Nowhere but storage for naphtha amid global supply glut

A rising volume of naphtha is building up in storage terminals in the ARA region and Singapore as demand for the petrochemical feedstock wanes. Slowing naphtha trade flows have seen LR tanker rates cool in the recent weeks.

Naphtha cracks are under immense pressure amidst a global oversupply stemming from weakness in petrochemical and gasoline blending demand. While Russia has cut back its naphtha exports by nearly 300kbd compared to the start of the year, naphtha supplies remain in excess of demand exacerbated by refiners cranking up their refining runs to meet the growing global gasoline and diesel tightness.

Loss of Russian naphtha no sweat for Asian crackers

Russia’s naphtha exports to Asia started their decline at the start of the year and accelerated after the invasion of Ukraine, falling to a low of 40kbd in April compared to 230kbd in 2021. While the lower Russian naphtha supplies have reduced the glut in Asia to some extent, it was not enough to offset a further retreat of naphtha cracks in the recent weeks as the outlook on naphtha demand turns more bearish.

Major cracker operators in Japan and South Korea are cutting back runs amidst weak margins, while Philippines’ JG Summit has decided to bring forward its cracker maintenance, reducing the overall naphtha demand in the region. The wide LPG discounts to naphtha continue to favour the former as the more economic feedstock for cracker operators, further limiting naphtha needs. It is not surprising that naphtha loadings to Asia in May have remained subdued at 1.4mbd, down nearly 25% y-o-y, with the trend expected to continue as margins fail to pick up.

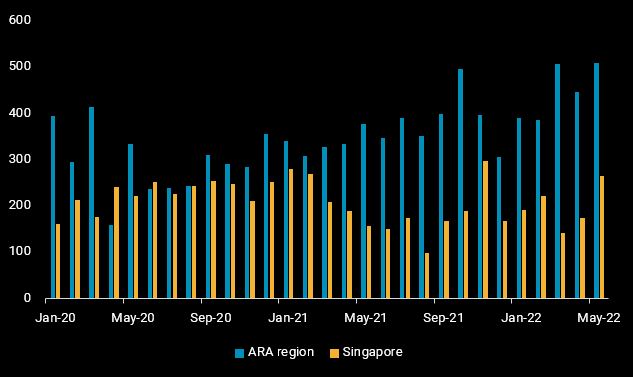

Excess naphtha supplies seek home in ARA and Singapore storage hubs

While actual inventory data is limited, the seaborne net trade flows of naphtha – measured by imports net of exports – offers a proxy of the net accumulation of naphtha supplies at a storage location barring domestic production and/or demand.

Net imports of naphtha into the ARA region in May crossed 500kbd for the second time this year, matching the multi-year highs seen in March, led by stronger inflows from Russia, Algeria and other exporters in the Mediterranean. A closed arbitrage to Asia has kept exports out of the region low, while regional naphtha demand for gasoline blending has been range-bound as well, despite a wide gasoline-naphtha spread. Naphtha’s low octane rating requires it to be blended with high-cost, high-octane blend components, limiting its attractiveness as a blend component.

In a similar trend, Singapore is also seeing its net imports of naphtha climbing for three consecutive months to 270kbd in May. Among the naphtha supplies, arrivals from the Middle East saw a large uptick, which would otherwise be destined for Northeast Asia if demand were healthy.

Seaborne net trade flows of naphtha into the ARA region and Singapore

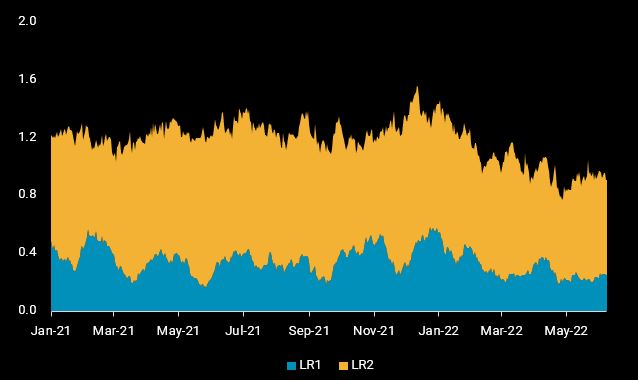

LR tanker rates sink as tonne-mile demand takes hit

As naphtha loadings to Asia slide, LR tonne-mile demand took a direct hit, declining by 15% in April/May compared to Jan/Feb. Despite this, the Mideast Gulf-to-Japan TC1 and TC5 rates rose sharply between late-Feb and early-May, receiving support from a knock-on effect of higher LR tonnage demand from other clean product trade flows that saw a re-positioning of vessels for other trade routes. These rates, however, have since cooled in May as the bearish outlook on naphtha loadings to Asia, coupled with a moderation of tonnage demand from other clean product trade flows, weigh on LR tankers’ tonnage demand.

China’s petchem recovery crucial for naphtha’s price recovery

The rising naphtha surplus will continue to pressure naphtha prices until cracker margins improve enough to incentivize higher runs. Crucially, light naphtha would need to find a home in crackers, unlike heavy naphtha which could be fed into reformers for aromatics production, the disposition for light naphtha is limited. There is upside potential that petrochemical demand from the world’s largest consumer, China, could see a gradual recovery as the country emerges from its Covid lockdown, driving an uptick in light naphtha demand in the second half of this year.