Light distillates come into focus

The massive shifts away from light distillates production and trade toward middle distillates during 2022 and into 2023 could provide support for light distillates from here on.

Diesel exports in Q4 2022 were 8% higher compared to Q4 2021, largely due to a huge push from China and Russia, with January 2023 showing continued strength. The surge in diesel exports – even before the majority of the 1.7 mbd new refining capacity scheduled to come online in 2023 – reflects a massive market reaction to the high diesel cracks that have persisted since the Russian invasion in Ukraine. Diesel crack spreads have already fallen during the second half of January 2023, partly due to recessionary factors, relatively warm weather and a majority of the winter season already behind us, and high gas inventories. But most importantly falling diesel cracks are a reflection of ample global supplies, reducing the relevance of how successfully Russia reshuffles its diesel exports away from its core market Europe.

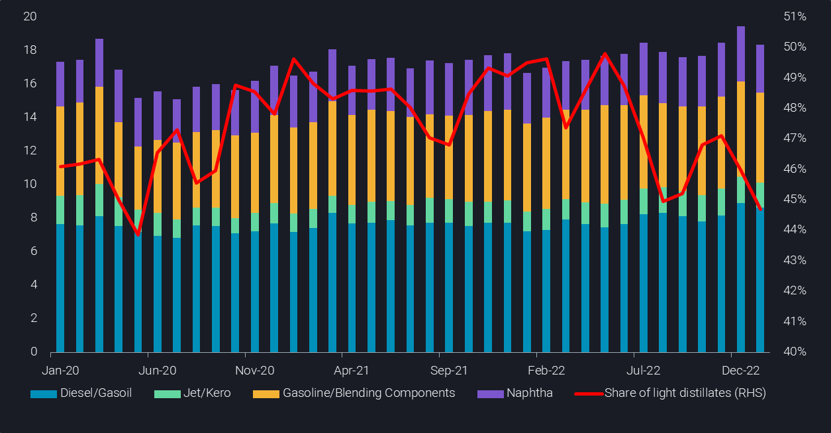

As we see global middle distillate seaborne exports grow over 2022 (blue and green bars), we can see the percentage share of light distillate exports (red line) decline due to refineries switching yields to take advantage of the high diesel margin. This extreme shift away from light distillates production could pose a risk in 2023 to meet demand which is expected to be elevated for instance in the US due to lower retail prices. Relative strong light distillate cracks could be required to move yields back from middle to light distillates, especially as we approach the US driving season amid low PADD 1 gasoline stock levels.

Demand for light distillates becoming evident

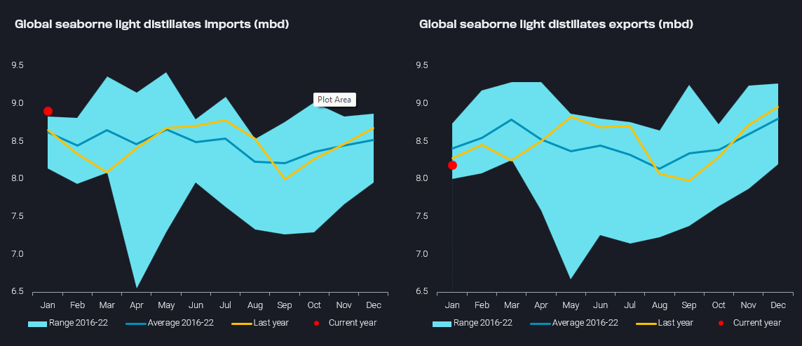

Indications of demand potential for light distillates is already surfacing in the flows data. We can see global light distillate imports on the left chart versus global light distillate exports on the right chart revealing very different paths.

Light distillate imports peaked at seasonal highs after gaining strength in late 2022, mainly driven by strength in Oceania and a pick up on naphtha from Asian markets. The opposite has been true for Europe where we have noticed high levels of exports and low imports partly due to low gasoline demand and high refinery runs in Europe, allowing gasoline flows to USAC and West Africa picking up in January.

Meanwhile, the very low world light distillate export levels in January 2023 (below seasonal averages) could indicate a looming shortfall for light distillates. As we look ahead to the upcoming US driving season, we expect higher than average US refinery spring turnarounds, lower retail fuel prices and low PADD 1 inventories (EIA), a perfect mix for strong seaborne transatlantic flows.

