High-sulphur fuel oil arbitrage flows reverse as Russia redirects its residues

In a trend that’s likely to stick, rising Russian fuel oil flows to East of Suez markets have weighed on Asia’s HSFO markets in recent weeks.

Rising Russian residual fuel oil (RFO) flows to Middle East and Asia, away from western markets, turned traditional HSFO arbitrage economics upside down in May and threw into reverse a trend of tightening HSFO balances that began to emerge around the end of the first quarter.

Russian exporters lost an important RFO outlet after the US placed a ban on Russian oil supplies, effective in late-April in response to the invasion of Ukraine. Russia residual fuels exports to the US averaged 270kbd between January and March 2022 versus 310kbd in 2021.

In Europe, the formal ban on Russian oil product imports is finally coming into force on 5 February 2023, but exports of Russian residual fuels to the continent have already declined as countries and businesses impose individual curbs on Russian exports. Russian RFO exports to Europe averaged almost 420kbd in the first five months of 2022, and a lower 365kbd since the war began, compared to nearly 500kbd in 2021.

This forced the world’s top fuel oil exporter to look to the east for other buyers to help plug the gap, with the trend potentially gathering pace as the European Union now has a clear-cut timeline for its own ban on Russian oil imports.

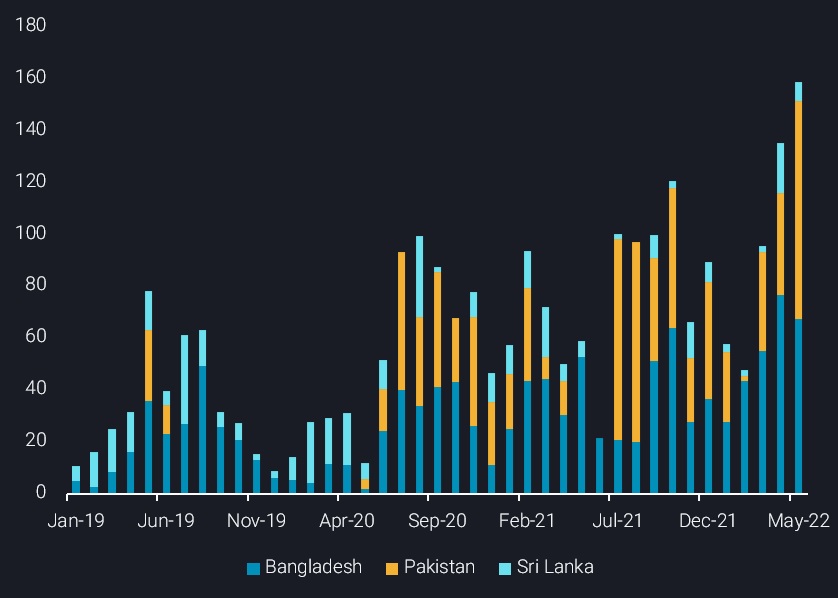

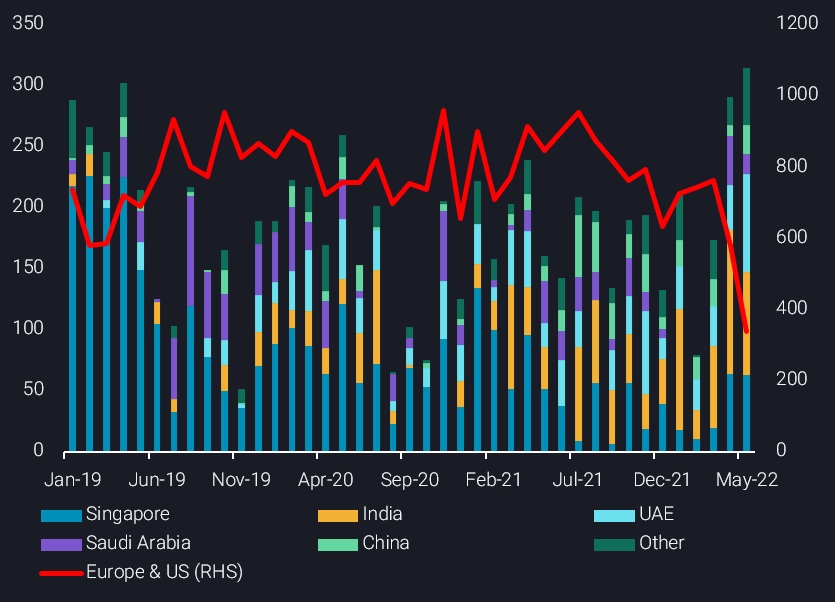

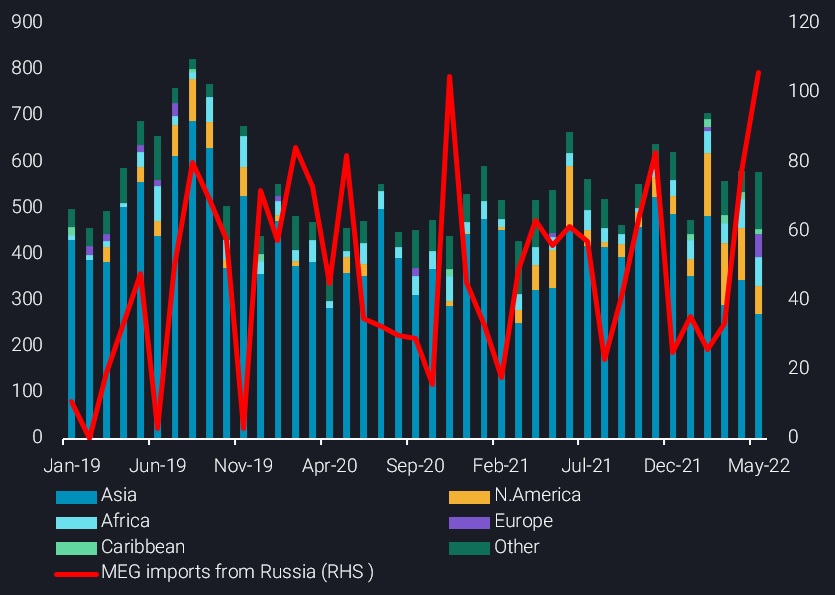

Combined fuel oil imports into Asia and the Middle East surged to 320kbd in May, the highest since at least 2016. Asia’s Russian RFO imports totalled 210kbd in April and May, the highest since April 2019, while May imports into the Middle East hit an 18-month high of 100kbd.

The higher Russian volumes into the Middle East in turn increased the availability of fuel oil exports to other regions including Asia and North America at a time when rising seasonal Middle Eastern demand for power generation constricts fuel oil exports from the oil-rich region.

Redirected flows hammer HSFO prices

The increased Russian flows to the east brought some much-needed relief to a market that was showing signs of tightening supplies as refiners maximized yields of gasoil and rising seasonal power generation demand. Issues around contaminated HSFO bunkers that emerged in Singapore in mid-February had also contributed to tightening HSFO supply.

