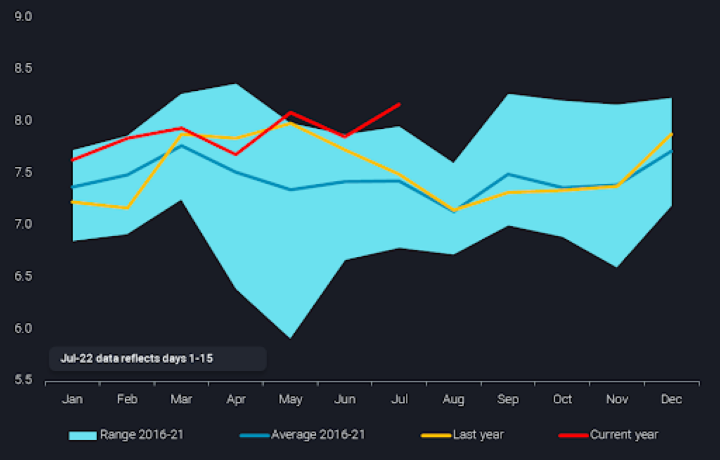

Global gasoline supplies reach seasonal highs as refineries start to re-balance supplies

Global refineries are running at maximum capacity and unless faster demand destruction takes place versus the supply decline, we can expect net inventory builds and lower seaborne gasoline flows.

Record high gasoline cracks have pushed global refiners’ gasoline production to a multi-year high, which has seen seaborne liftings/loadings reaching seasonal highs for three consecutive months since May.

As we move away from peak gasoline season in the Atlantic Basin and witness demand destruction in the East of Suez markets, we see global gasoline cracks fall from recent historical highs, incentivising global refiners to start maximizing middle distillate production as European countries look for alternative diesel sources before sanctions further curtail Russian oil imports, latest around the turn of the year.

Demand Upside

Any yield shifts towards middle distillate production for flexible refinery systems will likely result in a downturn in seaborne gasoline liftings after July since future gasoline demand upside is limited from here, which while supported by a stellar post Covid demand recovery in Latam, is weighed down by lower demand in Southeast Asia due to demand destruction.

Countries like the Philippines are heavily dependent on imports and exposed to high gasoline prices, and unlike Indonesia there are no tax credits or government subsidies propping up demand.

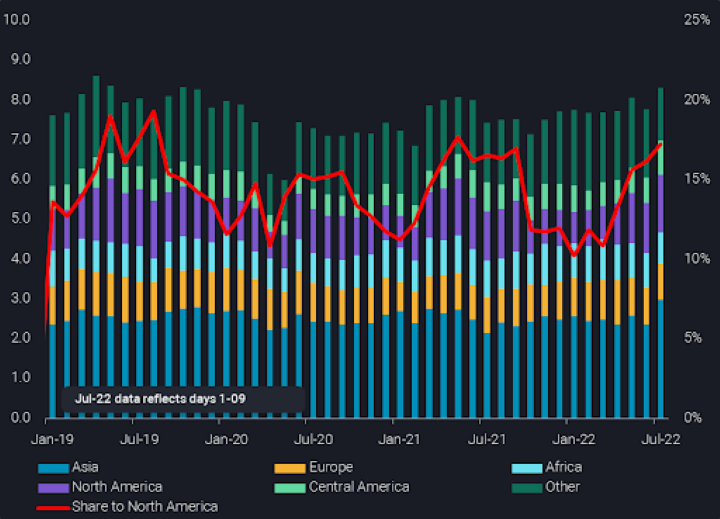

We will likely see continued demand stemming from the recovering US market whose historically low gasoline inventories have yet to be replenished due to scarce secondary unit feedstocks and limited high-octane blending component availability in Europe.

And although LatAm gasoline demand normally peaks mid summer, we will likely continue to see a pull on imports due to relatively low domestic production, keeping gasoline cracks buoyed in the US.

Supply Limitations

We are already seeing indications of gasoline supply changes East of Suez, especially in the Middle East and India where refineries operate with more flexibility. Seaborne liftings of gasoline have fallen 17% and 24% respectively in these regions in July compared to June. In addition, China’s clean product exports are also moving away from gasoline to jet/diesel with the lifting of travel restrictions, which is expected to see an uptick in domestic gasoline demand.

And in the US, although refineries are running at maximum utilization rates, the lack of Russian VGO for FCC feedstocks is causing refiners to run suboptimally compared to historical levels, resulting in overall lower gasoline production (EIA).

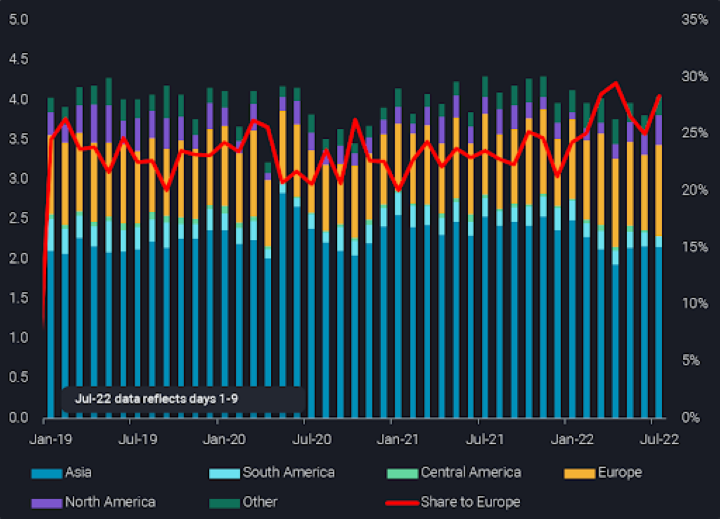

The US has taken advantage of the oversupplied naphtha market in the form of gasoline imports from Europe. As high octane blending components imports into ARA continue their declining trend since April, we see upward limitations of these imports. US PADD 1 gasoline imports from Europe were up 27% in June 2022 compared to June 2019.

And as European refiners continue to rely on light crude supplies to maximize diesel production, high gasoline supplies will likely continue to an extent keeping global supplies ample as gasoline-rich crudes especially from West Africa, Caspian and the US.

Global refineries are running close to maximum capacity with the exception of Russia and China and to some extent unplanned turnarounds in Europe. Although elevated global gasoline prices are eating into demand, unless demand destruction takes place to a larger extent than the supply decline, we can expect to see net inventory builds and lower seaborne gasoline flows in the near term.

Looking ahead, as we see global refineries limit supplies to correct the gasoline supply imbalances caused by price inflated demand destruction, we could see a floor for global gasoline cracks.