The fate of naphtha as petchem feedstock depends on Asia reopening

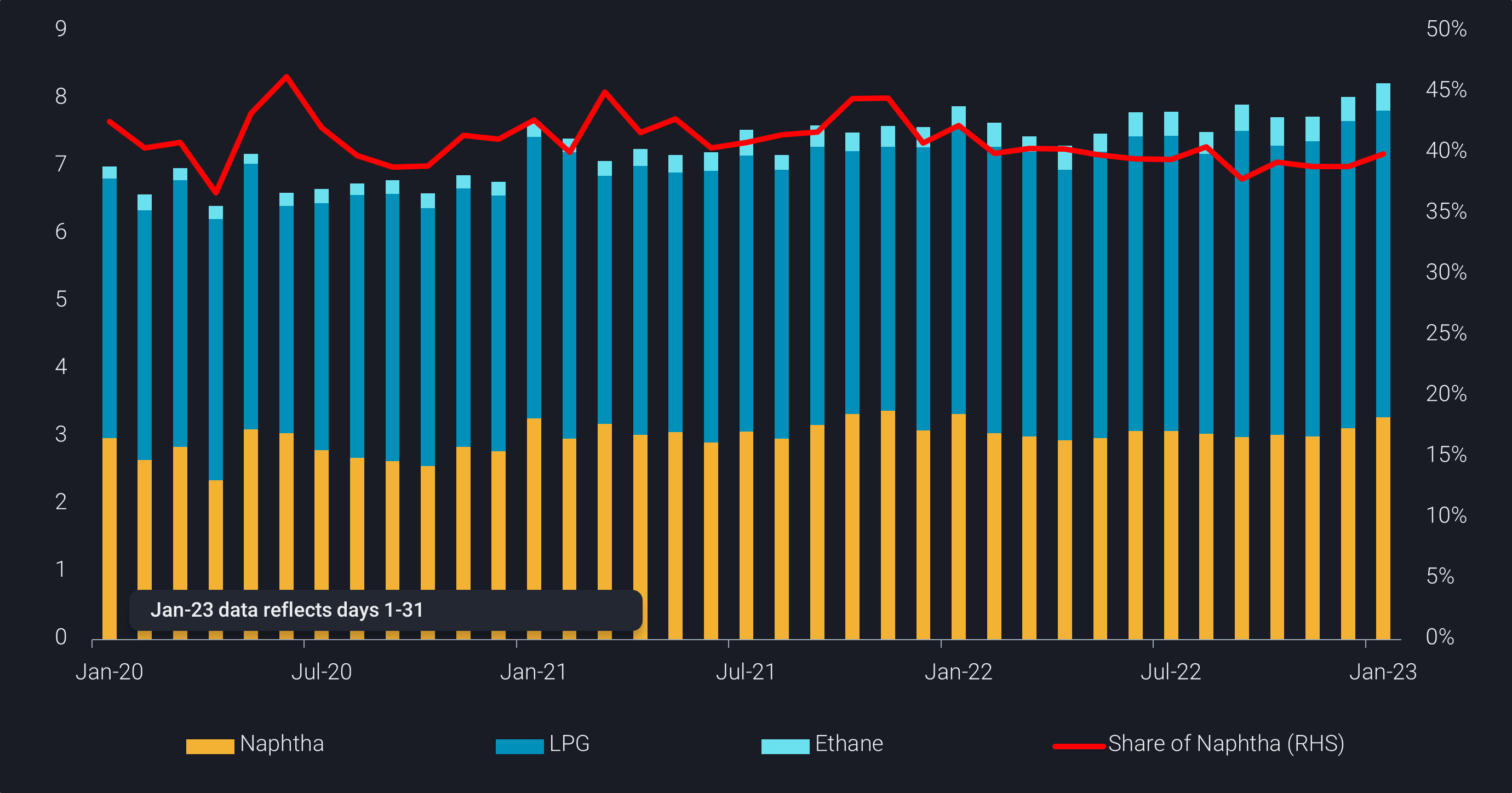

Turning to the petchem sector, global naphtha imports have sunk down to pandemic levels during 2022 in terms of percentage share of global petchem feedstock imports. Some of this can be attributed to growing volumes of LPG used in power generation and heating. However, as naphtha imports are a good indicator of the petchem market situation, until the world’s largest consumer China sees a recovery as it emerges from Covid lockdown, an uptick in light naphtha demand for crackers is unlikely to occur. We even may have to wait for the second half of the year.

EU ban on Russian product import impact to naphtha flows

Lastly, since naphtha exports make up Russia’s second largest clean product exports after diesel, it is important to understand where these volumes are moving, considering ARA is no longer available and Asia is slow to recover.