But regional prices quickly retreated from their April highs as Russian cargoes began to point east. The 380cst HSFO front-month east-west arbitrage spread briefly fell to a rare discount in late-May (Argus data), cooling Asian HSFO prices as inventories were replenished. As one Singapore-based fuel oil broker put it: “I’ve never seen it before.”

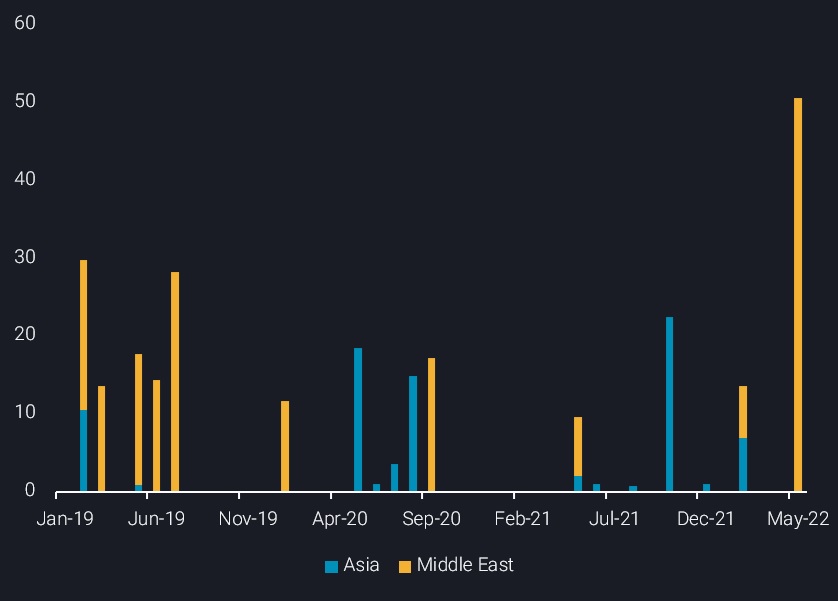

While it is unlikely this will trigger a sustained reverse arbitrage flow from Asia to Europe given a backwardated market structure and the greater voyage distances, there has been an increase in Middle Eastern fuel oil exports to Europe to a record 50kbd in May as buyers seek alternative supplies to Russian imports.

Asia’s benchmark 380cst HSFO crack to Dubai crude continues to tumble into deeper discounts in June amid ample supply. Similarly, the benchmark northwest Europe 380cst HSFO barge crack continues to widen its discount as the closed arbitrage window effectively blocks the European barrels from being exported to the east.

The ample HSFO supplies in Asia are likely to persist as Russia seeks to establish new outlets for its vast fuel oil output amid tightening western sanctions. Russia needs to clear its residual fuel supplies before it can increase its refinery runs again and allowing for more exports of high-value diesel. Also, the steady increase in global refining runs amid soaring refining margins should add to residue supplies, e.g. in Latin America, and put pressure on HSFO balances.

This comes in stark contrast to an acute tightness in the VLSFO market, where prices have surged to record highs over the past two weeks, widening the HiLo (HSFO-VLSFO) spread to a record high. This is in part due to red-hot transportation fuel cracks which are pulling in higher-quality, low-sulphur residues to optimize conversion unit runs and yields that would have otherwise ended up in the VLFSO blend pool.

The wide sulphur spread also benefits ship owners and operators that have installed scrubbers and it is likely to continue incentivizing owners to seriously consider scrubber installations in their decisions as fuel prices continue to rocket.