Middle East CPP loadings climb with diesel leading gains

In this insight we examine how on a product and country basis the Middle East responds to global shifts in transportation fuels, especially diesel.

The importance of the Middle East’s role as a swing supplier of clean products has grown in recent weeks and given the current market fundamentals and the uncertainties related to Russia, this is likely to remain the case for some time.

News of discussions between France’s TotalEnergies and UAE’s Adnoc on a diesel supply agreement (Argus Media) underlines the important role the Middle East plays right now and even more so in the coming months, as European buyers seek to curb Russian oil. Quite some progress has been made in this regard in crude oil, residues and other products, but not yet for diesel.

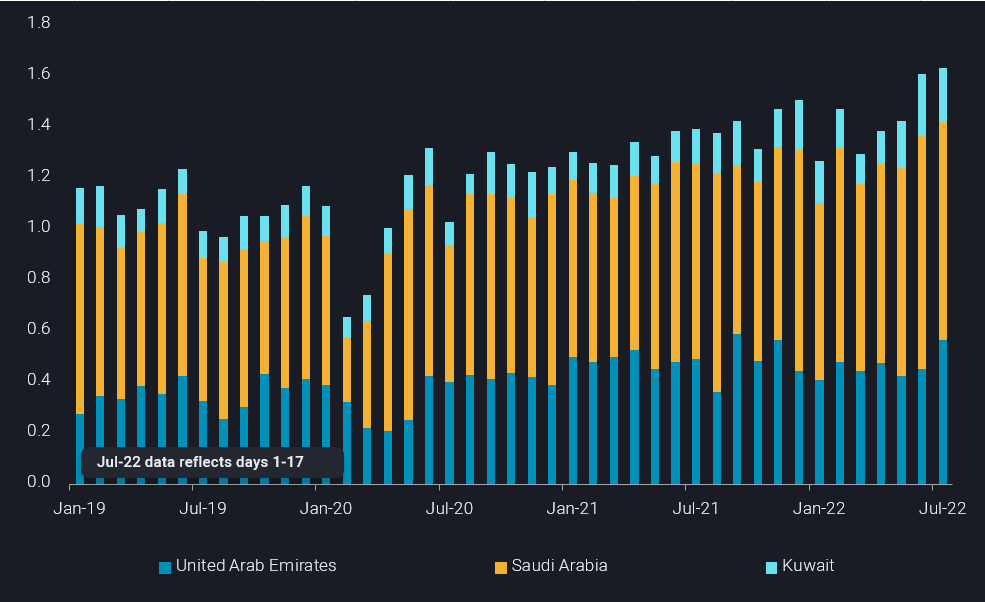

Our latest data shows Saudi Arabia, UAE and Kuwait as the key contributors to the recent growth in CPP loadings, especially diesel. These increases during the June-July period have come mostly from the back of refinery upgrades and/or increased refinery run rates.

In contrast, gasoline/blending components loadings from the Middle East have lost momentum and have likely peaked in the near term – the US driving season is now over (a dampener for West of Suez gasoline demand) and the concerns are growing over the impact of a wider recession/inflation upon East of Suez gasoline consumption.

Key highlights from our data:

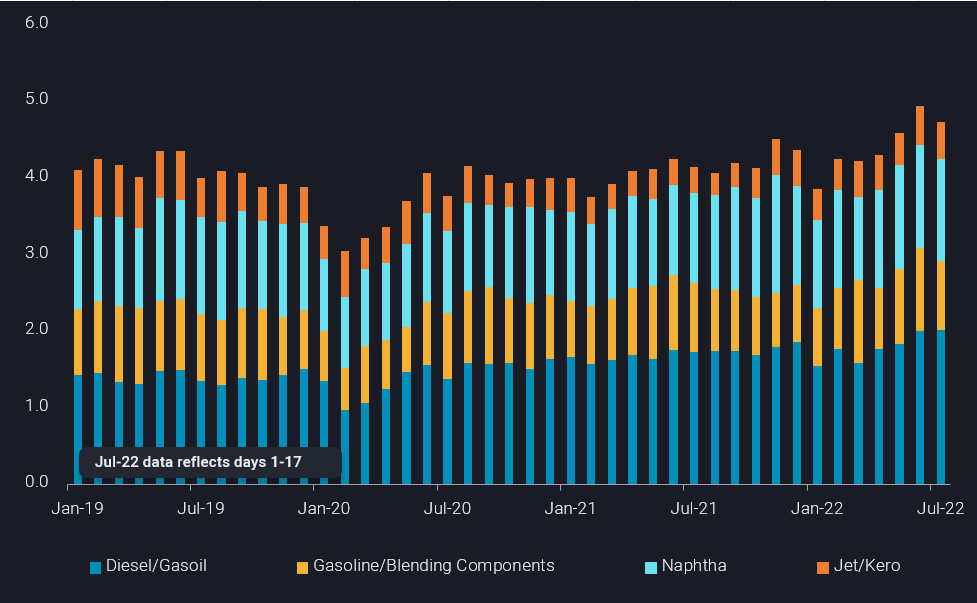

- Middle East key clean product loadings (diesel, gasoline, naphtha, jet) so far in July (1-17) are down by around 200kbd from 4.9mbd in June – the highest monthly total recorded by Vortexa data (since 2016)

- This m-o-m decline is largely due to lower gasoline/blending component loadings, and a slight drop in jet loadings

- Diesel/gasoil loadings for July still remain above the 2mbd mark, which was crossed in June for the first time in our observed data

- Saudi Arabia, UAE and Kuwait have been the main contributors to the regional rise in diesel loadings, with the three countries’ collective total up at 1.6mbd so far in July – matching the multi-year high set in the previous month

- Kuwait’s diesel/gasoil loadings since the start of June stand at 230kbd, up from an average of around 150kbd across Jan-May – this suggests KPC’s delayed clean fuels project may have reached completion

- Early indications in July show UAE’s diesel loadings have jumped by around 110kbd m-o-m – as one of the few suppliers in the region that can load VLCCs with diesel, UAE-Europe flows could rise in the coming months especially if a Total-Adnoc deal is finalised

- Saudi diesel loadings from the main refinery export refinery hubs (Jubail and Yanbu) peaked for this year in June at 780kbd and July loadings, though down 40kbd m-o-m, still remain high from a historical perspective

- Looking ahead, one key variable in the coming months is to what extent Saudi Aramco’s newest refinery in Jizan can ramp up loadings – less than 30kbd has been exported since May