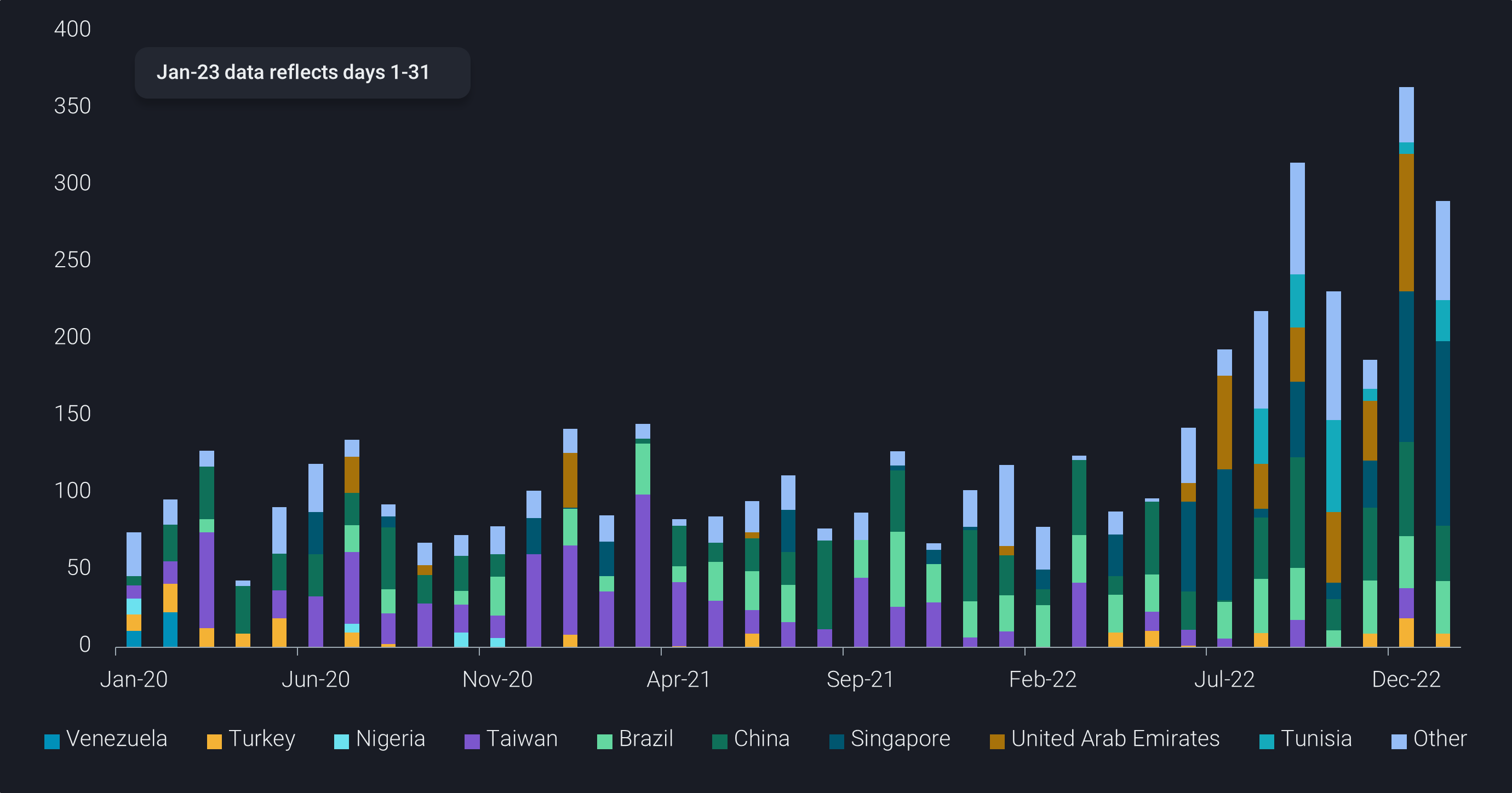

On the chart below, we can see Russian naphtha flows appearing in non-traditional locations and although no particular location is especially dominant, the Singapore bars are significant given restrictions to import Russian hydrocarbons. In fact, these flows are making use of STS, potentially disguising the origin of the molecules.

Europe, meanwhile, should be in an easy position to cope with the lack of Russian naphtha, giving its considerable net length in light distillates. Considering the high refining runs in Europe and relatively low planned spring turnaround season, it is likely there will be plenty of naphtha around for gasoline blending while demand for naphtha as petchem feedstock remains any subdued due to recessionary factors.

Looking forward, there is a strong case for strengthening gasoline cracks in the coming months, while the upside for naphtha hinges on China’s speed in re-opening its economy and overall regional petchem demand. This and Europe’s long-haul distillate import needs will likely give LR2s a good reason to enter or stay in the middle distillate market until a stronger recovery in long-haul naphtha trade flows is materialising.