricing, especially in Europe. Q4 has seen extraordinarily low naphtha loadings from Europe (incl. Intra-country flows), with the idea being that refiners run reformers as high as possible to produce hydrogen, reducing at the same time naphtha supplies. The main product of the process, reformate, may then call for more external naphtha to blend proper gasoline grades. This could help explain the very high level of naphtha imports into Europe during the Jul-Nov period. Healthy gasoline cracks in that period, as well as sky-high LPG prices and related low inflows into Europe, added to the high demand for external naphtha.

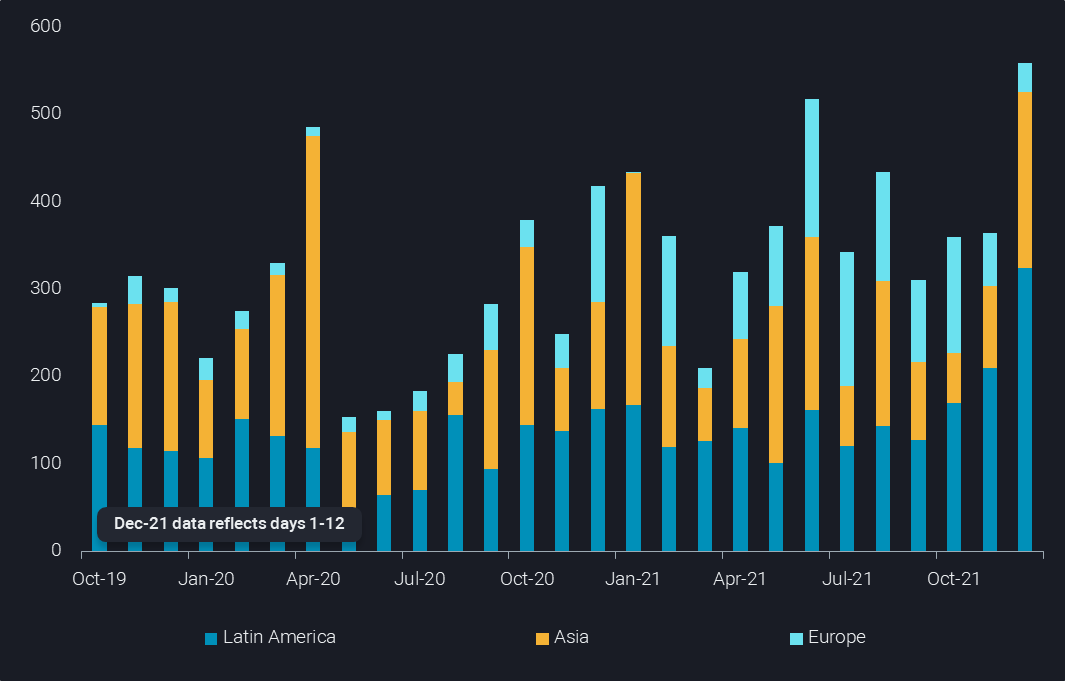

Naphtha exports from the United States by destination (kbd)

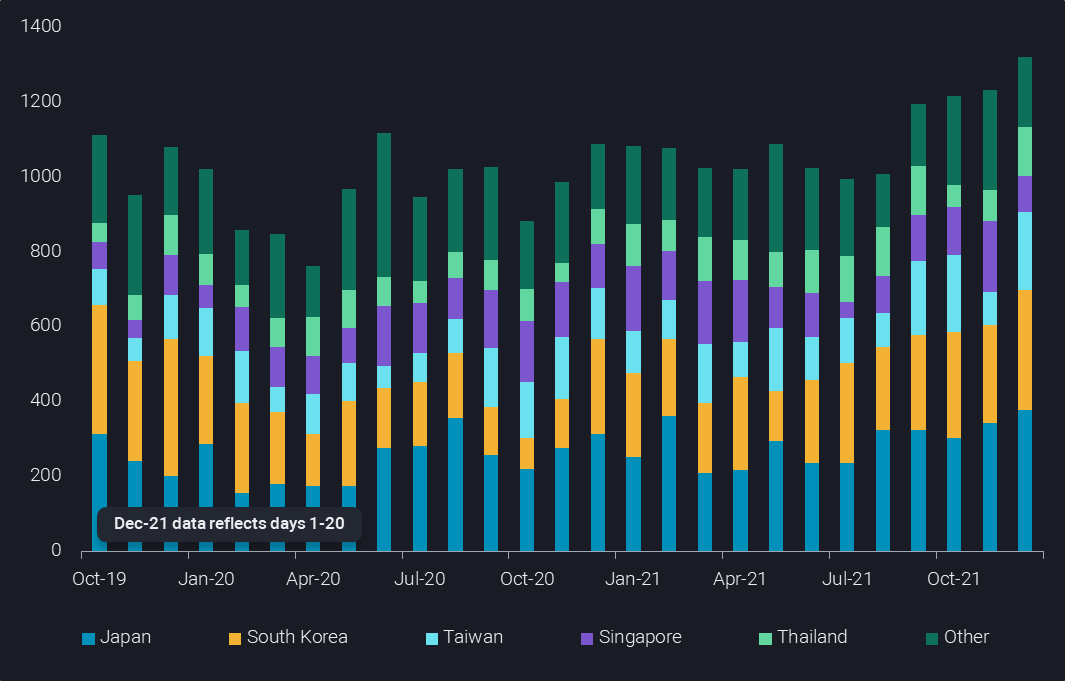

The high summer/autumn naphtha flows to Europe came at the margin primarily from the United States (see chart above). To quite some extent, US flows were redirected from Asia to Europe, encouraged by a massive step up in Middle Eastern naphtha arrivals in Asia ever since September (see chart below).

Asian naphtha imports from the Middle East by destination country (kbd)

But over the last 1.5 months, loadings from the US to Europe fell sharply with barely anything arriving in the first 20 days of December. A huge call on US naphtha molecules has emerged from Latin America, in particular Brazil, supposedly for gasoline blending purposes. Flows to Asia are also rebounding, at least during Dec 1-12. This is now contributing to a very tight naphtha market, with Argus Media reporting European naphtha cracks reaching 6-year highs this week.

More from Vortexa Analysis

- Dec 14, 2021: 2022: The Freight Forecast

- Dec 9, 2021: Big oil producers shine as refiners

- Dec 8, 2021 Russia and Ukraine: What’s at Stake for Oil?

- Dec 7, 2021 LPG flood reaches Asia and Europe in December

- Dec 2, 2021 Omicron obscures outlook for tanker markets

- Dec 1, 2021 Rising flows, wrong time?

- Dec 1, 2021 What a time(ing)!?

- Nov 25, 2021 Clean tankers battle it out in the Atlantic and the Middle East

- Nov 23, 2021 How helpful is the US-led SPR release

- Nov 23, 2021 Asia’s gasoline cracks make an unexpected U-turn

- Nov 18, 2021 Asia’s crude appetite sweetens in November